Risk Less. Grow More. – BusinessRiskTV.com for Smarter Enterprise

Tag: Attend Our Workshops and Masterclasses BusinessRiskTV Enterprise

Attend Our Workshops and Masterclasses BusinessRiskTV Enterprise Risk Management

Attending workshops and masterclasses can be a great way to enhance your knowledge and skills in a specific area of interest. Here are some tips to make the most out of these events:

Choose the right event: Research and choose the event that aligns with your goals and objectives. Look for the topics that are most relevant to your business or personal growth.

Prepare ahead: Before attending the event, make sure you have all the necessary materials, such as notepads, pens, laptops, or tablets. Also, research the presenters and their work to get an idea of what to expect.

Network: Workshops and masterclasses are great opportunities to meet new people and expand your network. Take advantage of breaks and other networking opportunities to connect with other attendees and speakers.

Engage actively: Participate actively in discussions and ask questions to the presenters. This can help you clarify any doubts or gain additional insights.

Apply what you learn: After the event, take time to reflect on what you have learned and think about how you can apply it to your work or personal life.

In summary, a

Attending workshops and masterclasses can be a valuable learning experience, but it requires active engagement and preparation to make the most out of it.

A critical business risk analysis of the 2026 global helium shortage triggered by Middle East conflict. Discover why semiconductor and healthcare sectors are at risk and the 12 urgent actions business leaders must take to protect their supply chains from a 33% supply collapse.

Why Is Helium Critical to the Global Economy?

Helium is the invisible backbone of modern high-tech industry because its unique physical properties make it irreplaceable for cooling superconducting magnets, manufacturing advanced semiconductors, and ensuring aerospace safety.As an inert gas with the lowest boiling point of any element, it is the only substance capable of reaching the temperatures (−269°C) required for MRI machines to function.Beyond healthcare, it is a “control point” for the digital age; without it, the Extreme Ultraviolet (EUV) lithography machines that produce 3nm chips for AI and smartphones would overheat and fail.

Financial Impact: As of March 2026, spot prices for high-purity helium have surged from approximately $600 to nearly $1,800 per thousand cubic feet, tripling costs for manufacturers in under a month.

Strategic Concentration: Just two countries—the United States and Qatar—account for roughly 75% of the world’s total helium production, making the global economy hyper-dependent on a single, fragile geographic bottleneck.

Irreplaceable Utility: The global semiconductor sector has surpassed healthcare as the largest consumer of helium, now accounting for over 25% of worldwide demand due to the explosion of AI-fueled chip production.

Why Should Business Leaders Worry About the Current War in the Middle East?

Business leaders must worry about the conflict because it has physically severed one-third of the global helium supply following missile strikes on Qatar’s Ras Laffan Industrial City.This isn’t just a pricing issue; it is a structural supply collapse.With the Strait of Hormuz effectively blocked, even operational facilities cannot export their product, leading to “force majeure” declarations that void long-term contracts and leave businesses scrambling for non-existent spot market volumes.

“The 2026 Ras Laffan shock has eliminated 33% of global helium output overnight.For industries like semiconductors, which are projected to grow 15–20% annually, this supply vacuum represents a terminal threat to 2026 production targets.” — Industry Risk Analysis Report, Q1 2026.

Who should be worried most?

Semiconductor Giants: Companies like Samsung, SK Hynix, and TSMC are facing an 8% contraction in chip output for the 2026 fiscal year.

Healthcare Providers: Hospitals in Western economies and developing nations alike are facing a “diagnostic blackout” as they struggle to keep MRI magnets cooled.

Aerospace & Defence: National security is at risk as helium is essential for rocket propulsion, satellite cooling, and advanced weaponry.

Where will the shortage be felt most?

Asia-Pacific (South Korea, Taiwan, China): These hubs are the most exposed due to their total reliance on Qatari seaborne exports.

Western Economies (Germany, France, UK): European markets have seen price increases of over 400%recently, as they lack the domestic reserves found in the US.

When Will the Helium Shortage Become Critical?

The helium shortage is becoming critical right now, with industry analysts warning that global inventories can only sustain current operations for a few more weeks before widespread production freezes occur.While some shipments remain in transit, the closure of key maritime routes means the “buffer stock” is rapidly depleting. By May 2026, the shortage is expected to transition from a pricing crisis to a physical unavailability crisis, forcing leaders to decide which business lines to shut down entirely.

12 Actions Business Leaders Must Take Today to Mitigate Impact

To protect your business from the “Helium Shortage” leaders should implement these risk management measures immediately:

Audit Helium Dependency: Identify every process, from leak detection to cooling, that requires helium.

Install Recovery Systems: Invest in on-site helium recycling and capture technology to reduce “once-through” consumption.

Diversify Supply Geographically: Shift procurement focus toward primary helium projects in stable regions like Canada, South Africa, and the US.

Implement Surcharge Pass-Throughs: Update contracts to allow for the passing of extreme gas price spikes to end consumers.

Secure Tier 2 Visibility: Map your entire supply chain to see where your sub-suppliers (like chipmakers) are vulnerable.

Accelerate R&D for Alternatives: Explore nitrogen or argon for less critical cooling or leak detection tasks.

Negotiate Long-Term Allotments: Move away from spot-market reliance and secure volume-guaranteed contracts, even at a premium.

Stockpile “In-Situ”: Where possible, keep additional ISO containers of liquid helium on-site as a strategic reserve.

Optimise Maintenance Cycles: Coordinate equipment maintenance to minimise helium “boil-off” during downtime.

Lobby for Strategic Reserves: Join industry groups like the BusinessRiskTV Business Risk Management Club to advocate for government-held helium reserves.

Adjust Production Schedules: Prioritise high-margin products that require helium and de-prioritise low-margin lines.

Engage in “Stability-First” Procurement: Value supply reliability over the lowest price in all future gas tenders.

Get help to protect and grow your business faster with BusinessRiskTV

The world is weeks away from a permanent yield loss in global agriculture. This analysis breaks down why the 2026 fertilizer shock is a “weapon of mass destruction” for your bottom line and provides 12 actionable steps to protect your business from the resulting global recession.

The 2026 fertilizer shortage is fundamentally a race against a biological calendar that no government intervention can bypass. While traditional media focuses on oil, the closure of the Strait of Hormuz on February 28, 2026, has trapped the molecules required to produce half the world’s food.

97% Collapse in Transit: Seaborne fertilizer trade through Hormuz has effectively ceased, cutting off 43% of global urea and 44% of the world’s sulfur.

No Strategic Reserves:Unlike oil, there is no global strategic fertilizer reserve. Once the “planting window” closes in the next six weeks, the yield loss for the year is permanent.

The “Biophysical Cliff”: In the Global South, where fertilizer application is already minimal, a 15% reduction in nitrogen doesn’t just lower yields—it causes production to collapse, as seen in Sri Lanka’s 40% rice harvest failure.

“The actual weapon of mass destruction in this conflict is not a missile. It is a calendar. The food is not decided by diplomats in six months; it is decided by soil chemistry in the next six weeks.” — BusinessRiskTV Global Intelligence

Can businesses in the Western world survive a global famine-driven recession?

A global famine-driven recession will impact Western businesses through a “bullwhip effect” of surging input costs and collapsing consumer discretionary spending. Even if food remains available in wealthy nations, the inflationary shock will be unprecedented.

AdBlue and Logistics Paralysis:Australia and Europe are facing a “no urea, no freight” scenario. Without urea-based AdBlue, heavy trucking fleets stall, leading to empty shelves in cities like Sydney and London.

Surging Input Costs:US corn farmers are already seeing ammonia prices hit $900 per ton. These costs will manifest as a massive spike in grocery prices by Q4 2026.

Macroeconomic Trap: With core PCE trapped near 3%, the Fed has no room to cut rates to stimulate a slowing economy, creating a “Stagflation 2.0” environment where food prices drive the CPI while growth flatlines.

What are the 12 business risk management steps to take today?

Audit Sub-Tier Dependencies: Identify where urea, ammonia, or sulfur sit in your deep supply chain (e.g., packaging, chemical processing).

Secure Logistics Fuel Additives: For firms with private fleets, stockpile AdBlue/DEF immediately to avoid grounding transport.

Renegotiate Fixed-Price Contracts: Shift to variable pricing or include “Force Majeure” clauses that account for commodity-driven hyperinflation.

Implement “Greed-flation” Monitoring: Track competitor pricing daily to ensure your margins aren’t eroded before you can react.

Diversify Sourcing to North America: Prioritise suppliers using Canadian or US-based nitrogen plants that are less dependent on the Gulf.

Hedge Food-Linked Commodities: Use futures markets to lock in prices for grains or livestock feed if your business is in the food/beverage sector.

Review Debt Covenants: Ensure rising operational costs won’t trigger technical defaults as interest rates remain “higher for longer.”

Scenario Plan for Civil Unrest: If your business has international footprints in the Global South, prepare for the “Sri Lanka Effect”—government instability driven by food shortages.

Optimise Product Portfolio: Shift focus to high-margin “necessity” goods as consumer discretionary income collapses.

Enhance Operational Efficiency: Use the next six weeks to cut non-essential overhead to build a cash moat for the Q4 price surge.

As a key business decision-maker, joining BusinessRiskTV is the most strategic move you can make in 2026 for three critical reasons:

Immediate ROI on Risk Intelligence: Membership provides actionable alerts on emerging threats—like the current fertilizer chokepoint—weeks before they hit mainstream media, saving members an average of 15% in avoidable procurement costs.

Global Expert Network: You gain direct access to a worldwide network of risk professionals who provide in-country intelligence and “no-fluff” strategies that turn volatility into a competitive advantage.

Low-Cost, High-Value Resilience: For a fraction of the cost of traditional consultancy, members receive real-time risk profile assessments and strategic updates designed to prevent costly operational mistakes during global crises.

Get help to protect and grow your business with BusinessRiskTV

While you’re watching oil prices, the molecules that feed 50% of the planet are physically trapped behind a war zone—and the window to save the 2026 harvest closes in exactly 42 days. This isn’t a “market correction.” It’s a biophysical cliff. 📉

We are currently witnessing the total collapse of the global fertilizer supply chain. With the Strait of Hormuz closed, 97% of seaborne fertilizer transit has evaporated. There is no Plan B. There is no strategic reserve.

The yield response to nitrogen is quadratic, not linear. In the Global South, production won’t just “dip”—it will collapse. We’ve seen this movie before in Sri Lanka, and now it’s playing in 30 countries simultaneously. For Western businesses, this means:

Logistics Failure: No urea = No AdBlue = No trucks moving groceries.

Inflationary Surge: Food prices will hit your table by Christmas with a force the Fed cannot stop.

The “Calendar Trap”: The Corn Belt needs nitrogen by mid-April. If they miss it, no amount of money can “fix” the yield loss in August.

Most analysts are talking about “strike counts” and “equities.” They are missing the soil chemistry. If you don’t understand how a sulfur shortage in the Gulf impacts a manufacturing plant in Ohio or a supermarket in Sydney, you are flying blind into the greatest recessionary shock of the decade.

Two-Speed Europe Business Guide: Risks, Opportunities & 6 Strategic Steps : The EU’s two-speed plan reshapes business. Our analysis covers the E6 group’s impact, supply chain shifts, and 6 essential risk management steps for leaders.

The E6 Core and the Coming EU Cracks: A Contrarian Risk Analysis for Business

The Inconvenient Truth: A Multi-Speed EU Reflects a Failing Political System

The proposal for a “two-speed Europe” championed by German Finance Minister Lars Klingbeil is not a clever, flexible solution for the European Union. It is a desperate, last-ditch political manoeuvre that starkly reveals the bloc’s fundamental dysfunction. The core thesis is this: The EU has become so politically paralysed that it can no longer function as a cohesive unit, forcing its largest and wealthiest members to abandon the pretence of consensus. The formation of the “E6” (Germany, France, Italy, Spain, Poland, Netherlands) is not a temporary working group; it is the blueprint for an elite, high-speed political and economic directorate designed to override the cumbersome machinery of the full 27-member union. This move does not save the EU; it initiates its reconfiguration into a core-periphery model that will breed permanent resentment and could catalyse the bloc’s gradual disintegration, particularly as political winds shift within its own core.

While defenders claim this is a “pragmatic” solution to EU decision-making inertia, the reality is that it formalises failure. It accepts that the core EU treaty principle of achieving “ever closer union” among equals is dead, replaced by a system where a few powerful states simply move forward and impose their agenda. This is not a benign technicality. It creates a de facto first- and second-class membership, where the “peripheral” nations are systematically disadvantaged, their policy autonomy undermined, and their ability to shape the European project severely diminished.

The “E6” Core Group: A Cartel That Will Ignore and Override the Rest

The risk that the E6 will act as an internal cartel, sidelining the wishes of other member states, is not a hypothetical fear—it is the explicit purpose of the formation.

Circumventing Vetoes and Imposing Policy: The primary motivation for the E6 is to bypass the EU’s unanimity requirement on sensitive matters like foreign policy, taxation, and security. When Luxembourg’s Prime Minister argued for a two-speed model, his logic was chillingly clear: “When a country says ‘I don’t want to,’ I can say: ‘Well, too bad. Don’t block me. Let me get on with it with others'”. This sentiment is the E6’s operating principle.

Existing Precedents of Core-Periphery Exploitation: This is not a new dynamic, but the hardening of an existing, exploitative one. An academic study examining the post-2009 crisis period shows how EU austerity policies, dictated by core institutions, devastated peripheral economies like Greece, locking them into a dependent relationship and widening economic and social gaps. The E6 formalises this power imbalance, allowing the core to set fiscal, defence, and industrial policies that serve their interests first.

The Single Market as a Tool of Coercion: Proponents argue that “outsider” nations will remain linked via the single market. In practice, this means they will be forced to accept regulations and standards set by the E6 to maintain market access, but will have no substantive vote in creating them. They become rule-takers, not rule-makers. The EU’s internal market, once a tool for convergence, risks becoming a mechanism for enforcing the core’s will on the periphery.

From Multi-Speed to Total Breakdown: The Domino Scenario of Collapse

The greatest existential threat to the EU is not this proposal itself, but the long-term political chain reaction it sets off.

Accelerating Divergence and Breeding Nationalism: A formalised two-tier system will halt economic and social convergence. One analyst warns it could increase economic divergence, leading to greater migration pressures and ultimately calls to limit the EU’s foundational principle of free movement. This fuels the very nationalist, anti-EU sentiments the bloc fears. Countries left in the “slow lane” will see their citizens grow disillusioned with a union that offers them diminished prospects and influence.

Political Shockwaves from Within the Core: The E6 is not a monolith. Poland’s inclusion is particularly volatile, given its government’s history of fierce clashes with Brussels over the rule of law. A future populist government in Italy, Spain, or even France could look at the E6’s commitments and decide to follow a British path. The exit of a single major E6 member would not just weaken the core; it would shatter the entire political and economic logic of the two-speed model, potentially triggering a rush for the exits.

The “Grexit” Precedent on a Grand Scale: The Greek debt crisis proved that the EU core was willing to entertain the expulsion of a member to preserve the eurozone. A two-speed Europe makes this concept operational. Weaker economies that fail to keep pace could face intense pressure to leave certain policy areas or be politically marginalised, creating a de facto “flexible disintegration”. Once the principle of an “inner circle” is accepted, the unthinkable—managing a member’s partial or full exit—becomes a policy tool.

Six Controversial Risk Management Steps for Business Leaders

Given this bleak prognosis, business leaders must abandon hope for EU stability and adopt a ruthless, realpolitik strategy.

1. Abandon “EU-Wide” Strategy; Adopt a “Core-First, Periphery-Contingent” Model

Action: Immediately re-allocate capital and strategic focus to the E6 nations. Treat the rest of the EU as a secondary, higher-risk market. Develop separate investment theses: one for the integrated, subsidy-rich core, and another for the volatile periphery.

Rationale: Future EU funding, defence contracts, and regulatory advantages will be heavily concentrated within the core. The periphery will suffer from capital flight and policy neglect.

2. Prepare for the End of the Single Market as We Know It

Action: Conduct stress tests on your supply chains and logistics for scenarios where free movement of goods, services, or people is restricted between the core and periphery, or where the core imposes new digital or regulatory borders.

Rationale: The political logic of a two-tier Europe inherently leads to regulatory divergence and potential barriers. Businesses cannot assume the single market’s integrity will survive this political fracturing.

3. Bet on the Core’s “Fortress” Economy—Especially in Defense and Tech

Action: Aggressively pivot business development towards sectors explicitly prioritised by the E6: defence manufacturing, dual-use technologies, critical raw material processing, and fintech platforms aligned with a deeper capital markets union.

Rationale: The E6’s agenda is to build strategic autonomy. This means massive, protected subsidies and procurement contracts for core-based champions, explicitly turning “defence into an engine for growth”.

4. Establish Political Risk Units Focused on Nationalist Movements in E6 Countries

Action: Move beyond tracking Brussels policy. Invest in intelligence-gathering on rising anti-EU, populist parties in Italy, France, and Poland. Model the business impact of any one of them winning power and renouncing E6 commitments.

Rationale: The stability of the entire new structure rests on the continued political alignment of its core members. This is its greatest vulnerability. A political shock in one E6 nation could unravel everything overnight.

5. Develop “Nation-State” Lobbying Capabilities to Bypass Brussels

Action: Drastically reduce reliance on pan-EU trade associations. Build direct, powerful lobbying operations within the national parliaments and ministries of Berlin, Paris, and Rome.

Rationale: Real power is shifting from EU institutions back to the capitals of the core nations. The E6 will decide policy in closed-door meetings, not in the European Parliament.

6. Scenario Plan for the “Domino Exit” and EU Liquidation

Rationale: While not the most likely scenario, the two-speed model makes a catastrophic failure sequence plausible. Leaders who dismiss this possibility are ignoring the historical precedent of how political unions can unravel with stunning speed when their central bargain breaks down.

Conclusion: Navigating the Unravelling

The two-speed Europe is a sign of profound weakness, not strength. It is an admission that the grand political project of unification has stalled and is now being replaced by a mercantilist club dominated by its largest economies. For businesses, the era of a predictable, rules-based EU is ending. The new era will be defined by geopolitical manoeuvring, privileged access for insiders, and heightened systemic risk. The prudent leader will not plan for a more integrated Europe, but for a fragmented one, where survival depends on picking the right side in a quiet internal conflict that has already begun.

The 2026 World Economic Forum in Davos revealed a stark rupture in transatlantic relations, creating immediate and long-term risks for global businesses. This analysis breaks down the key takeaways for leaders and provides six actionable steps to protect and grow your business in an era of heightened geopolitical confrontation.

The Davos Divide and the New Risk Landscape

The 2026 World Economic Forum in Davos will be remembered not for its solutions, but for its stark exposures. The confrontation between European leaders and the American administration laid bare a deep fracture in the Western alliance, moving geopolitical tensions from the background to the forefront of executive decision-making. President Trump’s antagonistic speech, which included grievances against European allies, questioning of NATO commitments, and a relentless focus on acquiring Greenland, signalled a profound shift toward a world where confrontation is replacing collaboration.

For business leaders, this is not merely political theatre. It is a direct and material risk. The WEF’s own Global Risks Report 2026 identifies “geoeconomic confrontation” as the top risk most likely to trigger a global crisis this year, followed by state-based armed conflict. This environment demands a new playbook for risk management—one that is proactive, integrated, and resilient. The old model of globalisation, with its deeply integrated supply chains and stable multilateral rules, is under severe pressure. As one analysis notes, companies are now forced to consider parallel supply chains and navigate a world where data, trade, and investment are increasingly weaponised.

This post provides a clear-eyed analysis of the key business risks emerging from Davos and outlines six practical, immediate steps to turn this uncertainty into a strategic advantage.

Key Risk Exposures for Businesses After Davos 2026

The events at Davos crystallised several interconnected risk categories that threaten business operations, strategy, and financial performance.

The core takeaway is the active unravelling of decades of economic integration. The U.S. administration’s focus on unilateral deals and transactional relationships, as seen with the “framework” for Greenland, undermines the predictable, rules-based system. For businesses, this translates directly into severe supply chain vulnerability. As noted in research from Wharton, companies are being forced to build duplicate, resilient supply chains—a China-centric one and a non-China-centric one—which creates enormous cost and redundancy. This fragmentation is no longer a future threat; it is a present-day operational and financial challenge.

2. Policy Volatility and Regulatory Divergence

Davos highlighted a growing chasm in core policy areas, especially climate and energy. While European leaders and CEOs like Allianz’s Oliver Bäte passionately defended the green transition, calling backlash “bulls—,” the U.S. administration championed fossil fuels and mocked renewable energy policies. This divergence creates a nightmare of regulatory compliance. Companies operating transatlantically face conflicting mandates, as seen historically with EU laws forcing tech changes (like the USB-C port mandate) and strict data rules like GDPR. The risk is being caught in a regulatory crossfire, incurring massive costs to comply with opposing standards in different markets.

3. The Weaponisation of Data and Digital Platforms

A novel and under appreciated risk highlighted in broader analyses is the politicisation of data. Governments increasingly demand control over data of multinational companies within their borders, using it as a tool for political leverage. This was evident in past pressures on tech companies during geopolitical tensions. In a world of “multipolarity without multilateralism,” your customer data, operational data, and intellectual property are no longer just corporate assets—they are geopolitical pawns. This creates immense risks for data security, privacy compliance, and brand reputation.

4. Erosion of the Social License to Operate

Businesses are increasingly “stuck in the middle” of societal and political polarisation. The “streets versus elites” narrative is rising, and companies face pressure to take stands on divisive issues while also demonstrating fealty to national governments. The WEF report identifies misinformation and disinformation as the #2 global risk over the next two years, which can rapidly inflame public sentiment against a brand. Navigating these waters without a clear strategy exposes companies to boycotts, talent attrition, and lasting reputational damage.

Six Practical Risk Management Steps for Business Leaders

In this age of competition, a reactive, wait-and-watch approach is a direct threat to survival. Here is your six-step action plan to build resilience and discover opportunity.

Step 1: Conduct a Geopolitical Stress Test on Your Core Operations

Immediately move beyond traditional SWOT analysis. Launch a cross-functional task force to conduct a dedicated geopolitical stress test. This involves mapping your entire value chain—from critical material sourcing and Tier-N suppliers to key logistics corridors and primary sales markets—against a map of escalating geopolitical flashpoints. Quantify the impact of potential disruptions. For example, what is the financial exposure if a specific trade corridor is tariffed or closed? What alternative suppliers exist outside of geopolitical hotspots? The goal is to move from qualitative worry to quantitative preparedness.

Step 2: Build a Dynamic Early Warning System

You cannot manage what you do not see. Relying on quarterly risk reports is obsolete. Implement an AI-powered early warning system that monitors real-time signals. This system should track not just news, but proposed legislation, social media sentiment, and trade policy adjustments in all your operational regions. Use technology to set alerts for specific keywords related to your industry, as some firms track terms like “oil drilling” in legislative texts. This transforms scattered data into actionable intelligence, giving you a crucial time advantage to respond.

Step 3: Formalise a “Political Risk War Room” and Governance

Political risk can no longer be siloed in government affairs. Follow the advice of experts and establish a cross-functional geostrategic committee that reports directly to the C-suite and board. This committee should include leaders from supply chain, finance, legal, communications, and strategy. Its mandate is to meet regularly, review early-warning intelligence, assess potential financial impacts, and authorise pre-planned contingency actions. This governance structure ensures rapid, coordinated decision-making when a crisis emerges.

Step 4: Develop “Plug-and-Play” Contingency Plans for Key Scenarios

For your top three geopolitical risk scenarios (e.g., “Sudden Tariffs on Key Import,” “Embargo on Technology Exports to Market X,” “Forced Local Data Storage Mandate”), develop pre-approved contingency playbooks. These should outline clear trigger points, decision authorities, and specific actions. For instance, a playbook for new tariffs might include immediate steps to activate alternative shipping routes, pre-negotiated contracts with alternative suppliers, and a communications template for customers. This shifts the response from panic to execution.

Step 5: Diversify Stakeholder Capital and Government Relationships

In a fragmented world, relationships are a critical risk mitigation asset. Proactively diversify your stakeholder engagement beyond traditional channels. Build relationships with policymakers, regulators, and community leaders in all your key markets before a crisis hits. Furthermore, explore financial resilience tools like political risk insurance to protect physical assets and investments in unstable regions. Also, reassess your capital structure and banking relationships to ensure you have access to liquidity from diverse sources if financial markets seize up due to geopolitical shock.

Step 6: Embed Strategic Agility into Your Business Model

Product Design: Develop products with modular designs that can be easily adapted to different regulatory or standards environments (e.g., different power specs, data protocols).

Manufacturing: Invest in flexible, smaller-scale production facilities (like “micro-factories”) that can be relocated or repurposed faster than monolithic plants.

Talent Strategy: Cultivate a distributed leadership bench with deep regional expertise, empowering local teams to make rapid decisions in response to local disruptions.

Conclusion: From Risk to Resilient Growth

The message from Davos 2026 is unambiguous: the business environment has fundamentally shifted. The greatest danger now is inaction—the risk of assuming the old rules still apply. However, within this volatility lies significant opportunity. Companies that proactively manage these geopolitical risks will not only protect their existing value but will gain a powerful competitive edge. They will be the ones able to seize market share as slower competitors falter, negotiate from a position of strength with governments, and attract investment as havens of stability.

The time for vague concern is over. The time for deliberate, structured action is now. Begin your geopolitical stress test this week.

—

Protect and grow your business faster with BusinessRiskTV

As private equity pours billions into AI corporate bonds to fund the “Big Seven” tech expansion, striking parallels to the 2008 subprime mortgage crisis are emerging. Explore the risks of circular funding, opaque credit ratings, and what this “AI Supercycle” debt means for global business stability and the economy in 2026.

Is AI Debt the New Subprime? The Private Equity Risks Facing the Big Seven

The global economy is currently witnessing a massive capital deployment into Artificial Intelligence infrastructure, largely driven by the “Big Seven” tech giants and fuelled by complex private equity debt. However, beneath the surface of this technological gold rush, risk managers are identifying structural echoes of the 2008 financial crisis. From “circular funding” loops to the role of credit rating agencies, the parallels are becoming too significant to ignore.

The Structural Parallels Between Mortgages and Models

In 2008, the “bedrock” was residential real estate; in 2026, it is the data centre. The fundamental belief driving today’s market is that AI demand will grow exponentially forever, mirroring the pre-2008 mantra that “home prices never go down.”

Credit rating agencies are once again under the spotlight. Just as they assigned AAA ratings to subprime mortgage-backed securities based on flawed correlations, they are now assessing AI-related corporate bonds and infrastructure debt with high grades. These ratings often rely on the perceived strength of the “Big Seven” (Microsoft, Alphabet, Amazon, Meta, Apple, Nvidia, and Tesla), yet they may overlook the rapid depreciation of the underlying collateral—GPUs and specialised servers that could become obsolete within years.

The Danger of Circular Funding and Shadow Banking

One of the most concerning parallels is the rise of “Circular Financing.” We are seeing a loop where tech giants invest equity into AI startups, which then use that same capital to lease compute power back from the investor’s cloud platforms. This inflates revenue figures and creates a “phantom” growth narrative.

Private equity firms and private credit lenders—the “shadow banks” of the modern era—are providing the leverage for these deals with less transparency than traditional regulated banks. This opacity mirrors the off-balance-sheet vehicles that hid systemic risk two decades ago. If the cash flows from AI applications do not materialise fast enough to service this debt, the entire “infinite money loop” could collapse, leading to a significant credit crunch.

What This Means for Global Businesses and the Economy

For modern businesses, this debt-heavy environment presents a unique set of risks. Companies relying on AI infrastructure could face sudden service disruptions or skyrocketing costs if their providers suffer a liquidity crisis. Furthermore, as regulators begin to flag these risks, the cost of borrowing for even non-AI businesses may rise as capital markets tighten in anticipation of a “re-rating.”

While some analysts argue that the “Big Seven” have enough cash to withstand a bubble burst, the systemic risk lies in the interconnectivity of the private equity ecosystem. A default in the mid-market AI sector could trigger margin calls and a “flight to quality,” potentially leading to a “tech-led” recession. Unlike 2008, the impact may be concentrated within the technology and private equity sectors, but in a world where tech is the backbone of all industry, the ripple effects will be felt globally.

To protect your business from the systemic risks associated with the AI debt bubble and private equity volatility, business leaders should implement a multi-layered risk management strategy.

Here are six actionable tips to build resilience today:

1. Conduct a “Shadow Infrastructure” Audit

Many businesses are unknowingly exposed to AI debt through their third-party vendors. Identify which of your critical service providers—from CRM systems to cybersecurity—rely on “Big Seven” cloud infrastructure or are heavily funded by private equity.

Action:Create a risk map of your technology stack. If a key vendor is part of a “circular funding” loop, they are higher risk for sudden insolvency or price hikes.

2. Diversify Across “Model Families”

Avoid “vendor lock-in” by ensuring your AI integrations are model-agnostic. Relying on a single provider’s API makes you vulnerable to their specific credit rating or debt obligations.

Action: Use an orchestration layer that allows you to swap between different Large Language Models (LLMs) or cloud providers (e.g., shifting from Azure to AWS or a private local server) without rewriting your entire codebase.

3. Move from Efficiency to “Compute Sovereignty”

During the 2008 crisis, businesses with “on-balance-sheet” assets fared better than those with complex lease agreements. Similarly, in an AI credit crunch, having your own dedicated compute resources can be a lifeline.

Action: For mission-critical AI tasks, consider “Small Language Models” (SLMs) that can run on local, owned hardware rather than relying exclusively on the expensive, debt-funded “Big AI” clouds.

4. Implement “Reverse Stress Testing”

Instead of asking “What if revenue drops?”, ask “What if our AI costs triple or the service goes offline for a month?”

The BRICS group’s pilot launch of the “Unit,” a gold-backed digital trade instrument, signals a major shift away from the US Dollar. For international businesses, this de-dollarisation trend creates significant FX and market access risks. Discover the 6 essential business risk management actions—from diversifying payment rails and currency hedging to supply chain re-evaluation—that business leaders must implement now to protect and grow their business in a rapidly changing, multipolar global financial landscape.

The launch of the BRICS “Unit” gold-backed digital trade instrument, even in its pilot phase, signals a significant, long-term shift toward de-dollarisation and the emergence of a multipolar financial system. This development primarily creates currency volatility risk, geopolitical risk, and market access risk for international businesses.

Business Risk Management Actions For BRICS Gold Backed Currency

Business leaders must take proactive steps to protect profit margins and capitalise on new trade opportunities that bypass the traditional dollar-centric financial architecture.

1. Diversify Currency Exposure and Payment Rails

Action: Systematically audit all accounts receivable and accounts payable to quantify exposure to the US Dollar (USD) versus BRICS currencies (BRL, CNY, INR, RUB, ZAR) and the new “Unit” if it becomes readily available for international trade.

Mitigation: Establish banking relationships or payment channels that can facilitate settlements in multiple currencies, including BRICS members’ local currencies and potentially the Unit. This reduces reliance on USD-centric payment systems like SWIFT.

2. Adopt Dynamic Currency Hedging Strategies

Action: Move beyond simple forward contracts and explore more flexible hedging instruments like currency options to protect margins while retaining the ability to benefit from favourable exchange rate movements.

Mitigation: Implement a formal, actively monitored Foreign Exchange (FX) risk management policy. Consider utilising natural hedging by matching revenues and expenses in the same currency to reduce net exposure (e.g., sourcing materials in Chinese Yuan if sales are also made in Yuan).

3. Revise Trade and Procurement Strategies

Action: Evaluate the cost-competitiveness of suppliers and buyers within BRICS and Global South nations who may preferentially adopt the Unit for trade settlement, benefiting from lower transaction costs.

Mitigation: Proactively renegotiate existing contracts to include multi-currency settlement clauses or specify pricing in a currency basket that aligns with the Unit’s composition (gold + BRICS currencies) to stabilise invoice values against pure fiat currency volatility.

4. Geographic and Supply Chain Re-evaluation

Action: Map the geographic distribution of your supply chain and customer base to identify regions most likely to adopt the “Unit” (i.e., BRICS nations, Global South/Africa).

Mitigation:Increase market intelligence focus on these regions. Where feasible, localise manufacturing or sourcing in key BRICS countries to operate and transact more easily within their emerging financial ecosystem and reduce cross-currency friction.

5. Monitor Political and Regulatory Developments

Action: Designate a senior executive or external consultant to track the official adoption status, technical specifications, and regulatory compliance requirements of the BRICS Unit in relevant markets.

Mitigation:Develop contingency plans for scenarios where major trading partners impose tariffs or sanctions in response to de-dollarisation efforts, such as the potential for US tariff actions.

6. Model Financial Impact Scenarios

Action: Incorporate high-impact, low-probability events—such as a rapid 10-20% USD devaluation or the swift, widespread adoption of the Unit across key commodity markets—into financial forecasting and budgeting.

Mitigation: Use the scenario models to determine acceptable levels of currency volatility for profit margins and establish clear trigger points for enacting the new, diversified hedging and payment strategies.

Get help to protect and grow your business faster with BusinessRiskTV

The Property (Digital Assets etc.) Act 2025 is a UK legal game-changer, formally recognising Bitcoin and stablecoins as property. This clarity opens major growth avenues but introduces new regulatory and financial reporting risks. Learn the seven critical risk management steps UK business leaders must adopt now to protect and grow their digital assets.

Property (Digital Assets etc.) Act 2025 is a major development for the UK’s financial and technology sectors.

The Act legally recognises digital assets (like Bitcoin and stablecoins) as a distinct form of personal property, separate from the traditional categories of “things in possession” (physical objects) or “things in action” (contractual rights).

Why the Act is Important to UK Businesses

The primary importance of this Act to UK businesses is the provision of legal certainty and clarity in a rapidly evolving area. This has several key implications:

Strengthened Ownership Rights: For businesses holding or trading cryptoassets, this statutory recognition means their ownership rights are now on a firmer legal footing.They have clearer legal pathways to prove ownership, recover stolen assets (through processes like freezing orders), and enforce their property rights in court.

Insolvency: Digital assets can now be clearly included in a company’s estate and claimed by creditors if a business goes into insolvency.This makes the administration process smoother.

Collateral and Lending: The clearer property status makes it easier to use digital assets as security or collateral for loans, potentially unlocking new funding avenues for businesses.

Integration with Traditional Law: It allows digital assets to be seamlessly integrated into existing legal processes, such as estate planning, trust structures, and cross-border litigation, saving time and reducing legal costs previously spent debating the assets’ fundamental legal status.

6 Business Risk Management Tips for UK Leaders

UK business leaders, especially those newly engaging with crypto assets or looking to expand their existing digital asset operations, should adopt a rigorous risk management strategy.

1. Establish a Comprehensive Regulatory Compliance Framework

Action: Conduct a thorough Regulatory Gap Analysis to map your current and planned crypto activities against the evolving UK regulatory perimeter (e.g., the Financial Conduct Authority (FCA) rules under the Financial Services and Markets Act (FSMA)).

Risk Mitigation: This addresses the risk of non-compliance (leading to fines, operating restrictions, or loss of license).Ensure robust Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) controls, including registration with the FCA if required for custody or exchange services.

2. Implement Superior Cyber Security and Custody Solutions

Action: Treat the security of crypto private keys with the highest level of care. Adopt institutional-grade multi-signature (multi-sig) wallets, use third-party regulated custodians, and maintain strict key management policies with geographic and personnel separation.

Risk Mitigation: This directly combats the high risk of theft and operational loss (e.g., due to hacking, phishing, or human error) which is irreversible on the blockchain.

3. Define Clear Governance and Risk Appetite

Action: Form a dedicated Digital Assets/Treasury Committee to define clear exposure limits, maximum permissible volatility, and use-case scenarios for digital asset holdings. Establish clear protocols for asset acquisition, trading, and disposal.

Risk Mitigation: This manages market risk (volatility) and governance risk. It ensures all digital asset activities align with the company’s overall risk appetite and are subject to transparent internal controls and audit.

4. Strengthen Consumer Protection and Transparency

Action: If your business serves UK retail consumers, adopt measures that align with the FCA’s Consumer Duty.Ensure marketing materials and disclosures are clear, fair, and not misleading, with prominent risk warnings about the volatile and unprotected nature of crypto investments.

Risk Mitigation: This shields the business from reputational and conduct risk by mitigating consumer detriment. New regulations will likely impose similar conduct-of-business rules as apply to traditional financial firms.

5. Review and Update Financial Reporting and Tax Procedures

Action: Engage with specialist crypto accounting and tax advisors now. Develop systems to accurately track the cost basis, valuation, and capital gains/losses on digital assets in compliance with HMRC and accounting standards (e.g., IFRS or UK GAAP).

Risk Mitigation: This addresses tax and audit risk. The unique nature of crypto transactions (e.g., staking rewards, DeFi yields, token swaps) requires specialised expertise to ensure accurate financial statements and prevent regulatory penalties.

6. Establish Comprehensive Legal Documentation and Insurance

Action: Ensure all contracts, terms and conditions, and smart contracts clearly define the legal ownership, governing law (UK law), and jurisdiction for dispute resolution, leveraging the certainty provided by the new Act. Simultaneously, explore new-generation crypto insurance products for crime, custody, and potential smart contract failures.

Risk Mitigation: This reduces legal risk by leveraging the new property status for enforceable contracts and manages financial loss risk by transferring certain unforeseen risks to an insurer.

7. Develop and Test Business Continuity Planning (BCP)

Action: Incorporate potential digital asset failure scenarios into your existing BCP and disaster recovery plans. This includes protocols for managing a custodian failure, a major blockchain halt/fork, or a significant regulatory change that restricts operations (e.g., sanctioning specific tokens or chains).

Risk Mitigation: This manages systemic and operational resilience risk. Given the global, decentralised, and 24/7 nature of crypto, traditional BCP procedures may be insufficient.

The Bank of England’s recent record £87.15 billion repo allotment, a tool used to provide liquidity to banks as the central bank reduces its bond holdings, could signal underlying stress in the UK banking sector. This growing reliance on the central bank for funds raises a red flag for the financial stability and economic safety of the UK. Discover what this means for the wider economy and learn six crucial risk management strategies every business leader should implement now to protect and grow their enterprise more resiliently in an uncertain economic climate.

Bank of England Allots Record £87.15 Billion in Repo Operation: What It Means for UK Business Risk

The Bank of England’s Record Repo Allotment: A Warning for UK Business? 🚨

The Bank of England recently allotted a record £87.15 billion in a short-term repo operation, a move that provides a substantial injection of liquidity into the UK’s banking system. While this may seem like a routine technical adjustment by the central bank, the increasing reliance on these operations could be a significant red flag for the safety of the UK’s financial system and wider economy.

What Is a Repo Operation and Why Is This a Red Flag?

A repo (repurchase agreement) is essentially a short-term loan. The Bank of England lends money to commercial banks and in return, the banks provide high-quality assets (like government bonds) as collateral. The Bank’s increasing use of this tool is directly linked to its Quantitative Tightening (QT) programme, which involves selling off the government bonds it bought during the era of Quantitative Easing (QE). The purpose of these repo operations is to prevent a potential liquidity squeeze in the financial system as the central bank reduces its balance sheet.

The record allotment is a red flag for a few key reasons:

Growing Illiquidity: The fact that banks are demanding a record amount of funds from the central bank suggests they may be struggling to find liquidity elsewhere in the market. This could indicate underlying stress in the banking sector and a reluctance among banks to lend to each other.

Systemic Risk: This reliance on the Bank of England for funding could be a sign of increased systemic risk. If a major bank were to face a sudden liquidity crisis, the central bank would be its lender of last resort. The increasing size of these operations shows the potential scale of that reliance.

Uncertainty and Instability: A record-breaking allotment, particularly one that exceeds a recent record, creates a narrative of growing instability. This can erode confidence in the banking system and the wider economy, making businesses and investors more hesitant to spend and invest. This uncertainty trickles down to businesses and consumers, affecting everything from investment decisions to household spending.

6 Risk Management Measures for Businesses

In an environment of economic uncertainty, business leaders must be proactive to protect their organisations. Here are six essential risk management measures to enhance resilience:

Strengthen Cash Flow and Liquidity:Cash is king, especially in a downturn. Focus on optimising your working capital by accelerating accounts receivable, negotiating longer payment terms with suppliers, and maintaining a healthy cash reserve. Create detailed cash flow forecasts to anticipate potential shortfalls and manage expenses.

Diversify Revenue Streams and Supply Chains:Over-reliance on a single product, service, customer, or supplier is a major vulnerability. Actively seek new markets, customer segments, and partnerships. For your supply chain, identify alternative vendors and consider strategies like near-shoring or holding a small buffer of critical inventory to mitigate potential disruptions.

Manage Debt and Capital Expenditure Wisely: During uncertain times, it is crucial to avoid taking on excessive debt. Evaluate all major capital expenditure projects. Postpone or cancel non-essential investments that don’t directly contribute to immediate revenue or operational efficiency.

Review and Optimise Operational Costs:Take a hard look at all business expenses. Eliminate unnecessary costs without sacrificing the quality of your product or service. This could involve renegotiating contracts, leveraging technology for greater efficiency, or consolidating services. The goal is to create a leaner, more resilient cost structure.

Why the Bank of England’s Record Repo Allotment Is a Red Flag

The Bank of England’s record-breaking repo allotment is a significant red flag because it points to potential underlying stress and growing liquidity issues within the UK banking system. While repo operations are a standard tool for central banks to manage monetary policy, the increasing size of these allotments, especially in the context of the central bank’s quantitative tightening (QT) programme, reveals a deeper problem.

Growing Illiquidity and Inter-bank Distrust: The primary role of a central bank’s repo operation is to provide liquidity. A record amount being requested by commercial banks suggests they are struggling to secure the funds they need from each other. In a healthy banking system, banks would lend to one another in the inter-bank market. The fact that they are turning to the Bank of England in such high volumes could indicate a breakdown of trust between financial institutions, which is a classic symptom of a stressed system.

Systemic Risk: The increasing reliance on the central bank for funding raises concerns about systemic risk. Systemic risk is the risk of a collapse of an entire financial system due to the failure of one or more institutions. If a significant portion of the banking sector is dependent on the Bank of England for liquidity, a sudden shock or disruption could have a cascading effect across the entire system. This over-reliance makes the financial system less resilient and more vulnerable to unforeseen events.

Uncertainty and Economic Instability: A record repo allotment creates a sense of uncertainty and instability in the market. The public and investors may interpret this as a signal that the banking system is not as robust as it appears. This loss of confidence can have a tangible impact on the wider economy. It can lead to a tightening of lending standards, making it harder for businesses and households to access credit, and it can also deter investment, ultimately slowing down economic growth. The large allotment, therefore, isn’t just a technical exercise; it’s a barometer of growing financial vulnerability in the UK.

Read more free business risk management articles and view videos

6 Essential Business Risk Management Measures for UK Business Leaders

In today’s complex and uncertain economic environment, proactive business risk management is no longer an option—it’s a necessity. UK business leaders must move beyond a reactive approach and build genuine resilience into the core of their operations. Here are six essential measures to take action on now.

Optimise working capital: Focus on accelerating accounts receivable by offering incentives for early payment or enforcing stricter payment terms. At the same time, negotiate more favourable payment terms with your suppliers to extend your accounts payable.

Create robust cash flow forecasts: Use financial modelling and scenario planning to predict potential cash shortfalls. This will help you anticipate problems and give you time to secure financing or make cost adjustments before a crisis hits.

Maintain a cash reserve: Aim to build a buffer of cash sufficient to cover at least three to six months of operating expenses. This reserve acts as a critical safety net against unexpected disruptions.

2. Diversify Revenue Streams and Supply Chains

Over-reliance on a single customer, product, or supplier is a major vulnerability. Diversification builds a more robust and flexible business model.

Review and diversify your supply chain: Identify and vet alternative suppliers, especially for critical raw materials or components. Consider a dual-sourcing model or incorporating local suppliers to mitigate risks from global transport issues or geopolitical events.

3. Conduct Scenario Planning and Stress Testing

Don’t wait for a crisis to expose your weaknesses. Proactive scenario planning allows you to test your business model against a range of potential threats.

Identify key risks: Create a comprehensive risk register that outlines potential risks (e.g., economic downturn, supply chain disruption, cyber-attack) and their potential impact.

High levels of debt can become a significant burden in a tightening credit environment.

Limit new borrowing: Be cautious about taking on new debt, particularly for non-essential projects. Evaluate every borrowing decision based on its potential return on investment and its impact on your balance sheet.

Re-evaluate capital projects: Postpone or cancel major capital expenditures that are not critical for business operations or do not have a clear and immediate path to profitability. Prioritize investments that enhance operational efficiency and resilience.

5. Review and OPTIMISE Operational Costs

A lean and efficient cost structure improves profitability and allows you to better weather economic storms.

Targets decision-makers searching for the financial impact of weak risk practices

THE HIDDEN TAX OF POOR RISK MANAGEMENT

Your business is leaking money. Not in the obvious ways — like overspending or inefficiency — but in silent, insidious drains you might not even see. Poor risk management isn’t just about avoiding disasters; it’s a profit killer, a growth stifler, and, in the worst cases, an executioner of businesses that could have thrived.

Consider this: 30% of bankruptcies are due to operational failures that could have been mitigated with better risk practices (OECD). That’s not bad luck—it’s self-inflicted. And if you think your company is immune, think again.

This isn’t theoretical. Every day, businesses hemorrhage cash through:

Employee disengagement —teams that don’t see risk as their problem, costing you in errors, delays, and lost innovation.

The result? Lower profitability. Stunted growth. And, in extreme cases, extinction.

But here’s the good news: this is entirely optional and fixable.

In this e-book, we’ll expose the 12 most damaging costs of poor risk management —many of which you’re likely paying right now — and deliver 12 actionable solutions to turn risk from a liability into a competitive advantage. You’ll learn how to:

Engage every employee in risk ownership (not just compliance, but profit protection).

Stop financial bleed from preventable failures.

Turn risk-aware decision-making into a growth engine.

This isn’t another dry risk management manual. This is a survival guide for profitable, resilient business leadership.

Ready to plug the leaks? Let’s begin.

🚨 YOUR BUSINESS IS LEAKING £££ – FIND THE HOLES! 🚨

83% of UK SMEs lose £50k+ yearly from hidden risks they don’t even measure:

❌ Operational failures burning cash ❌Supply chain disasters killing margins

❌ Cyberattacks costing millions

BusinessRiskTV’s NEW eBook reveals:

✅ 12 PROVEN FIXES to stop profit leaks

✅ Real case studies from UK businesses

✅ Simple checklists to act TODAY

Chapter 1: The Hidden Costs of Poor Risk Management – How Ignoring Risk Erodes Your Profits and Threatens Survival

Introduction: The Silent Profit Killer

Every business faces risks—some obvious, others invisible. But when risk management is an afterthought, those risks don’t just linger; they multiply costs, shrink margins, and sabotage growth. This chapter exposes the real financial and operational toll of poor risk management—and why most businesses underestimate it.

—

1. The Direct Financial Costs: Where the Money Leaks

A. Unexpected Losses from Operational Failures

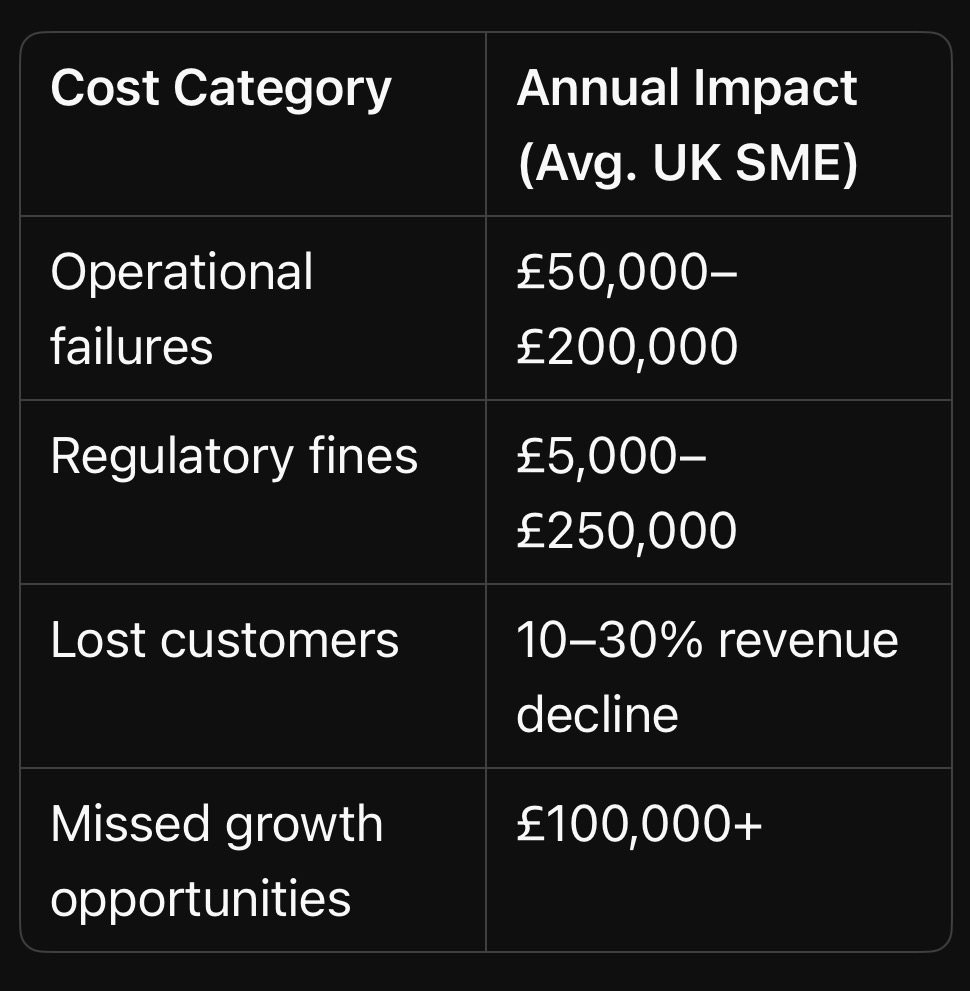

Example: A manufacturing firm ignores equipment maintenance, leading to a breakdown that halts production for 48 hours. The result? £250,000 in lost revenue + £50,000 in emergency repairs.

Stat: Companies with weak operational risk management see 30% higher unexpected costs (Deloitte).

B. Regulatory Fines & Legal Penalties

Case Study: A UK SME in financial services fails to comply with GDPR, resulting in a £180,000 fine —plus reputational damage.

Stat: 60% of small UK businesses aren’t fully compliant with key regulations (FSB).

Key Takeaway: Poor risk management isn’t just about avoiding disasters — it’s a tax on profitability, growth, and survival.

—

Actionable Insight: Audit one high-cost risk in your business this week (e.g., late payments, compliance gaps). What’s it really costing you?*

—

Chapter 2: The True Cost of Operational Failures – How Inefficient Risk Management Cripples Your Business

Introduction: The Domino Effect of Poor Operational Risk Controls

Operational risks don’t just cause one-off incidents—they trigger chain reactions that drain cash, demoralise teams, and erode customer trust. This chapter exposes the hidden, cascading costs of mismanaged operational risks and why most businesses only see the tip of the iceberg.

—

1. The Obvious Costs: What You Can’t Ignore

A. Downtime & Lost Production

Manufacturing Example: A single machine failure halts a production line for 8 hours → £25,000 in lost output + overtime costs to catch up.

Hospitality Example: A restaurant’s refrigeration breakdown spoils £3,000 of stock overnight — plus angry customers.

Stat: UK manufacturers lose £180 billion/year to unplanned downtime (EEF).

B. Emergency Repairs & Rush Orders

Reactive spending costs 3–5X more than planned maintenance.

Case Study: A logistics firm ignores fleet maintenance → two vans fail MOTs simultaneously → £8k in last-minute rentals + delayed deliveries.

C. Waste & Rework

Construction Example: Poor quality control leads to £50,000 of defective materials — then doubles labour costs to fix errors.

Stat: 20–30% of project budgets are wasted on rework (KPMG).

—

2. The Hidden Costs: What You’re Not Tracking (But Should Be)

A. Employee Productivity Drain

Scenario: A retail store’s outdated inventory system causes daily stock discrepancies. Staff waste 4 hours/day manually reconciling data instead of selling.

Stat: UK workers spend 15% of their time fixing preventable issues (PwC).

B. Management Distraction & Burnout

Small Business Reality: The owner spends 60% of their week putting out fires (supplier delays, IT crashes) instead of growing the business.

Psychological Cost: Chronic stress → poor decisions → more risks.

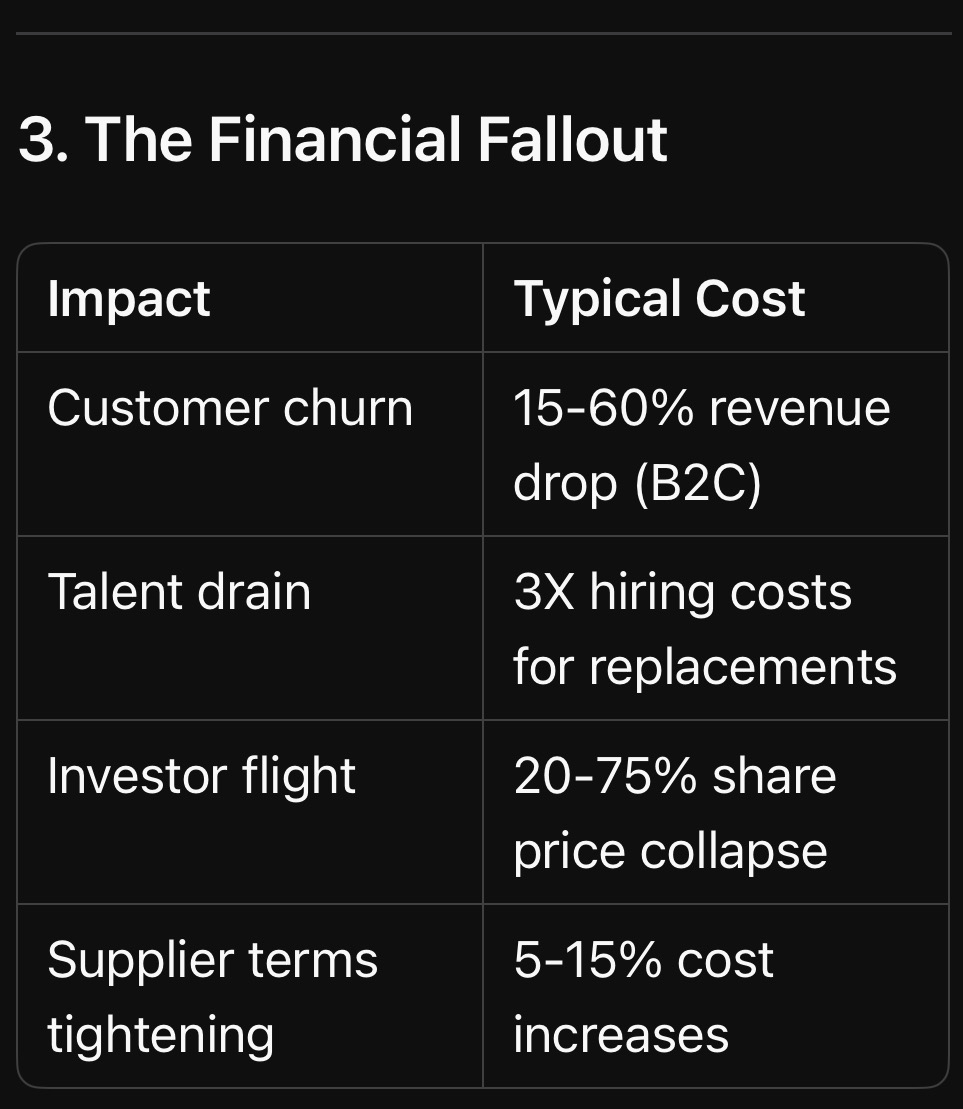

C. Customer Churn & Reputation Erosion

E-commerce Example: A fulfilment centre’s picking errors lead to 10% of orders arriving wrong → 15% of customers never return.

Stat: 70% of customers switch brands after just 2–3 bad experiences (Salesforce).

—

3. The Strategic Costs: How Operational Risks Stunt Growth

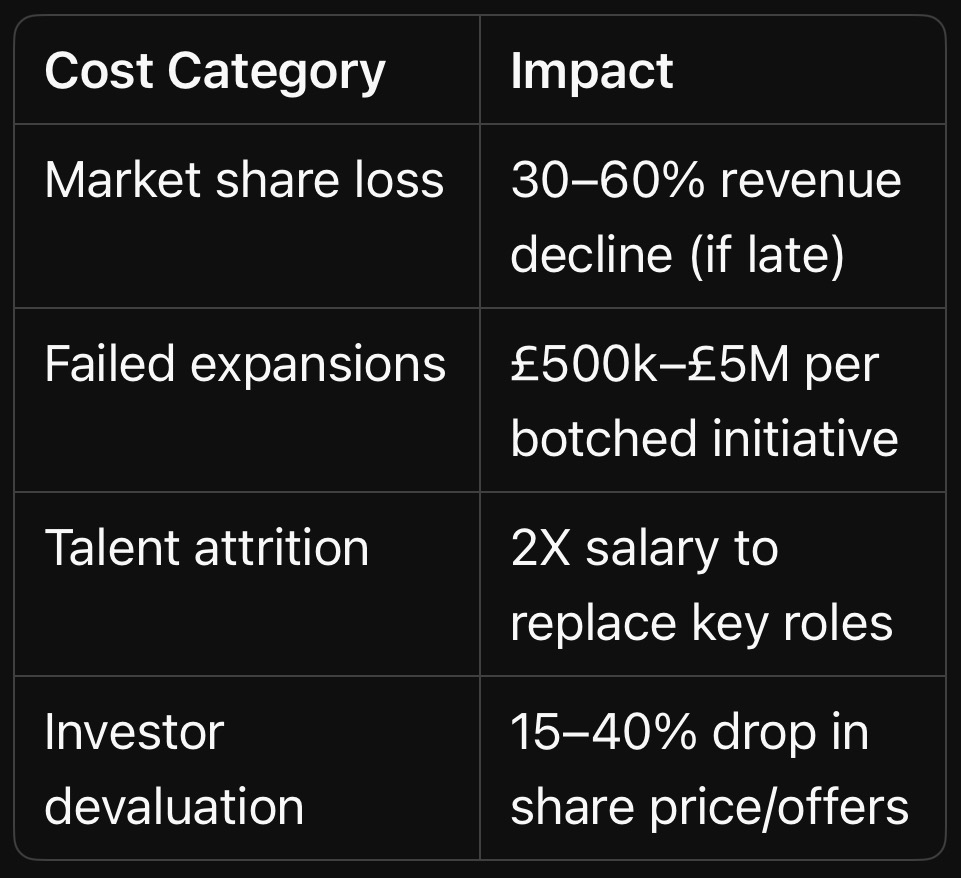

A. Lost Competitive Advantage

Case Study: A UK bakery’s unreliable oven delays a product launch by 3 months —competitors dominate supermarket shelves first.

B. Innovation Paralysis

Teams stuck in “firefighting mode” never test new ideas.

Example: A tech firm’s IT team spends 80% of time fixing outages → zero R&D progress.

C. Investor & Partner Distrust

Supply Chain Example: A fashion brand’s repeated delivery failures lead to two major retailers dropping them —£500k annual revenue gone.

—

4. The Survival Threat: When Operational Risks Become Fatal

A. Cash Flow Death Spiral

Construction Firm Case Study:

1. Poor contract risk assessment → unpaid invoices pile up

2. Equipment breakdown → project delays

3. Penalties for late delivery → bank calls in loan Result: Administration within 6 months.

B. The Carillion Effect

How ignoring operational risks (contract mismanagement, cash flow gaps) led to the UK’s biggest corporate collapse.

—

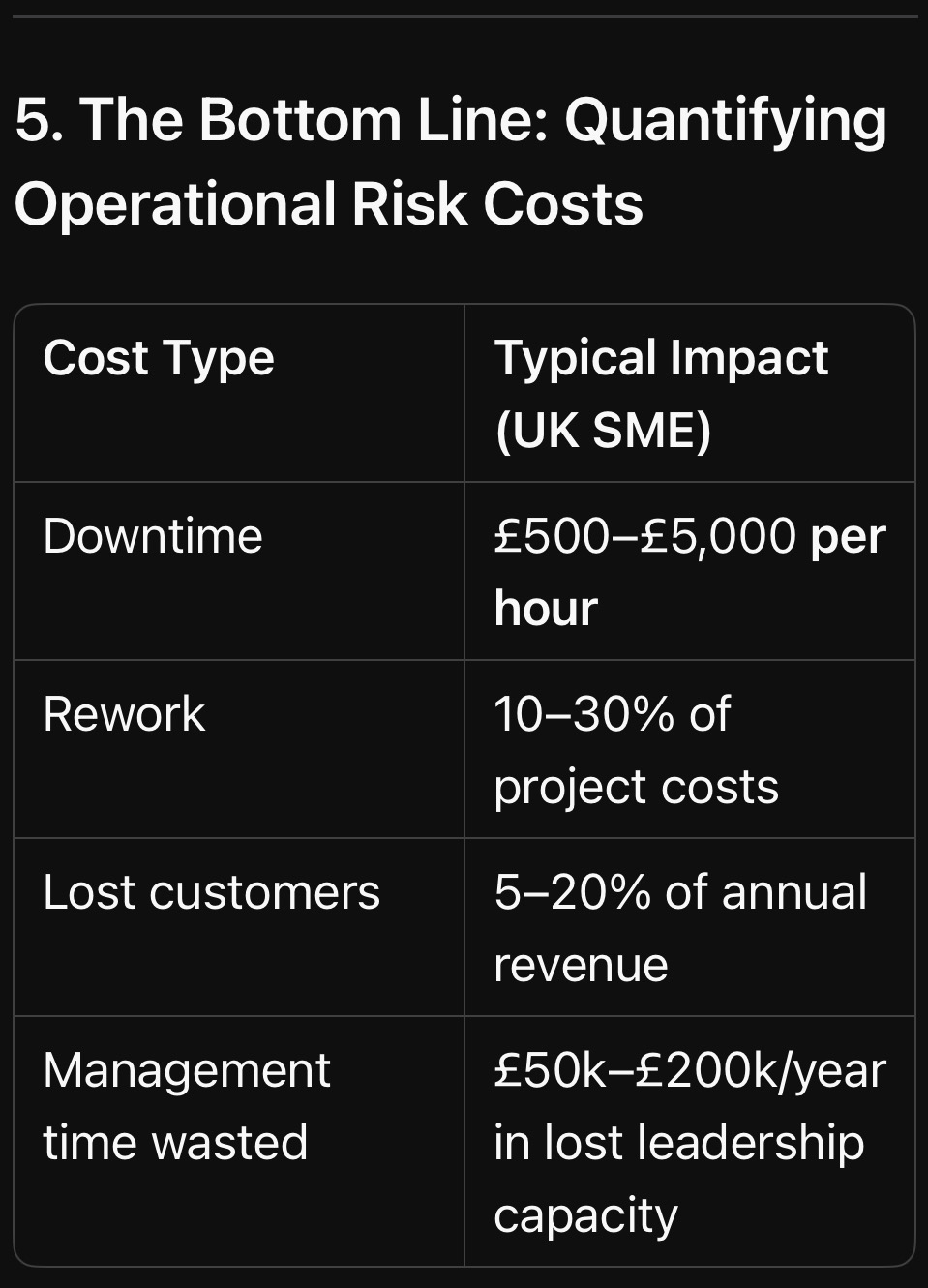

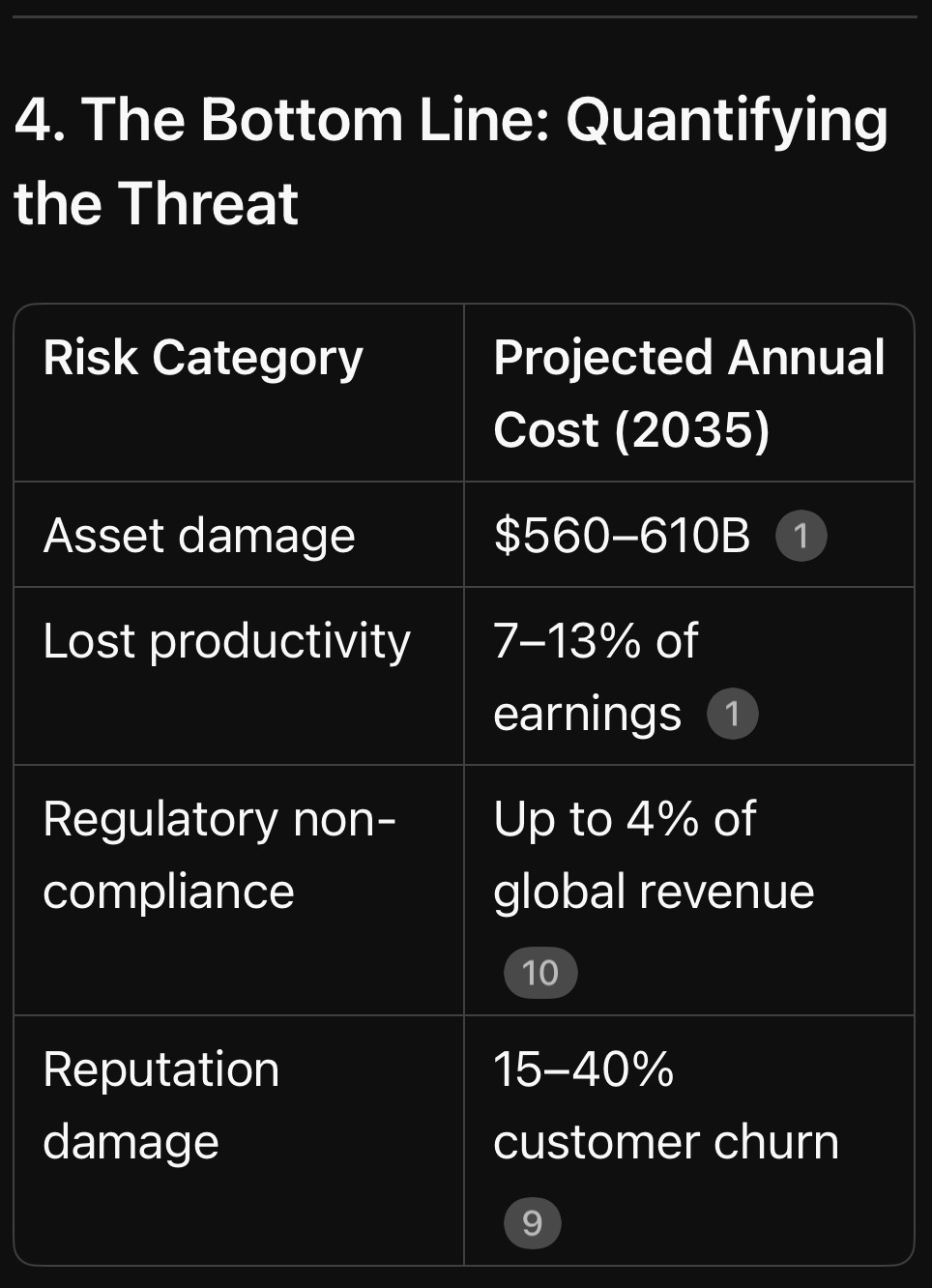

5. The Bottom Line: Quantifying Operational Risk Costs

Key Insight: Operational risks don’t just cost money—they steal time, talent, and future opportunities.

—

More From BusinessRiskTV Business Experts Hub : How to Fix It

We explore how to turn operational risk management into a profit centre, including:

The 5-minute daily habit that prevents 80% of failures

How to engage frontline teams in risk reduction (with real-world examples)

Actionable Task: Map one critical operational process (e.g., order fulfilment). Where could a single failure cost you £10k+?

—

Chapter 3: Strategic Risks – How Blind Spots in Planning Can Bankrupt Even Profitable Businesses

Introduction: The Silent Assassin of Business Growth

Strategic risks don’t announce themselves with alarms — they creep in unnoticed while leadership is distracted by day-to-day operations. By the time the damage is visible, it’s often too late to pivot. This chapter exposes how poor strategic risk management destroys market position, erodes competitive edge, and turns industry leaders into cautionary tales.

—

1. What Are Strategic Risks? (And Why They’re Different)

Key Takeaway: Strategic risks don’t just hurt profits — they erase entire business models.

—

More from BusinessRiskTV Business Experts Hub : How to Anticipate & Outmanoeuvre Strategic Risks

We explore practical frameworks to:

Spot industry shifts early (using weak signals)

Stress-test your strategy against disruption

Turn risks into opportunities (like Amazon’s pivot from books to cloud)

Actionable Task: List one strategic assumption your business relies on (e.g., “Customers will always prefer X”). How would you survive if it’s wrong?

—

Chapter 4: Financial Risks – How Poor Cash Flow & Debt Management Can Sink Your Business Overnight

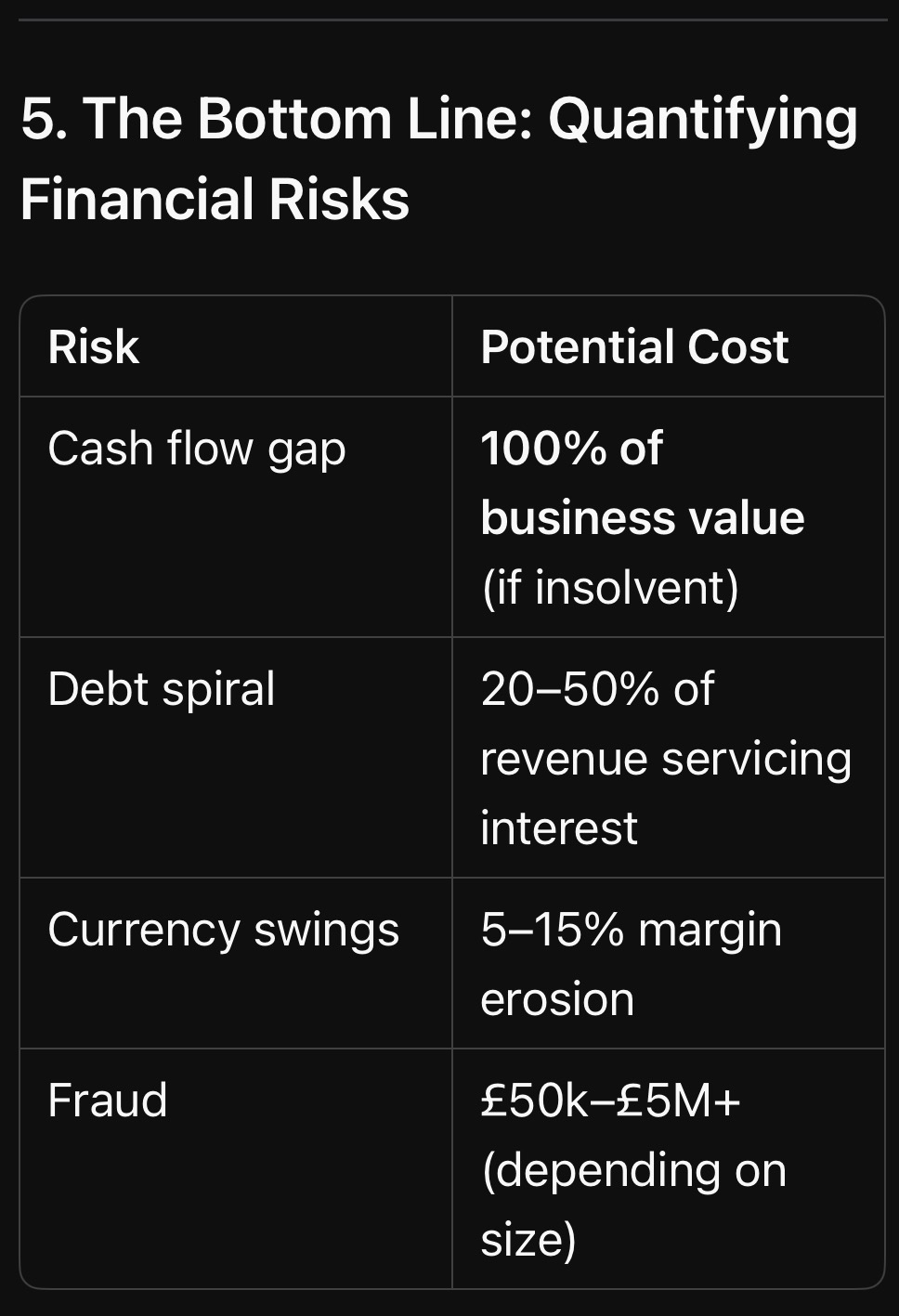

Introduction: The Silent Killer of Healthy Businesses

Profit doesn’t equal survival. Thousands of UK businesses post record revenues—right before going bust. Why? Because financial risk management isn’t about counting pennies — it’s about anticipating traps that strangle cash flow, trigger defaults, and collapse supply chains.

This chapter exposes the lethal financial risks hiding in plain sight — and why even profitable companies run out of money.

—

1. The Obvious (But Ignored) Financial Risks

A. Cash Flow Crises – The #1 Business Killer

Reality: 82% of UK business failures cite cash flow problems as the primary cause (UK Insolvency Service).

Example: A £5M-turnover construction firm collapses because:

– Client pays invoices 90 days late

– Supplier demands upfront payments due to past delays

– Bank rejects emergency loan Result: Liquidation despite £1.2M in “paper profits.”

B. Debt Avalanches – When Borrowing Backfires

Case Study: A fast-growing e-commerce firm takes on high-interest debt to fund inventory. Sales dip, interest compounds, and suddenly 60% of revenue services debt.

– Stat: 40% of UK SMEs struggle with unmanageable debt (Bank of England).

C. Currency & Commodity Swings

Example: A UK bakery’s flour costs jump 30% after a wheat shortage. Contracts lock in prices — margins vanish overnight.

—

2. The Hidden Financial Risks That Compound Quietly

A. Customer Concentration Risk

Scenario: A B2B software firm gets 70% of revenue from one client. When that client leaves, payroll can’t be met.

Rule of Thumb: No single client should exceed 15–20% of revenue.

B. Supplier Dependency & Price Shocks

Case Study: A car manufacturer relies on one battery supplier. When shortages hit, production stalls for 3 months → £9M loss.

C. Fraud & Financial Mismanagement

Stat: UK businesses lose £137B yearly to fraud, waste, and accounting errors (PwC).

Example: A finance director “cooks the books” — investors pull out when the truth surfaces.

—

3. The Strategic Fallout: When Financial Risks Spiral

A. Credit Downgrades & Banking Nightmares

Example: A once-stable firm misses a loan covenant — interest rates spike 5%, lines of credit freeze.

B. Investor Panic & Equity Crashes

Case Study: A tech startup’s burn rate exceeds projections — VCs demand emergency restructuring, slashing valuation by 50%.

C. Employee Exodus (When Paychecks Bounce)

Stat: 78% of employees leave within 6 months of payroll issues (CIPD).

—

4. The Ultimate Cost: Bankruptcy Dominoes

A. The “Profitable But Insolvent” Paradox

How It Happens:

1. Big contracts signed → revenue looks strong

2. Clients pay late → cash dries up

3. Suppliers demand payment → no money for salaries/tax

4. HMRC forces liquidation despite “growth.”

B. The Carillion Effect (Again)

£7B collapse triggered by:

– Aggressive accounting

– Reliance on unsustainable contracts

– No cash buffer for delays

Key Insight: Financial risks don’t just reduce profits — they erase businesses in weeks.

—

More from BusinessRiskTV Business Experts Hub : How to Fix It

We explore real-world financial risk strategies, including:

The 13-week cash flow rule (used by turnaround experts)

How to renegotiate debt before it’s too late

Building a “war chest” for crises

Actionable Task: Run a “stress test” on your cash flow: What if 2 clients pay 60 days late?

—

Chapter 5: Cyber Risks – The Invisible Threat That Could Bankrupt Your Business by Breakfast

Introduction: The Digital Time Bomb Ticking in Your Business

Imagine arriving at work to find:

Your customer database on the dark web

Fraudsters draining £250,000 from your account

Ransomware locking every file until you pay Bitcoin

This isn’t a movie plot — it’s Monday morning for thousands of UK businesses. Cyber risks don’t just steal data; they extort cash, destroy reputations, and trigger regulatory hell. And here’s the worst part: Most victims never see it coming until the damage is done.

—

1. The Direct Costs: What Happens When Cybercrime Hits

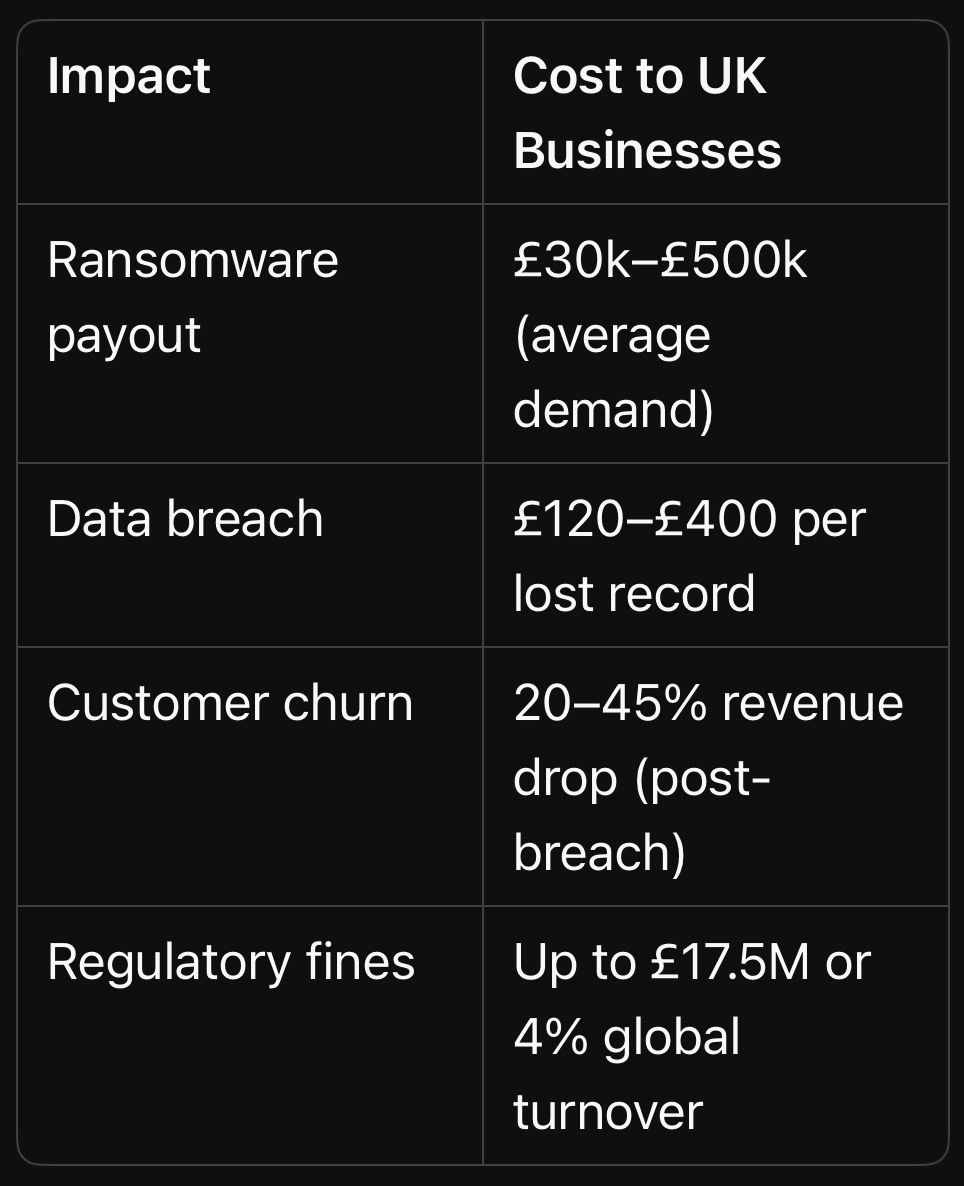

A. Ransomware: The Digital Kidnapping Epidemic

2023 Reality: A UK construction firm’s blueprints, invoices, and payroll systems encrypted. Hackers demand £120,000 to unlock files.

Stat: 73% of UK businesses hit by ransomware in 2023 (NCSC).

Brutal Truth: Paying doesn’t guarantee recovery — 32% never get full data back (Sophos).

B. Data Breaches: When Your Customers Become Victims

Case Study: A mid-sized retailer’s poorly secured e-commerce platform leaks 380,000 credit cards.

£500,000 GDPR fine

£1.2M in fraud reimbursements

22% customer churn

Stat: Average UK data breach cost: £3.4 million (IBM).

C. Business Email Compromise (BEC): The Silent Heist

How It Works: A hacker impersonates your CEO, emails finance: “Urgent: Transfer £80k to new supplier.”

UK Losses: £1.3 billion stolen via BEC in 2023 (UK Finance).

—

2. The Hidden Costs That Cripple You Later

A. Reputation Freefall & Customer Exodus

After a breach:

– 58% of customers avoid breached brands (Verizon)

– Recovery Cost: 3–5X more on marketing to rebuild trust

B. Operational Paralysis

Example: A law firm’s servers go down for 72 hours post-attack. £350k in billable hours lost + client lawsuits.

C. Insurance Nightmares

Post-Claim Realities:

– Premiums triple

– Mandatory audits drain management time

– Some policies simply won’t renew

—

3. The Strategic Fallout: Long-Term Business Damage

A. Lost Contracts & Blacklisting

Government/Corporate Tenders Now Demand:

– Cyber Essentials Certification (missing? Disqualified automatically)

– Proof of incident response plans

B. Investor Flight

Startup Killer: A fintech’s pre-IPO breach scares off VCs, slashing valuation by 60%.

C. Director Liability (Yes, You Can Go to Jail)

UK Law: Under GDPR & NIS Directive, negligent executives face fines up to £17.5M or 4% of global revenue — plus disqualification.

—

4. Why Cyber Risks Are Worse Than You Think

A. It’s Not Just “Big Targets”

61% of UK attacks hit SMEs (Verizon) — hackers bet they’re unprepared.

B. Remote Work = 300% More Attack Surfaces

Example: An employee’s compromised home laptop gives hackers access to your entire CRM.

C. AI-Powered Attacks Are Here

New Threat: Deepfake audio of your CFO “calling” finance to wire funds.

Key Insight: Cyber risks aren’t an “IT problem” — they’re an existential business threat.

—

More from BusinessRiskTV Business Experts Hub : How to Fight Back

We will explore real-world cyber defenses, including:

The 5-step SME ransomware shield (costs <£5k/year)

– How to trick hackers into avoiding you (attackers prefer easy targets)

– Turning employees into human firewalls

Actionable Task: Run this free test now: [Have I Been Pwned](https://haveibeenpwned.com/) to check if your work emails are already in hacker databases.

—

Chapter 6: Human Risks – When Your Greatest Asset Becomes Your Biggest Liability

Introduction: The Enemy Inside Your Walls

Your employees can either be your strongest defence — or your weakest link. Negligence, disengagement, and malicious actions cost UK businesses £30 billion annually (ACAS). This chapter exposes how poor people risk management leads to:

– Catastrophic errors

– Culture collapse

– Regulatory disasters

– Fraud epidemics

And why traditional HR policies fail to prevent 89% of these risks (PwC).

—

1. The Obvious (But Ignored) Human Risks

A. The High Cost of Disengagement

Example: A retail chain’s apathetic staff miss 40% of shoplifting incidents —costing £220,000/year in stolen stock.

Stat: Disengaged employees are 450% more likely to cause operational errors (Gallup).

B. Turnover Tsunamis

Case Study: A tech firm’s toxic culture drives out 7 senior engineers in 6 months — delaying a £2M product launch by 11 months.

Replacement Cost: Up to 2X annual salary per lost employee (Oxford Economics).

C. Training Gaps That Become Legal Nightmares

Reality Check: A warehouse worker badly operates a forklift, causing £80k in damages + HSE fines—because “training was just a 10-minute video.”

—

2. The Hidden (But More Dangerous) Human Risks

A. Insider Threats: When Employees Attack

Shocking Stat: 58% of data breaches involve insiders (Verizon).

Methods:

– The Malicious: IT admin sells customer data (£50k on dark web)

– The Careless: Accountant emails payroll files to personal Gmail

B. Culture Risks: How Toxicity Spreads

Example: A sales team’s “win at all costs” mentality leads to fraudulent client promises — £600k in lawsuits + FCA investigation.

C. Leadership Blind Spots

CEO Overconfidence: Ignoring team warnings about a flawed expansion → £3M write-off.

Stat: 82% of business failures trace back to poor leadership decisions (KPMG).

—

3. The Strategic Fallout: When People Risks Sink Companies

A. The Volkswagen Emissions Scandal

Root Cause: A culture where “nobody dared question” fraudulent engineering.

– Cost: €32 billion in fines/losses + permanent brand damage.

B. The Barclays CEO Scandal

How It Happened: Leadership’s obsession with “star hires” led to unchecked bullying — triggering £1M fines + investor revolt.

C. The Everyday SME Killer

Scenario: Your “trusted” bookkeeper embezzles £150k over 3 years — exposed only during a tax audit.

—

4. Why Traditional Approaches Fail

Annual compliance training?86% of employees forget it within 30 days (MIT).

“Hotline whistleblowing”?62% of staff fear retaliation (EY).

Top-down policies? Frontline teams see them as “head office nonsense.”

Key Insight: Your employees create or destroy value daily — often without realising it.

—

More from BusinessRiskTV Business Experts Hub : How to Transform Human Risk into Advantage

We explore battle-tested solutions, including:

The “Psychological Safety” hack

How to spot insider threats before they strike

Turning compliance into competitive edge

Actionable Task: Run a 5-minute “risk culture pulse check” with your team this week: “What’s one process you think could fail catastrophically?”

—

Chapter 7: Supply Chain Risks – The Fragile Web That Could Strangle Your Business Overnight

Introduction: Your Business Is Only as Strong as Its Weakest Supplier

A single delayed shipment. One insolvent vendor. A geopolitical shockwave. Suddenly, your production line stops, customers revolt, and cash flow evaporates.

Key Insight: Supply chains have become the ultimate leverage point — for your competitors or your downfall.

—

More from BusinessRiskTV Business Experts Hub : How to Build an Unbreakable Supply Chain

We explore wartime-tested strategies, including:

The “3D Supplier Mapping” trick (used by Special Forces logisticians)

How to turn suppliers into partners (not adversaries)

When to nearshore/onshore without bankrupting yourself

Actionable Task: Identify one “critical” supplier you couldn’t operate without. How would you survive if they vanished tomorrow?

—

Chapter 8: Reputational Risks – When Trust Collapses Faster Than Your Share Price

Introduction: The 24-Hour Business Execution

A single tweet. One viral video. A disgruntled employee’s LinkedIn post. In today’s digital wildfire, your hard-earned reputation can evaporate before your crisis team finishes their first coffee.

The brutal reality:

87% of consumers will abandon a brand after a reputation crisis (YouGov)

It takes 4-7 years to build trust but just 4 bad days to destroy it (Edelman Trust Barometer)

65% of a company’s market value is tied to intangible assets like reputation (Ocean Tomo)

This isn’t about PR spin – it’s about preventing the preventable and surviving the unpredictable.

—

1. The Obvious Reputation Killers

A. Social Media Firestorms

Case Study: A restaurant manager’s racist comment caught on video → 300,000 angry tweets in 48 hours → permanent 40% revenue drop

Stat: Viral crises spread 20x faster than management can respond (MIT Sloan)

B. Executive Scandals

The P&G CEO Effect: A $375 billion company lost $40B in market cap in days after CEO’s inappropriate relationship surfaced

“No comment” = “We’re guilty” in public perception

Corporate-speak increases distrust by 41% (Edelman)

Legal-first responses often worsen the crisis

—

5. The Survival Playbook (Preview)

More from BusinessRiskTV Business Experts Hub we will explore modern reputation armour, including:

The “Dark Web Early Warning” system (catch crises before they explode)

Turning employees into reputation ambassadors