Navigating Uncertainty: 12 Risk Management Strategies for Business Leaders in a Sahm Rule Shadow

As a U.S. economics expert, I’m keenly aware of the whispers surrounding a potential recession. The Sahm Rule, a recession indicator with a perfect track record since 1960, is raising eyebrows. While not a definitive predictor, its current proximity to triggering a recession signal warrants a proactive approach from business leaders.

The Sahm Rule, developed by former Federal Reserve economist Claudia Sahm, suggests a recession is likely when the three-month moving average of the unemployment rate climbs 0.5 percentage points above its low point in the prior twelve months. As of April 2024, the unemployment rate has ticked upwards, and while it hasn’t yet triggered the Sahm Rule, the possibility hangs in the air.

This economic uncertainty necessitates a robust risk management strategy. Here are 12 key areas business leaders should focus on:

1. Stress Test Your Finances: Conduct a thorough financial stress test. Simulate various economic scenarios, including a mild recession, to understand your company’s ability to weather a downturn. Identify potential cash flow shortages and explore contingency plans like raising capital or reducing expenses.

2. Prioritise Cash Flow Management: Cash is king, especially during economic turbulence. Focus on optimising your cash conversion cycle by collecting receivables faster and negotiating longer payment terms with suppliers. Implement stricter expense controls and prioritise essential spending.

3. Inventory Optimisation: Review your inventory levels and consider implementing a just-in-time (JIT) inventory management system. This minimises storage costs and reduces the risk of holding obsolete inventory during a potential slowdown.

4. Diversify Your Customer Base: Don’t rely on a single customer segment or market. Broaden your customer base by exploring new markets, product lines, or customer demographics. This helps mitigate risk if one segment experiences a downturn.

5. Revisit Pricing Strategies: Carefully evaluate your pricing strategy. You may need to adjust prices to maintain profitability while remaining competitive. Consider offering tiered pricing or promotions to attract budget-conscious customers.

6. Workforce Optimisation: Analyse your workforce needs and implement cost-saving measures without sacrificing productivity. Consider flexible work arrangements, upskilling current employees, or temporary staffing solutions.

7. Strengthen Supplier Relationships: Building strong relationships with suppliers can be invaluable during a recession. Negotiate favourable payment terms and explore opportunities for collaboration to streamline processes and reduce costs.

8. Enhance Communication: Open and transparent communication is crucial during uncertain times. Regularly update your employees, customers, and investors on your business strategy and how you’re navigating the economic climate.

9. Embrace Technology: Technology can be a powerful tool for efficiency and cost savings. Explore automation opportunities, cloud-based solutions, and data analytics tools to optimise operations and improve decision-making.

10. Focus on Customer Retention: It’s always cheaper to retain existing customers than acquire new ones. Invest in customer service, loyalty programs, and personalised marketing initiatives to keep your customers engaged.

11. Build Brand Resilience: A strong brand reputation can create a buffer during economic downturns. Focus on building brand loyalty and trust by delivering exceptional customer experiences.

12. Scenario Planning: Engage in scenario planning to prepare for various economic possibilities. This allows you to adapt quickly and make informed decisions, regardless of the economic climate.

Beyond the Sahm Rule:

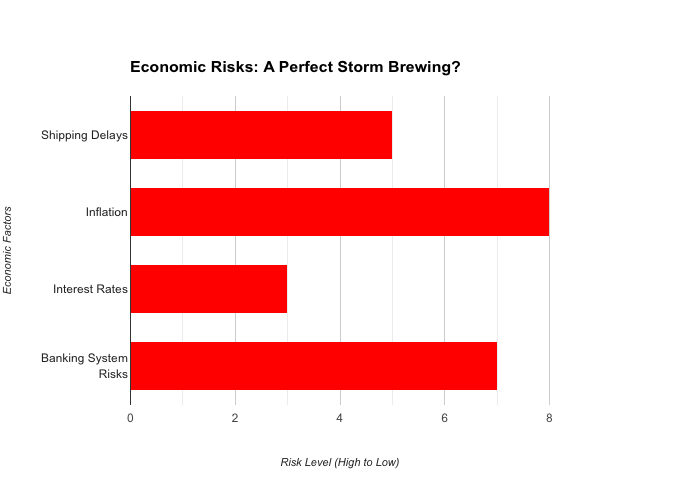

While the Sahm Rule is a valuable indicator, it’s not the only factor to consider. Keep a close eye on other economic indicators like inflation, consumer spending, and Federal Reserve policy. Regularly monitor industry trends and competitor activity to stay ahead of the curve.

Conclusion:

The current economic environment necessitates a proactive and strategic approach from business leaders. By incorporating these risk management strategies and staying informed, you can position your company to weather potential economic storms and emerge stronger on the other side. Remember, a well-prepared and adaptable business is better equipped to navigate any economic uncertainty, be it a mild slowdown or a more significant recession.

Get help to protect and grow your business

Subscribe for free business risk alerts and risk reviews

Read more business risk management articles