The Bank of England’s recent record £87.15 billion repo allotment, a tool used to provide liquidity to banks as the central bank reduces its bond holdings, could signal underlying stress in the UK banking sector. This growing reliance on the central bank for funds raises a red flag for the financial stability and economic safety of the UK. Discover what this means for the wider economy and learn six crucial risk management strategies every business leader should implement now to protect and grow their enterprise more resiliently in an uncertain economic climate.

Bank of England Allots Record £87.15 Billion in Repo Operation: What It Means for UK Business Risk

The Bank of England’s Record Repo Allotment: A Warning for UK Business? 🚨

The Bank of England recently allotted a record £87.15 billion in a short-term repo operation, a move that provides a substantial injection of liquidity into the UK’s banking system. While this may seem like a routine technical adjustment by the central bank, the increasing reliance on these operations could be a significant red flag for the safety of the UK’s financial system and wider economy.

What Is a Repo Operation and Why Is This a Red Flag?

A repo (repurchase agreement) is essentially a short-term loan. The Bank of England lends money to commercial banks and in return, the banks provide high-quality assets (like government bonds) as collateral. The Bank’s increasing use of this tool is directly linked to its Quantitative Tightening (QT) programme, which involves selling off the government bonds it bought during the era of Quantitative Easing (QE). The purpose of these repo operations is to prevent a potential liquidity squeeze in the financial system as the central bank reduces its balance sheet.

The record allotment is a red flag for a few key reasons:

Growing Illiquidity: The fact that banks are demanding a record amount of funds from the central bank suggests they may be struggling to find liquidity elsewhere in the market. This could indicate underlying stress in the banking sector and a reluctance among banks to lend to each other.

Systemic Risk: This reliance on the Bank of England for funding could be a sign of increased systemic risk. If a major bank were to face a sudden liquidity crisis, the central bank would be its lender of last resort. The increasing size of these operations shows the potential scale of that reliance.

Uncertainty and Instability: A record-breaking allotment, particularly one that exceeds a recent record, creates a narrative of growing instability. This can erode confidence in the banking system and the wider economy, making businesses and investors more hesitant to spend and invest. This uncertainty trickles down to businesses and consumers, affecting everything from investment decisions to household spending.

6 Risk Management Measures for Businesses

In an environment of economic uncertainty, business leaders must be proactive to protect their organisations. Here are six essential risk management measures to enhance resilience:

Strengthen Cash Flow and Liquidity:Cash is king, especially in a downturn. Focus on optimising your working capital by accelerating accounts receivable, negotiating longer payment terms with suppliers, and maintaining a healthy cash reserve. Create detailed cash flow forecasts to anticipate potential shortfalls and manage expenses.

Diversify Revenue Streams and Supply Chains:Over-reliance on a single product, service, customer, or supplier is a major vulnerability. Actively seek new markets, customer segments, and partnerships. For your supply chain, identify alternative vendors and consider strategies like near-shoring or holding a small buffer of critical inventory to mitigate potential disruptions.

Manage Debt and Capital Expenditure Wisely: During uncertain times, it is crucial to avoid taking on excessive debt. Evaluate all major capital expenditure projects. Postpone or cancel non-essential investments that don’t directly contribute to immediate revenue or operational efficiency.

Review and Optimise Operational Costs:Take a hard look at all business expenses. Eliminate unnecessary costs without sacrificing the quality of your product or service. This could involve renegotiating contracts, leveraging technology for greater efficiency, or consolidating services. The goal is to create a leaner, more resilient cost structure.

Why the Bank of England’s Record Repo Allotment Is a Red Flag

The Bank of England’s record-breaking repo allotment is a significant red flag because it points to potential underlying stress and growing liquidity issues within the UK banking system. While repo operations are a standard tool for central banks to manage monetary policy, the increasing size of these allotments, especially in the context of the central bank’s quantitative tightening (QT) programme, reveals a deeper problem.

Growing Illiquidity and Inter-bank Distrust: The primary role of a central bank’s repo operation is to provide liquidity. A record amount being requested by commercial banks suggests they are struggling to secure the funds they need from each other. In a healthy banking system, banks would lend to one another in the inter-bank market. The fact that they are turning to the Bank of England in such high volumes could indicate a breakdown of trust between financial institutions, which is a classic symptom of a stressed system.

Systemic Risk: The increasing reliance on the central bank for funding raises concerns about systemic risk. Systemic risk is the risk of a collapse of an entire financial system due to the failure of one or more institutions. If a significant portion of the banking sector is dependent on the Bank of England for liquidity, a sudden shock or disruption could have a cascading effect across the entire system. This over-reliance makes the financial system less resilient and more vulnerable to unforeseen events.

Uncertainty and Economic Instability: A record repo allotment creates a sense of uncertainty and instability in the market. The public and investors may interpret this as a signal that the banking system is not as robust as it appears. This loss of confidence can have a tangible impact on the wider economy. It can lead to a tightening of lending standards, making it harder for businesses and households to access credit, and it can also deter investment, ultimately slowing down economic growth. The large allotment, therefore, isn’t just a technical exercise; it’s a barometer of growing financial vulnerability in the UK.

Read more free business risk management articles and view videos

6 Essential Business Risk Management Measures for UK Business Leaders

In today’s complex and uncertain economic environment, proactive business risk management is no longer an option—it’s a necessity. UK business leaders must move beyond a reactive approach and build genuine resilience into the core of their operations. Here are six essential measures to take action on now.

Optimise working capital: Focus on accelerating accounts receivable by offering incentives for early payment or enforcing stricter payment terms. At the same time, negotiate more favourable payment terms with your suppliers to extend your accounts payable.

Create robust cash flow forecasts: Use financial modelling and scenario planning to predict potential cash shortfalls. This will help you anticipate problems and give you time to secure financing or make cost adjustments before a crisis hits.

Maintain a cash reserve: Aim to build a buffer of cash sufficient to cover at least three to six months of operating expenses. This reserve acts as a critical safety net against unexpected disruptions.

2. Diversify Revenue Streams and Supply Chains

Over-reliance on a single customer, product, or supplier is a major vulnerability. Diversification builds a more robust and flexible business model.

Review and diversify your supply chain: Identify and vet alternative suppliers, especially for critical raw materials or components. Consider a dual-sourcing model or incorporating local suppliers to mitigate risks from global transport issues or geopolitical events.

3. Conduct Scenario Planning and Stress Testing

Don’t wait for a crisis to expose your weaknesses. Proactive scenario planning allows you to test your business model against a range of potential threats.

Identify key risks: Create a comprehensive risk register that outlines potential risks (e.g., economic downturn, supply chain disruption, cyber-attack) and their potential impact.

High levels of debt can become a significant burden in a tightening credit environment.

Limit new borrowing: Be cautious about taking on new debt, particularly for non-essential projects. Evaluate every borrowing decision based on its potential return on investment and its impact on your balance sheet.

Re-evaluate capital projects: Postpone or cancel major capital expenditures that are not critical for business operations or do not have a clear and immediate path to profitability. Prioritize investments that enhance operational efficiency and resilience.

5. Review and OPTIMISE Operational Costs

A lean and efficient cost structure improves profitability and allows you to better weather economic storms.

Targets decision-makers searching for the financial impact of weak risk practices

THE HIDDEN TAX OF POOR RISK MANAGEMENT

Your business is leaking money. Not in the obvious ways — like overspending or inefficiency — but in silent, insidious drains you might not even see. Poor risk management isn’t just about avoiding disasters; it’s a profit killer, a growth stifler, and, in the worst cases, an executioner of businesses that could have thrived.

Consider this: 30% of bankruptcies are due to operational failures that could have been mitigated with better risk practices (OECD). That’s not bad luck—it’s self-inflicted. And if you think your company is immune, think again.

This isn’t theoretical. Every day, businesses hemorrhage cash through:

Employee disengagement —teams that don’t see risk as their problem, costing you in errors, delays, and lost innovation.

The result? Lower profitability. Stunted growth. And, in extreme cases, extinction.

But here’s the good news: this is entirely optional and fixable.

In this e-book, we’ll expose the 12 most damaging costs of poor risk management —many of which you’re likely paying right now — and deliver 12 actionable solutions to turn risk from a liability into a competitive advantage. You’ll learn how to:

Engage every employee in risk ownership (not just compliance, but profit protection).

Stop financial bleed from preventable failures.

Turn risk-aware decision-making into a growth engine.

This isn’t another dry risk management manual. This is a survival guide for profitable, resilient business leadership.

Ready to plug the leaks? Let’s begin.

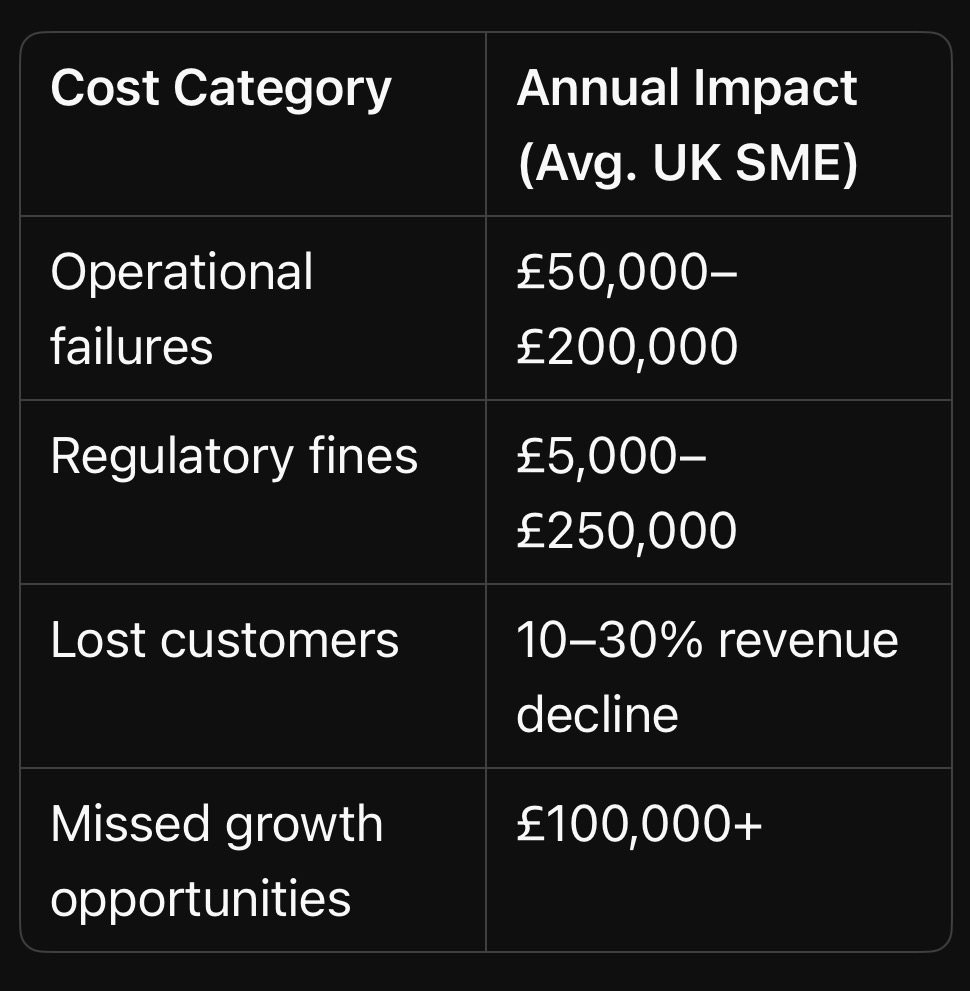

🚨 YOUR BUSINESS IS LEAKING £££ – FIND THE HOLES! 🚨

83% of UK SMEs lose £50k+ yearly from hidden risks they don’t even measure:

❌ Operational failures burning cash ❌Supply chain disasters killing margins

❌ Cyberattacks costing millions

BusinessRiskTV’s NEW eBook reveals:

✅ 12 PROVEN FIXES to stop profit leaks

✅ Real case studies from UK businesses

✅ Simple checklists to act TODAY

Chapter 1: The Hidden Costs of Poor Risk Management – How Ignoring Risk Erodes Your Profits and Threatens Survival

Introduction: The Silent Profit Killer

Every business faces risks—some obvious, others invisible. But when risk management is an afterthought, those risks don’t just linger; they multiply costs, shrink margins, and sabotage growth. This chapter exposes the real financial and operational toll of poor risk management—and why most businesses underestimate it.

—

1. The Direct Financial Costs: Where the Money Leaks

A. Unexpected Losses from Operational Failures

Example: A manufacturing firm ignores equipment maintenance, leading to a breakdown that halts production for 48 hours. The result? £250,000 in lost revenue + £50,000 in emergency repairs.

Stat: Companies with weak operational risk management see 30% higher unexpected costs (Deloitte).

B. Regulatory Fines & Legal Penalties

Case Study: A UK SME in financial services fails to comply with GDPR, resulting in a £180,000 fine —plus reputational damage.

Stat: 60% of small UK businesses aren’t fully compliant with key regulations (FSB).

Key Takeaway: Poor risk management isn’t just about avoiding disasters — it’s a tax on profitability, growth, and survival.

—

Actionable Insight: Audit one high-cost risk in your business this week (e.g., late payments, compliance gaps). What’s it really costing you?*

—

Chapter 2: The True Cost of Operational Failures – How Inefficient Risk Management Cripples Your Business

Introduction: The Domino Effect of Poor Operational Risk Controls

Operational risks don’t just cause one-off incidents—they trigger chain reactions that drain cash, demoralise teams, and erode customer trust. This chapter exposes the hidden, cascading costs of mismanaged operational risks and why most businesses only see the tip of the iceberg.

—

1. The Obvious Costs: What You Can’t Ignore

A. Downtime & Lost Production

Manufacturing Example: A single machine failure halts a production line for 8 hours → £25,000 in lost output + overtime costs to catch up.

Hospitality Example: A restaurant’s refrigeration breakdown spoils £3,000 of stock overnight — plus angry customers.

Stat: UK manufacturers lose £180 billion/year to unplanned downtime (EEF).

B. Emergency Repairs & Rush Orders

Reactive spending costs 3–5X more than planned maintenance.

Case Study: A logistics firm ignores fleet maintenance → two vans fail MOTs simultaneously → £8k in last-minute rentals + delayed deliveries.

C. Waste & Rework

Construction Example: Poor quality control leads to £50,000 of defective materials — then doubles labour costs to fix errors.

Stat: 20–30% of project budgets are wasted on rework (KPMG).

—

2. The Hidden Costs: What You’re Not Tracking (But Should Be)

A. Employee Productivity Drain

Scenario: A retail store’s outdated inventory system causes daily stock discrepancies. Staff waste 4 hours/day manually reconciling data instead of selling.

Stat: UK workers spend 15% of their time fixing preventable issues (PwC).

B. Management Distraction & Burnout

Small Business Reality: The owner spends 60% of their week putting out fires (supplier delays, IT crashes) instead of growing the business.

Psychological Cost: Chronic stress → poor decisions → more risks.

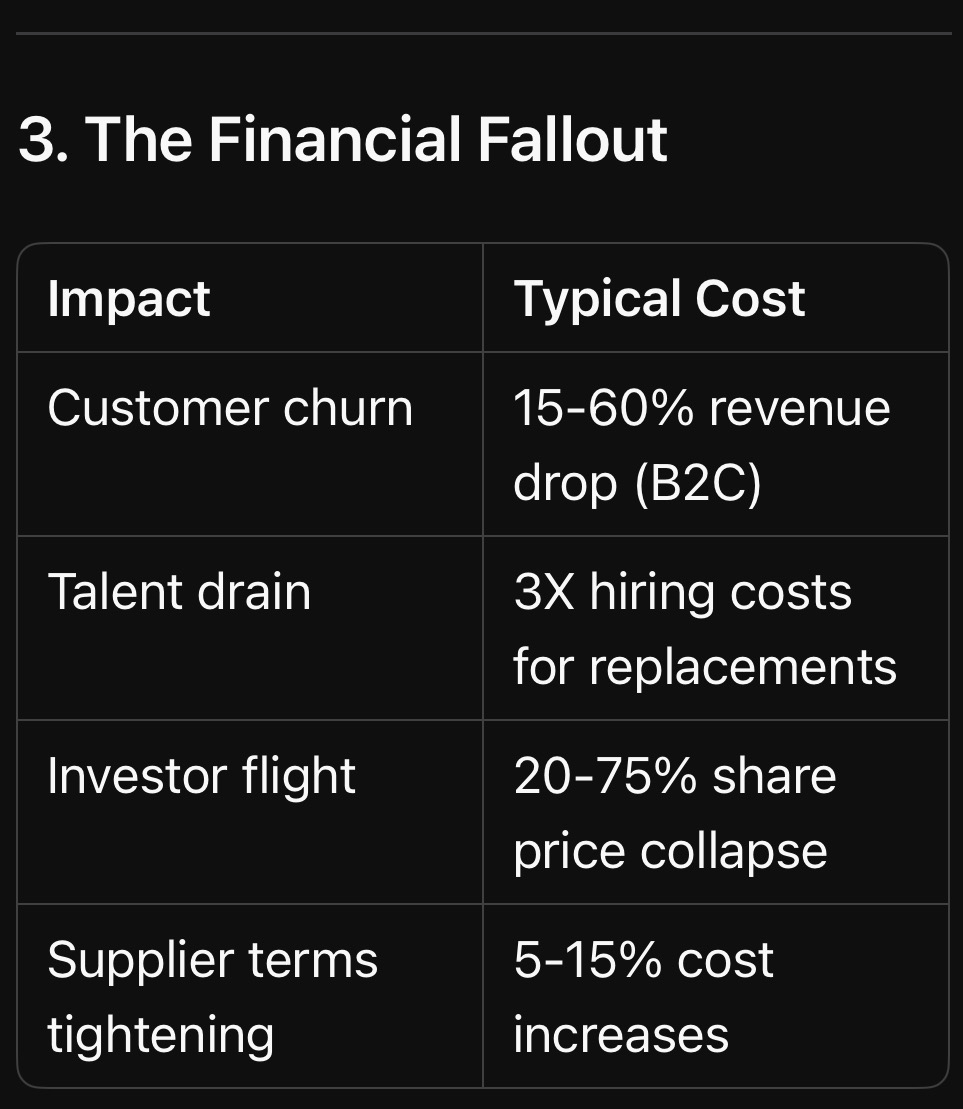

C. Customer Churn & Reputation Erosion

E-commerce Example: A fulfilment centre’s picking errors lead to 10% of orders arriving wrong → 15% of customers never return.

Stat: 70% of customers switch brands after just 2–3 bad experiences (Salesforce).

—

3. The Strategic Costs: How Operational Risks Stunt Growth

A. Lost Competitive Advantage

Case Study: A UK bakery’s unreliable oven delays a product launch by 3 months —competitors dominate supermarket shelves first.

B. Innovation Paralysis

Teams stuck in “firefighting mode” never test new ideas.

Example: A tech firm’s IT team spends 80% of time fixing outages → zero R&D progress.

C. Investor & Partner Distrust

Supply Chain Example: A fashion brand’s repeated delivery failures lead to two major retailers dropping them —£500k annual revenue gone.

—

4. The Survival Threat: When Operational Risks Become Fatal

A. Cash Flow Death Spiral

Construction Firm Case Study:

1. Poor contract risk assessment → unpaid invoices pile up

2. Equipment breakdown → project delays

3. Penalties for late delivery → bank calls in loan Result: Administration within 6 months.

B. The Carillion Effect

How ignoring operational risks (contract mismanagement, cash flow gaps) led to the UK’s biggest corporate collapse.

—

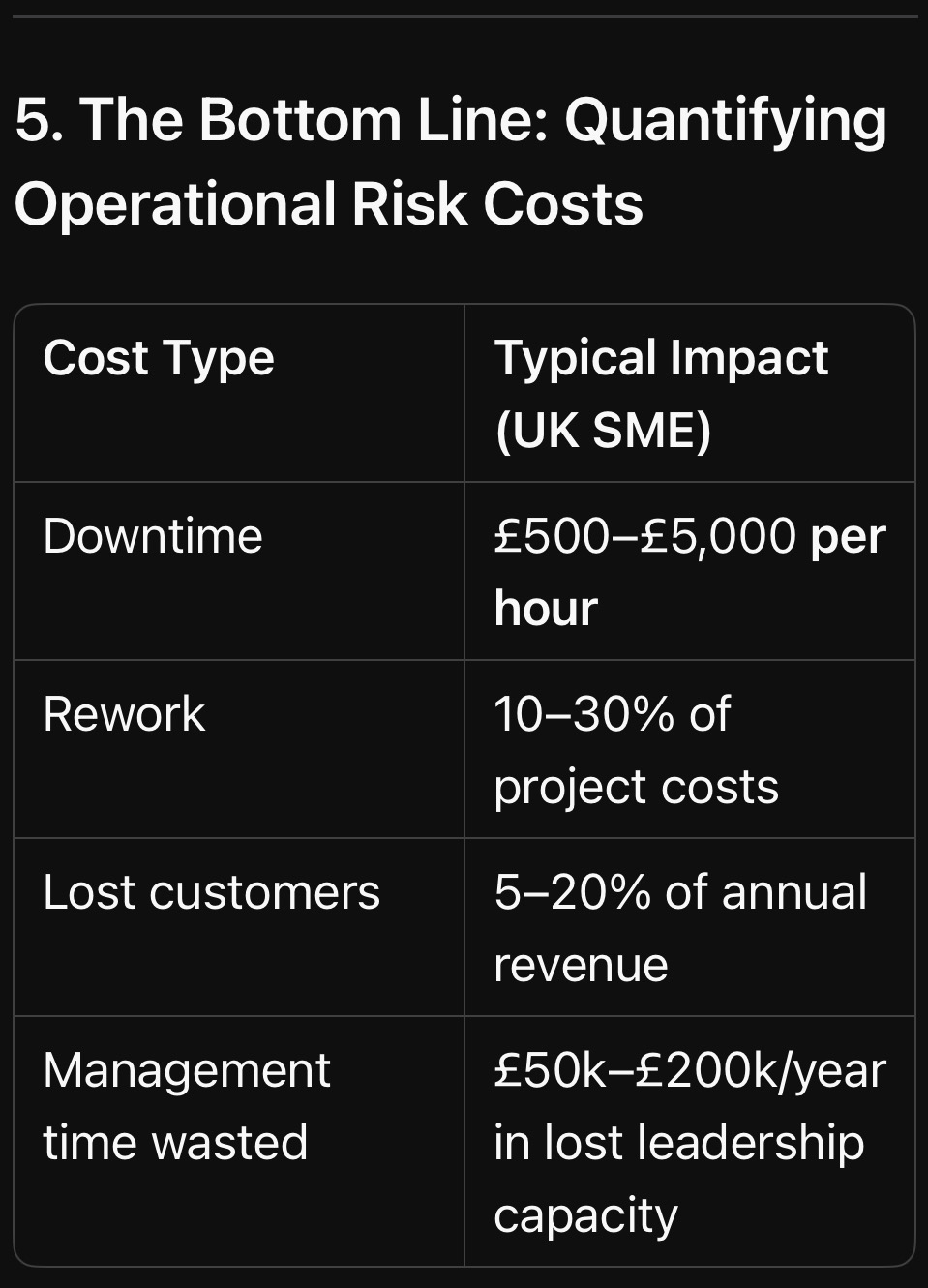

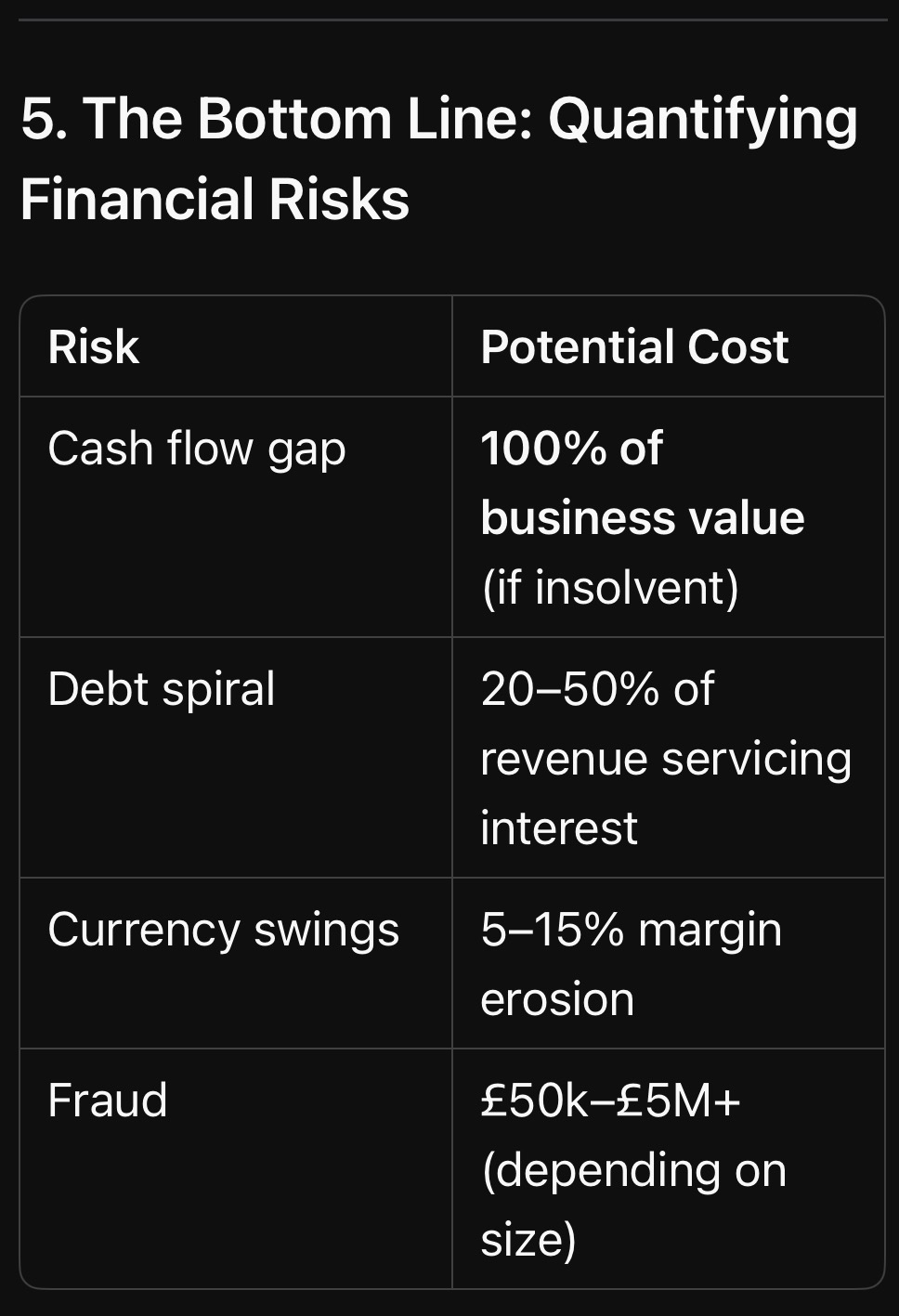

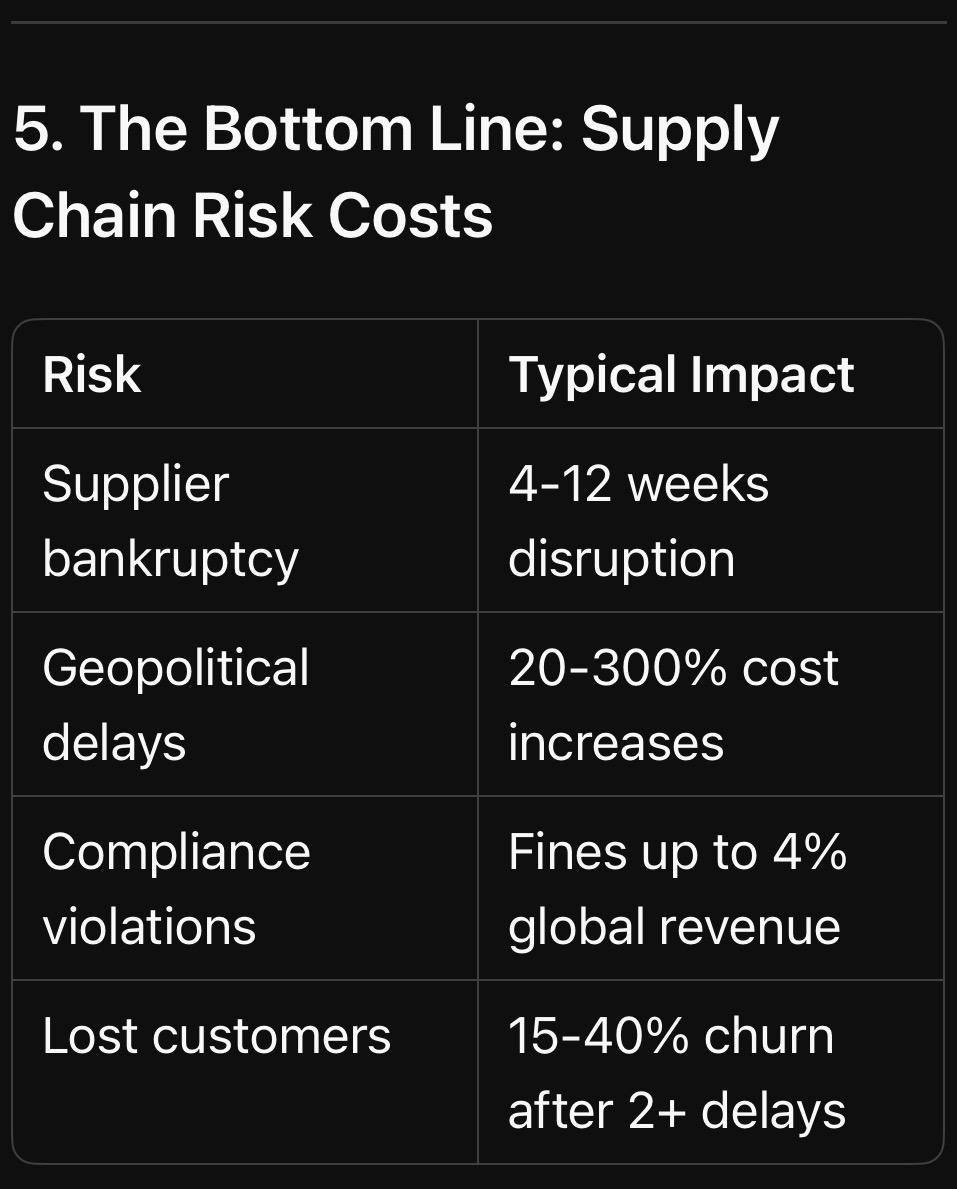

5. The Bottom Line: Quantifying Operational Risk Costs

Key Insight: Operational risks don’t just cost money—they steal time, talent, and future opportunities.

—

More From BusinessRiskTV Business Experts Hub : How to Fix It

We explore how to turn operational risk management into a profit centre, including:

The 5-minute daily habit that prevents 80% of failures

How to engage frontline teams in risk reduction (with real-world examples)

Actionable Task: Map one critical operational process (e.g., order fulfilment). Where could a single failure cost you £10k+?

—

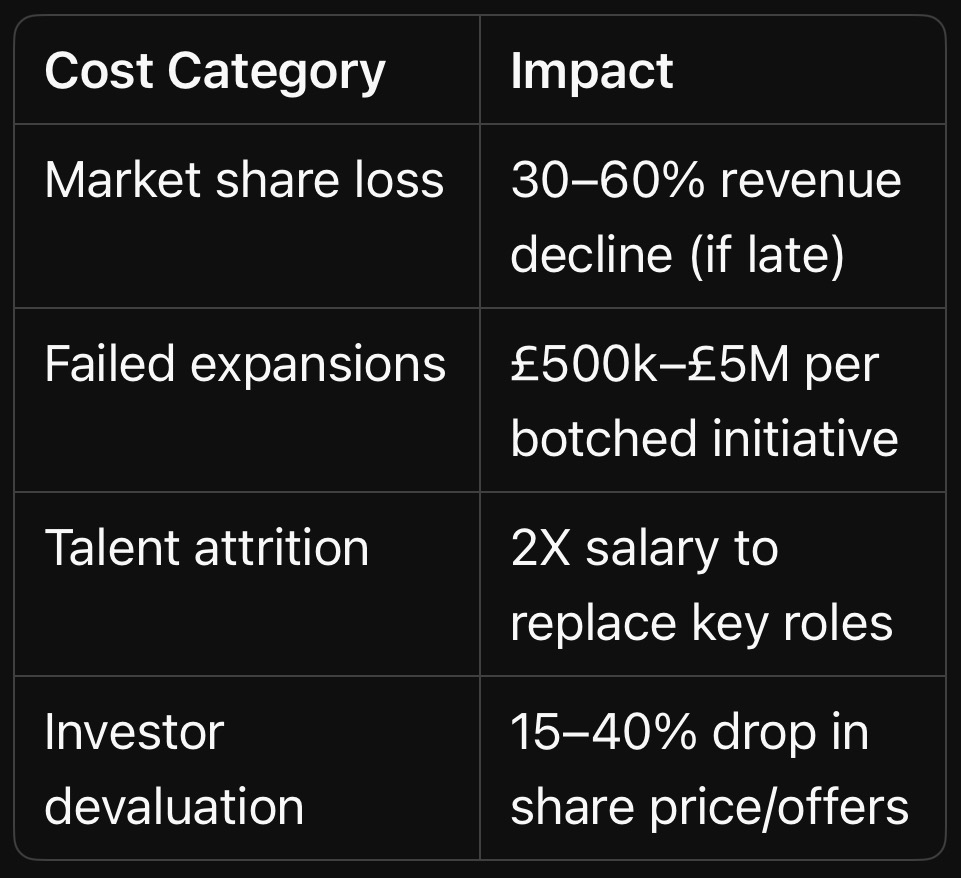

Chapter 3: Strategic Risks – How Blind Spots in Planning Can Bankrupt Even Profitable Businesses

Introduction: The Silent Assassin of Business Growth

Strategic risks don’t announce themselves with alarms — they creep in unnoticed while leadership is distracted by day-to-day operations. By the time the damage is visible, it’s often too late to pivot. This chapter exposes how poor strategic risk management destroys market position, erodes competitive edge, and turns industry leaders into cautionary tales.

—

1. What Are Strategic Risks? (And Why They’re Different)

Key Takeaway: Strategic risks don’t just hurt profits — they erase entire business models.

—

More from BusinessRiskTV Business Experts Hub : How to Anticipate & Outmanoeuvre Strategic Risks

We explore practical frameworks to:

Spot industry shifts early (using weak signals)

Stress-test your strategy against disruption

Turn risks into opportunities (like Amazon’s pivot from books to cloud)

Actionable Task: List one strategic assumption your business relies on (e.g., “Customers will always prefer X”). How would you survive if it’s wrong?

—

Chapter 4: Financial Risks – How Poor Cash Flow & Debt Management Can Sink Your Business Overnight

Introduction: The Silent Killer of Healthy Businesses

Profit doesn’t equal survival. Thousands of UK businesses post record revenues—right before going bust. Why? Because financial risk management isn’t about counting pennies — it’s about anticipating traps that strangle cash flow, trigger defaults, and collapse supply chains.

This chapter exposes the lethal financial risks hiding in plain sight — and why even profitable companies run out of money.

—

1. The Obvious (But Ignored) Financial Risks

A. Cash Flow Crises – The #1 Business Killer

Reality: 82% of UK business failures cite cash flow problems as the primary cause (UK Insolvency Service).

Example: A £5M-turnover construction firm collapses because:

– Client pays invoices 90 days late

– Supplier demands upfront payments due to past delays

– Bank rejects emergency loan Result: Liquidation despite £1.2M in “paper profits.”

B. Debt Avalanches – When Borrowing Backfires

Case Study: A fast-growing e-commerce firm takes on high-interest debt to fund inventory. Sales dip, interest compounds, and suddenly 60% of revenue services debt.

– Stat: 40% of UK SMEs struggle with unmanageable debt (Bank of England).

C. Currency & Commodity Swings

Example: A UK bakery’s flour costs jump 30% after a wheat shortage. Contracts lock in prices — margins vanish overnight.

—

2. The Hidden Financial Risks That Compound Quietly

A. Customer Concentration Risk

Scenario: A B2B software firm gets 70% of revenue from one client. When that client leaves, payroll can’t be met.

Rule of Thumb: No single client should exceed 15–20% of revenue.

B. Supplier Dependency & Price Shocks

Case Study: A car manufacturer relies on one battery supplier. When shortages hit, production stalls for 3 months → £9M loss.

C. Fraud & Financial Mismanagement

Stat: UK businesses lose £137B yearly to fraud, waste, and accounting errors (PwC).

Example: A finance director “cooks the books” — investors pull out when the truth surfaces.

—

3. The Strategic Fallout: When Financial Risks Spiral

A. Credit Downgrades & Banking Nightmares

Example: A once-stable firm misses a loan covenant — interest rates spike 5%, lines of credit freeze.

B. Investor Panic & Equity Crashes

Case Study: A tech startup’s burn rate exceeds projections — VCs demand emergency restructuring, slashing valuation by 50%.

C. Employee Exodus (When Paychecks Bounce)

Stat: 78% of employees leave within 6 months of payroll issues (CIPD).

—

4. The Ultimate Cost: Bankruptcy Dominoes

A. The “Profitable But Insolvent” Paradox

How It Happens:

1. Big contracts signed → revenue looks strong

2. Clients pay late → cash dries up

3. Suppliers demand payment → no money for salaries/tax

4. HMRC forces liquidation despite “growth.”

B. The Carillion Effect (Again)

£7B collapse triggered by:

– Aggressive accounting

– Reliance on unsustainable contracts

– No cash buffer for delays

Key Insight: Financial risks don’t just reduce profits — they erase businesses in weeks.

—

More from BusinessRiskTV Business Experts Hub : How to Fix It

We explore real-world financial risk strategies, including:

The 13-week cash flow rule (used by turnaround experts)

How to renegotiate debt before it’s too late

Building a “war chest” for crises

Actionable Task: Run a “stress test” on your cash flow: What if 2 clients pay 60 days late?

—

Chapter 5: Cyber Risks – The Invisible Threat That Could Bankrupt Your Business by Breakfast

Introduction: The Digital Time Bomb Ticking in Your Business

Imagine arriving at work to find:

Your customer database on the dark web

Fraudsters draining £250,000 from your account

Ransomware locking every file until you pay Bitcoin

This isn’t a movie plot — it’s Monday morning for thousands of UK businesses. Cyber risks don’t just steal data; they extort cash, destroy reputations, and trigger regulatory hell. And here’s the worst part: Most victims never see it coming until the damage is done.

—

1. The Direct Costs: What Happens When Cybercrime Hits

A. Ransomware: The Digital Kidnapping Epidemic

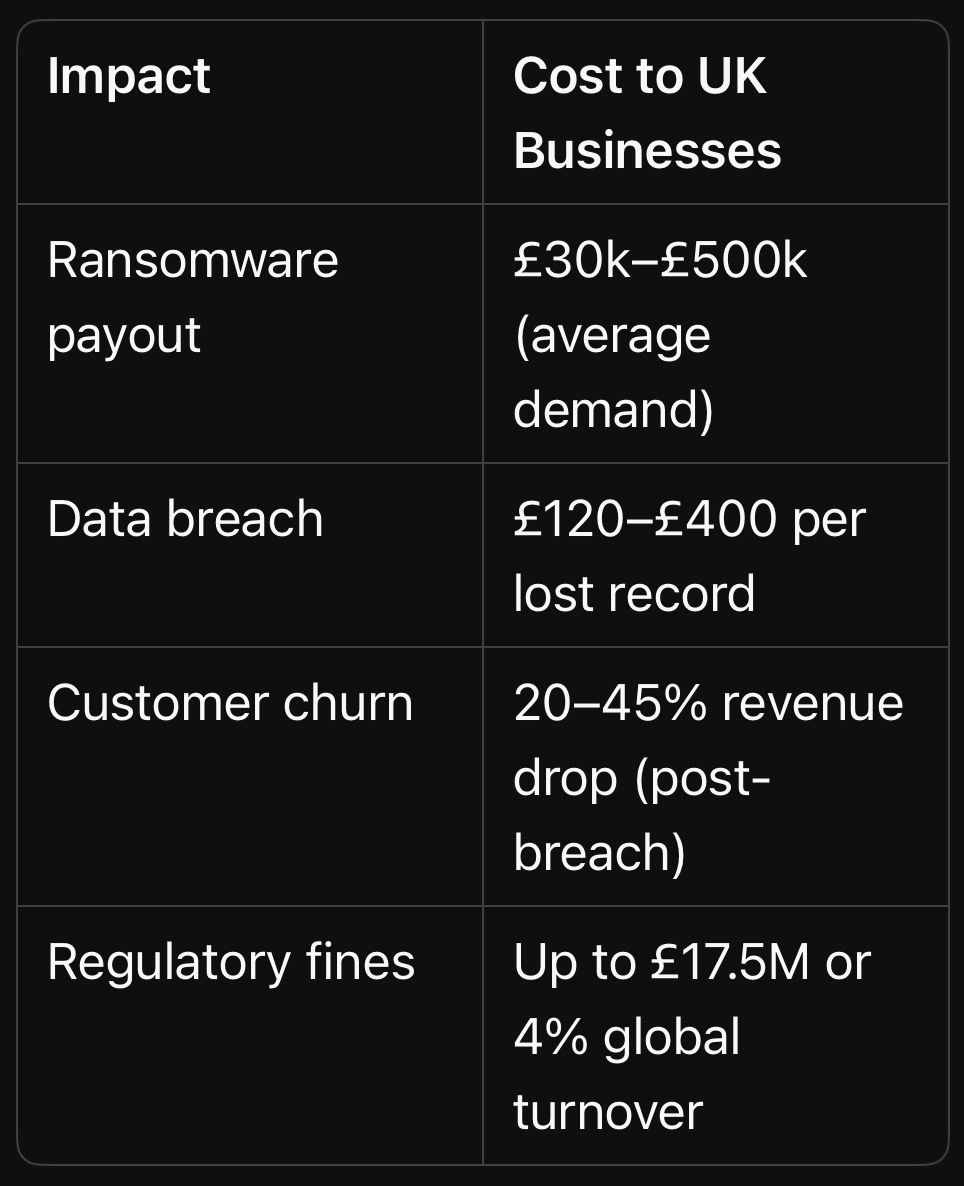

2023 Reality: A UK construction firm’s blueprints, invoices, and payroll systems encrypted. Hackers demand £120,000 to unlock files.

Stat: 73% of UK businesses hit by ransomware in 2023 (NCSC).

Brutal Truth: Paying doesn’t guarantee recovery — 32% never get full data back (Sophos).

B. Data Breaches: When Your Customers Become Victims

Case Study: A mid-sized retailer’s poorly secured e-commerce platform leaks 380,000 credit cards.

£500,000 GDPR fine

£1.2M in fraud reimbursements

22% customer churn

Stat: Average UK data breach cost: £3.4 million (IBM).

C. Business Email Compromise (BEC): The Silent Heist

How It Works: A hacker impersonates your CEO, emails finance: “Urgent: Transfer £80k to new supplier.”

UK Losses: £1.3 billion stolen via BEC in 2023 (UK Finance).

—

2. The Hidden Costs That Cripple You Later

A. Reputation Freefall & Customer Exodus

After a breach:

– 58% of customers avoid breached brands (Verizon)

– Recovery Cost: 3–5X more on marketing to rebuild trust

B. Operational Paralysis

Example: A law firm’s servers go down for 72 hours post-attack. £350k in billable hours lost + client lawsuits.

C. Insurance Nightmares

Post-Claim Realities:

– Premiums triple

– Mandatory audits drain management time

– Some policies simply won’t renew

—

3. The Strategic Fallout: Long-Term Business Damage

A. Lost Contracts & Blacklisting

Government/Corporate Tenders Now Demand:

– Cyber Essentials Certification (missing? Disqualified automatically)

– Proof of incident response plans

B. Investor Flight

Startup Killer: A fintech’s pre-IPO breach scares off VCs, slashing valuation by 60%.

C. Director Liability (Yes, You Can Go to Jail)

UK Law: Under GDPR & NIS Directive, negligent executives face fines up to £17.5M or 4% of global revenue — plus disqualification.

—

4. Why Cyber Risks Are Worse Than You Think

A. It’s Not Just “Big Targets”

61% of UK attacks hit SMEs (Verizon) — hackers bet they’re unprepared.

B. Remote Work = 300% More Attack Surfaces

Example: An employee’s compromised home laptop gives hackers access to your entire CRM.

C. AI-Powered Attacks Are Here

New Threat: Deepfake audio of your CFO “calling” finance to wire funds.

Key Insight: Cyber risks aren’t an “IT problem” — they’re an existential business threat.

—

More from BusinessRiskTV Business Experts Hub : How to Fight Back

We will explore real-world cyber defenses, including:

The 5-step SME ransomware shield (costs <£5k/year)

– How to trick hackers into avoiding you (attackers prefer easy targets)

– Turning employees into human firewalls

Actionable Task: Run this free test now: [Have I Been Pwned](https://haveibeenpwned.com/) to check if your work emails are already in hacker databases.

—

Chapter 6: Human Risks – When Your Greatest Asset Becomes Your Biggest Liability

Introduction: The Enemy Inside Your Walls

Your employees can either be your strongest defence — or your weakest link. Negligence, disengagement, and malicious actions cost UK businesses £30 billion annually (ACAS). This chapter exposes how poor people risk management leads to:

– Catastrophic errors

– Culture collapse

– Regulatory disasters

– Fraud epidemics

And why traditional HR policies fail to prevent 89% of these risks (PwC).

—

1. The Obvious (But Ignored) Human Risks

A. The High Cost of Disengagement

Example: A retail chain’s apathetic staff miss 40% of shoplifting incidents —costing £220,000/year in stolen stock.

Stat: Disengaged employees are 450% more likely to cause operational errors (Gallup).

B. Turnover Tsunamis

Case Study: A tech firm’s toxic culture drives out 7 senior engineers in 6 months — delaying a £2M product launch by 11 months.

Replacement Cost: Up to 2X annual salary per lost employee (Oxford Economics).

C. Training Gaps That Become Legal Nightmares

Reality Check: A warehouse worker badly operates a forklift, causing £80k in damages + HSE fines—because “training was just a 10-minute video.”

—

2. The Hidden (But More Dangerous) Human Risks

A. Insider Threats: When Employees Attack

Shocking Stat: 58% of data breaches involve insiders (Verizon).

Methods:

– The Malicious: IT admin sells customer data (£50k on dark web)

– The Careless: Accountant emails payroll files to personal Gmail

B. Culture Risks: How Toxicity Spreads

Example: A sales team’s “win at all costs” mentality leads to fraudulent client promises — £600k in lawsuits + FCA investigation.

C. Leadership Blind Spots

CEO Overconfidence: Ignoring team warnings about a flawed expansion → £3M write-off.

Stat: 82% of business failures trace back to poor leadership decisions (KPMG).

—

3. The Strategic Fallout: When People Risks Sink Companies

A. The Volkswagen Emissions Scandal

Root Cause: A culture where “nobody dared question” fraudulent engineering.

– Cost: €32 billion in fines/losses + permanent brand damage.

B. The Barclays CEO Scandal

How It Happened: Leadership’s obsession with “star hires” led to unchecked bullying — triggering £1M fines + investor revolt.

C. The Everyday SME Killer

Scenario: Your “trusted” bookkeeper embezzles £150k over 3 years — exposed only during a tax audit.

—

4. Why Traditional Approaches Fail

Annual compliance training?86% of employees forget it within 30 days (MIT).

“Hotline whistleblowing”?62% of staff fear retaliation (EY).

Top-down policies? Frontline teams see them as “head office nonsense.”

Key Insight: Your employees create or destroy value daily — often without realising it.

—

More from BusinessRiskTV Business Experts Hub : How to Transform Human Risk into Advantage

We explore battle-tested solutions, including:

The “Psychological Safety” hack

How to spot insider threats before they strike

Turning compliance into competitive edge

Actionable Task: Run a 5-minute “risk culture pulse check” with your team this week: “What’s one process you think could fail catastrophically?”

—

Chapter 7: Supply Chain Risks – The Fragile Web That Could Strangle Your Business Overnight

Introduction: Your Business Is Only as Strong as Its Weakest Supplier

A single delayed shipment. One insolvent vendor. A geopolitical shockwave. Suddenly, your production line stops, customers revolt, and cash flow evaporates.

Key Insight: Supply chains have become the ultimate leverage point — for your competitors or your downfall.

—

More from BusinessRiskTV Business Experts Hub : How to Build an Unbreakable Supply Chain

We explore wartime-tested strategies, including:

The “3D Supplier Mapping” trick (used by Special Forces logisticians)

How to turn suppliers into partners (not adversaries)

When to nearshore/onshore without bankrupting yourself

Actionable Task: Identify one “critical” supplier you couldn’t operate without. How would you survive if they vanished tomorrow?

—

Chapter 8: Reputational Risks – When Trust Collapses Faster Than Your Share Price

Introduction: The 24-Hour Business Execution

A single tweet. One viral video. A disgruntled employee’s LinkedIn post. In today’s digital wildfire, your hard-earned reputation can evaporate before your crisis team finishes their first coffee.

The brutal reality:

87% of consumers will abandon a brand after a reputation crisis (YouGov)

It takes 4-7 years to build trust but just 4 bad days to destroy it (Edelman Trust Barometer)

65% of a company’s market value is tied to intangible assets like reputation (Ocean Tomo)

This isn’t about PR spin – it’s about preventing the preventable and surviving the unpredictable.

—

1. The Obvious Reputation Killers

A. Social Media Firestorms

Case Study: A restaurant manager’s racist comment caught on video → 300,000 angry tweets in 48 hours → permanent 40% revenue drop

Stat: Viral crises spread 20x faster than management can respond (MIT Sloan)

B. Executive Scandals

The P&G CEO Effect: A $375 billion company lost $40B in market cap in days after CEO’s inappropriate relationship surfaced

“No comment” = “We’re guilty” in public perception

Corporate-speak increases distrust by 41% (Edelman)

Legal-first responses often worsen the crisis

—

5. The Survival Playbook (Preview)

More from BusinessRiskTV Business Experts Hub we will explore modern reputation armour, including:

The “Dark Web Early Warning” system (catch crises before they explode)

Turning employees into reputation ambassadors

When to apologise vs. when to fight back

Actionable Task: Google “[Your Brand] + scandal” right now. What autocomplete suggestions appear?

—

Chapter 9: Climate Risks – The Existential Threat That’s Already Costing Your Business

Introduction: Your Business Is on the Frontlines of the Climate Crisis

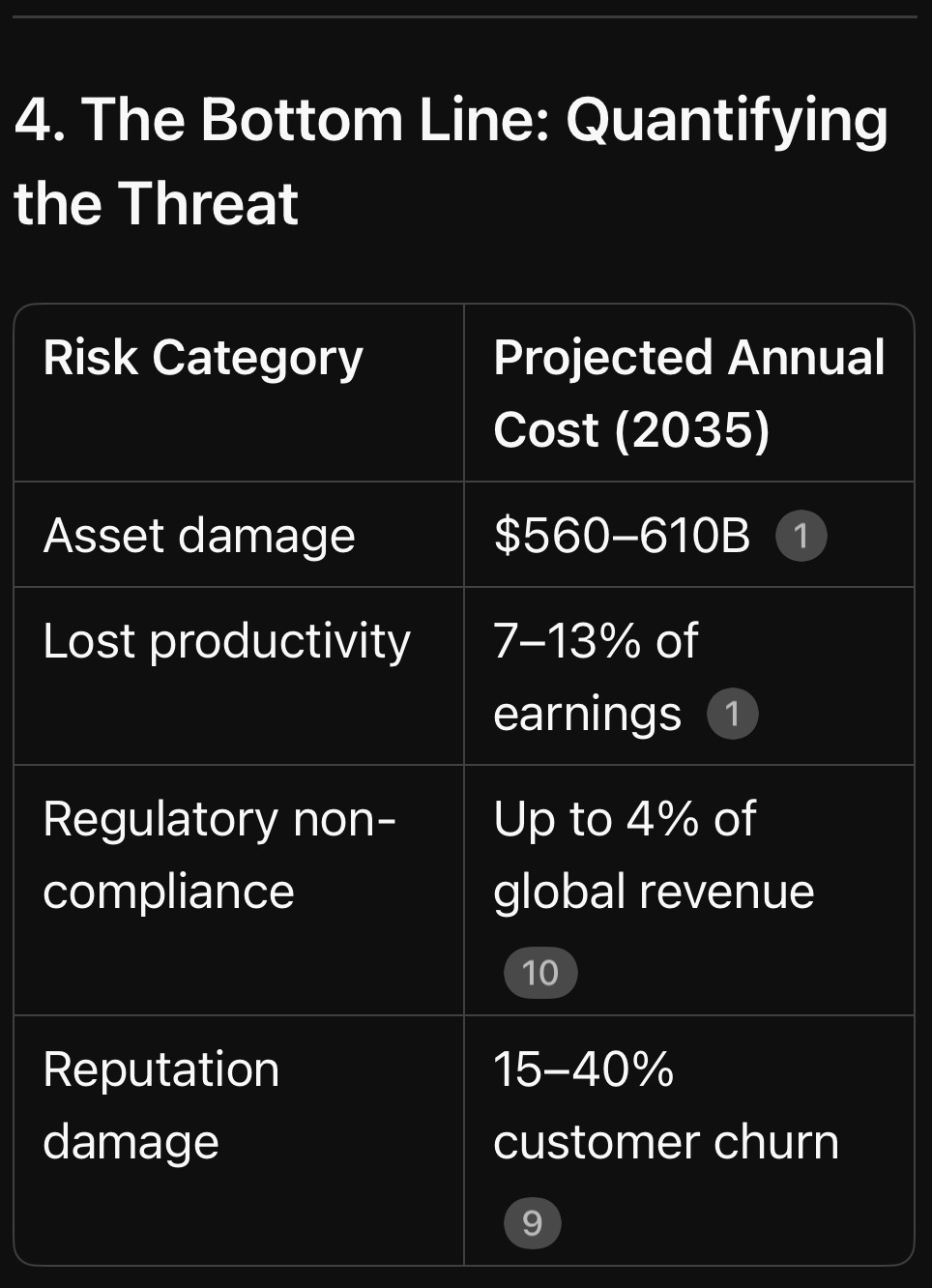

Climate change isn’t a distant threat — it’s eroding profits, disrupting supply chains, and rewriting industry rules rightnow. In 2024 alone, climate disasters caused $2 trillion in global losses, with businesses absorbing the brunt through:

Operational shutdowns (e.g., factories flooded, data centres overheated

Soaring insurance premiums (up 300% in high-risk zones)

Regulatory penalties (e.g., non-compliance with carbon disclosure rules)

This chapter exposes the hidden costs of climate risks — and why most companies are dangerously unprepared.

—

1. The Two Faces of Climate Risk

A. Physical Risks: When Nature Attacks

1. Acute Disasters:

– Example: Hurricane Helene (2024) caused $225B in damages, disrupting microchip supplies by destroying a key quartz supplier .

– Stat: Severe weather events now cost businesses $560–610B yearly in asset losses .

2. Chronic Pressures:

– Heatwaves reduce worker productivity by 15–20% in sectors like construction and agriculture .

– Droughts forced a UK beverage company to halt production for 6 weeks due to water shortages .

B. Transition Risks: The Legal and Market Backlash

1. Policy Shocks:

– Carbon taxes could erase 20% of profits for high-emission firms by 2030 .

– Example: EU’s Carbon Border Tax added 10–20% costs for non-compliant imports .

2. Reputation Fallout:

– 75% of consumers boycott brands with poor sustainability records .

– Investor Flight: ESG-backlash aside, 90% of Fortune 500 firms now face shareholder climate lawsuits .

—

2. The Hidden Costs You’re Not Tracking

A. Supply Chain Domino Effects

Case Study: Floods in Thailand (2023) disrupted 40% of global hard drive production → tech firms lost $20B+

Stat: 73% of companies admit their supply chains are “highly vulnerable” to climate shocks .

B. Workforce Crises

Heat Stress: UK warehouses saw 30% more sick days during 2024’s record summer .

Talent Drain: 67% of Gen Z employees reject jobs at firms with weak climate policies .

C. Stranded Assets

Example: Oil companies wrote off $300B in reserves as “unburnable” due to net-zero policies.

Projection: 20% of commercial real estate will be uninsurable by 2030 .

Key Insight: Climate risks are profit killers — not just “ESG checkboxes.”

—

More from BusinessRiskTV Business Experts Hub : How to Fight Back

We will explore actionable climate resilience strategies, including:

The “3D Supply Chain Mapping” tactic (used by Special Forces logisticians)

How to turn carbon cuts into tax savings

AI-powered climate forecasting tools

Actionable Task: Run a 5-minute vulnerability scan: Which single climate threat (e.g., flood, heatwave) couldshut down your operations for 48 hours?

—

*Sources: World Economic Forum , Allianz , Beazley , Optera , EPA *

Chapter 10: 12 Actionable Solutions to Transform Risk into Competitive Advantage

Introduction: Risk Management Isn’t About Survival—It’s About Dominance

The most profitable companies don’t just avoid risks — they weaponise them. Toyota’s supply chain resilience made it the #1 automaker during the chip shortage. Amazon turned cybersecurity into a $35B AWS profit centre.

This chapter delivers 12 battle-tested solutions to stop losing money and start outpacing competitors.

—

Solution 1: The “Risk Ownership” Culture Hack

Problem: Employees see risk as “management’s problem.”

Fix:

– Tie 10-15% of bonuses to risk KPIs (e.g., near-miss reports, compliance audits)

– Example: A logistics firm reduced warehouse injuries by 62% after adding safety metrics to performance reviews

Action Step: This week, have each department identify one preventable risk they’ll now “own.”

—

Solution 2: The 5-Minute Daily Risk Radar

Problem: Monthly reports miss emerging threats.

Fix:

– Daily 5-minute standups on:

Top 3 operational vulnerabilities (e.g., server capacity, inventory levels)

Weak signals (e.g., supplier payment delays, social media complaints)

Case Study: A manufacturer caught a critical component shortage 3 weeks early by tracking supplier lead times daily

**Template:**

“`

[ ] Key risk #1 status

[ ] New threat detected

[ ] Mitigation action

“`

—

Solution 3: Cyber “Human Firewall” Training That Works

Problem: Boring compliance training fails.

Fix:

Monthly simulated phishing with “hacked” employees retaking interactive VR training

Result: One law firm reduced click-through rates from 28% to 3% in 6 months

Free Tool: Use CanIPhish for automated simulations

—

Solution 4: The 13-Week Cash Flow War Chest

Problem: Companies die from cash flow gaps, not lack of profit.

Fix:

1. Map all cash inflows/outflows week-by-week

2. Identify 3 survival levers (e.g., delayed payables, early collections)

3. Stress test with:

– 30% sales drop

– 60-day client payment delays

Example: A restaurant chain survived COVID by pre-negotiating 90-day rent deferrals before lockdowns

—

Solution 5: Supplier “X-Ray” Audits

Problem: 4th-tier suppliers can bankrupt you.

Fix:

– Demand blockchain-tracked materials for critical inputs

– Red Team Test: Randomly delay payments to check supplier liquidity

– Stat: Firms with mapped supply chains recover 9x faster from disruptions

—

Solution 6: AI-Powered Risk Forecasting

Toolkit:

Climate: Cervest (predict asset flooding)

Cyber: Darktrace (autonomous threat detection)

Financial: Simudyne (stress test scenarios)

ROI Example: A insurer cut claims by 22% using flood prediction AI

—

Solution 7: The “Pre-Mortem” Strategy Session

Problem: Executives ignore failure scenarios.

Fix: Before decisions:

1. Imagine the project has failed catastrophically

2. Brainstorm exactly why

3. Build safeguards

Case Study: Boeing’s 737 Max crashes could’ve been prevented by this method

—

Solution 8: Embedded Risk Officers

Innovation: Place risk champions in:

– R&D teams (kill flawed prototypes early)

– Sales (flag unrealistic client promises)

– Result: A pharma firm avoided $200M in FDA fines by catching compliance gaps during drug development

—

Solution 9: Dynamic Risk Scoring

Tool: Custom risk dashboards weighting:

– Probability (1–10)

– Impact (£)

– Velocity (how fast threat is growing)

– Example: A bank auto-prioritises risks scoring >£500k impact

—

Solution 10: The “Unthinkable” Drill

Annual Exercise: Simulate:

– CEO arrested

– HQ destroyed

– Key Result: BrewDog survived a ransomware attack because they’d practiced IT failovers quarterly

—

Solution 11: Turn Risk Into Revenue

Examples:

– Tesla sells carbon credits ($1.8B in 2023)

– Maersk’s green shipping premiums command 20% price hikes

Dubai Freelancer Visa for the purpose of operating an online business

Escape the Ordinary, Embrace Dubai: Your Blueprint for UK Residents to Launch an Online Empire and Secure Residency Through the Freelancer Visa!

Feeling the squeeze of the UK economy? Tired of the same old routine? What if I told you there’s a vibrant, opportunity-rich landscape beckoning, where you can not only build a thriving online business but also secure residency? That’s the allure of Dubai’s Freelancer Visa, a golden ticket for ambitious UK residents looking to redefine their professional and personal lives in 2025! Imagine waking up to sunshine, operating your global online venture from a dynamic hub, and benefiting from a pro-business environment. Sounds enticing, right?

For savvy UK entrepreneurs and freelancers, this isn’t just a pipe dream; it’s an increasingly viable pathway. Dubai has strategically positioned itself as a global nexus for innovation and commerce, actively attracting international talent and investment.One of the key instruments in this strategy is its dedicated Freelancer Visa programme, specifically designed to empower independent professionals and online business owners. This isn’t about escaping your responsibilities; it’s about strategically positioning yourself for greater success and a higher quality of life. Think about it: a burgeoning digital economy, attractive tax policies within designated free zones, and a cosmopolitan lifestyle – all within reach.

This comprehensive guide will navigate you through the intricacies of leveraging Dubai’s Freelancer Visa to establish and scale your online business while securing residency. We’ll delve into the “why,” the “what,” the “where,” the “when,” and the “how” of this exciting opportunity. Get ready to unlock a world of possibilities and take control of your future!

Why Dubai’s Freelancer Visa is a Smart Move for UK Residents in 2025

Several compelling factors make Dubai’s Freelancer Visa an increasingly attractive option for UK residents looking to establish or grow their online businesses and gain residency:

1. Thriving Digital Economy and Business-Friendly Environment:Dubai has made significant strides in fostering a robust digital infrastructure and a pro-business ecosystem.The government actively supports innovation, technology adoption, and entrepreneurship. This creates a fertile ground for online businesses to flourish, offering access to a dynamic market and a global network of professionals. The sheer energy and ambition palpable in Dubai can be incredibly motivating for entrepreneurs seeking growth.

2. Strategic Location and Global Connectivity:Situated at the crossroads of East and West, Dubai offers unparalleled access to global markets.Its world-class transportation infrastructure, including a major international airport and efficient logistics networks, facilitates seamless international business operations. For online businesses with a global reach, this strategic positioning can be a significant advantage, allowing for easier interaction with clients and partners across different time zones.

3. Attractive Tax Policies within Free Zones: One of the most significant draws for entrepreneurs is the favourable tax environment within Dubai’s designated free zones.Many of these zones offer 0% corporate and personal income tax, which can substantially boost profitability for your online business. This financial advantage allows for greater reinvestment and faster growth compared to higher-tax jurisdictions. Imagine the impact of zero income tax on your bottom line!

4. High Quality of Life and Cosmopolitan Environment:Dubai offers a high standard of living with modern infrastructure, world-class amenities, and a diverse and vibrant social scene. The city boasts excellent healthcare, education, and recreational facilities. For UK residents seeking a change of pace and a more cosmopolitan environment, Dubai provides a compelling lifestyle proposition. Plus, the year-round sunshine is a definite bonus!

5. Opportunity for Residency and Long-Term Stability:Unlike short-term business visas, the Freelancer Visa in Dubai offers a pathway to long-term residency, providing stability and a sense of belonging. This can be particularly appealing for individuals looking to build a long-term future for themselves and their families in a dynamic and growing international hub. Securing residency opens up numerous personal and professional opportunities.

6. Access to a Diverse Talent Pool: Dubai attracts a highly skilled and diverse international talent pool. This can be a significant advantage for online businesses looking to scale and build a strong team. The multicultural environment fosters innovation and provides access to a wide range of expertise.

7. Government Support for SMEs and Startups: The Dubai government actively supports small and medium-sized enterprises (SMEs) and startups through various initiatives, funding programmes, and incubation centres.This supportive ecosystem can provide valuable resources and networking opportunities for newly established online businesses.

Eligible Online Businesses for the Dubai Freelancer Visa

The Dubai Freelancer Visa is designed to attract a wide range of skilled professionals operating online. While specific regulations may evolve, here are some common categories of online businesses and freelance professions generally eligible for this visa:

Illustration and Animation (Online Commissions/Sales): Creating and selling digital artwork and animations.

Important Note: This list is not exhaustive, and the specific eligibility criteria can be subject to change based on the free zone authority and the prevailing regulations. It is crucial to consult with the relevant free zone authority or a professional consultancy to confirm the eligibility of your specific online business activity.

Navigating Dubai’s Free Business Zones: Your Launchpad for Success

Dubai boasts several designated free zones, each with its own specific focus and regulations. These zones offer attractive incentives, including tax exemptions, full foreign ownership, and streamlined business setup processes. Here are some of the prominent free zones that are particularly relevant for online businesses and freelancers:

1. Dubai Multi Commodities Centre (DMCC):Located in the Jumeirah Lakes Towers (JLT) area, DMCC is one of Dubai’s largest and most diverse free zones. It’s home to a wide range of businesses, including those in technology, trading, and professional services. DMCC offers a dedicated “Freelancer Package” designed to provide cost-effective business setup and licensing options for individual professionals. Their online portal and efficient processes make it a popular choice.

2. Dubai Internet City (DIC):As the name suggests, DIC is a hub for technology and internet-based companies.It hosts a large ecosystem of IT, software, e-commerce, and digital media businesses. While traditionally focused on larger companies, DIC also offers options for freelancers and smaller online ventures within its broader framework. Being part of this vibrant tech community can offer significant networking and collaboration opportunities.

3. Dubai Media City (DMC):DMC is the region’s leading hub for media and creative industries.It’s home to numerous media companies, advertising agencies, production houses, and freelance professionals in content creation, journalism, and digital media. If your online business aligns with these sectors, DMC can provide a supportive and industry-focused environment.

4. Dubai Knowledge Park (DKP):DKP is dedicated to human resource management, training, and professional development. While it might seem less directly relevant to all online businesses, it can be a good option for online educators, trainers, and e-learning content creators.

5. Meydan Free Zone: Located near the Meydan Racecourse, this free zone offers a cost-effective and relatively straightforward business setup process, including options suitable for freelancers and online businesses. It’s known for its competitive pricing and efficient services.

6. IFZA (International Free Zone Authority): IFZA is another popular choice offering competitive setup costs and a wide range of business activities suitable for online operations.They have streamlined processes and cater to international entrepreneurs.

Key Considerations When Choosing a Free Zone:

Business Activity Alignment: Ensure the free zone allows your specific online business activity under its licensing regulations.

Cost of Setup and Renewal: Compare the fees associated with registration, licensing, and annual renewal across different free zones.

Facilities and Support Services: Consider the availability of co-working spaces, business centres, and other support services you might need.

Networking Opportunities:Some free zones have stronger industry-specific communities, which can be beneficial for networking and collaboration.

Visa and Immigration Procedures: Understand the specific visa and immigration processes associated with each free zone.

It is highly recommended to research the specific offerings and regulations of each free zone thoroughly and potentially consult with business setup specialists to determine the best fit for your individual needs and online business model.

Timing Your Application: When to Make the Move

Deciding when to apply for the Dubai Freelancer Visa is a crucial aspect of your planning. Several factors should influence your timeline:

1. Business Readiness: Ideally, you should have a clear business plan, a defined online service or product offering, and ideally, some existing online presence or client base. While you can start the process with a strong concept, being prepared will streamline your application and ensure you can hit the ground running in Dubai.

2. Financial Preparedness:Setting up a business and relocating involves costs. Ensure you have sufficient funds to cover visa application fees, business registration costs, initial living expenses in Dubai, and working capital for your online venture. Research the specific costs associated with your chosen free zone and desired lifestyle.

3. Visa Processing Time: The processing time for the Freelancer Visa can vary depending on the free zone and the volume of applications. It’s prudent to factor in potential delays and allow ample time before your intended relocation date. Generally, the process can take anywhere from a few weeks to a couple of months.

4. Personal Circumstances: Consider your personal commitments, such as existing employment contracts, family arrangements, and any other obligations that might impact your ability to relocate. Plan your move in a way that minimizes disruption to your life.

Can You Apply from the UK or on a Visitor Visa in Dubai?

Applying from the UK: Yes, it is generally possible to initiate the application process for a Dubai Freelancer Visa while you are still in the UK. Most free zones have online portals and allow you to complete the initial documentation and application remotely. However, you will likely need to travel to Dubai at some point to finalise the process, undergo medical examinations, and receive your residency visa.

Applying on a Visitor Visa in Dubai: Yes, it is also possible to apply for a Freelancer Visa while you are in Dubai on a visitor visa. This is a common route for individuals who want to explore the environment and meet with free zone authorities before committing. However, it’s crucial to ensure that your visitor visa allows for a change of status and that you comply with all immigration regulations. You will typically need to undergo the application process through the chosen free zone authority while in Dubai. Be aware of the validity period of your visitor visa and ensure you have enough time to complete the Freelancer Visa process. Overstaying your visitor visa can lead to penalties.

Recommendation: Regardless of whether you apply from the UK or on a visitor visa, it is highly recommended to contact the specific free zone authority you are interested in or consult with a business setup agency to get the most up-to-date information on their application procedures and requirements for non-resident applicants.

Who is Eligible to Apply for the Freelancer Visa?

While specific eligibility criteria can vary slightly between different free zones, the general requirements for a Dubai Freelancer Visa typically include:

Professional Expertise: You must possess demonstrable skills and experience in a profession or business activity that is eligible under the free zone’s regulations (as discussed earlier). You may need to provide a portfolio, client testimonials, or other evidence of your expertise.

Educational Qualifications: Some free zones may require a minimum level of educational qualification relevant to your field. Be prepared to provide copies of your degrees or certifications.

Financial Capacity: You will need to demonstrate that you have sufficient financial resources to support yourself during the initial period of your residency and to fund your business operations. This might involve providing bank statements or a business plan with financial projections.

Clean Criminal Record: You will typically need to provide a police clearance certificate from your home country (the UK in this case) to demonstrate that you have a clean criminal record.

Medical Fitness: You will be required to undergo a medical examination in Dubai to ensure you are medically fit to reside and work in the UAE.

Passport Validity: Your passport must have a sufficient validity period (usually at least six months) at the time of application.

Business License Application: You will need to apply for a freelancer or sole establishment business license within your chosen free zone, outlining your specific business activities.

Visa Application Forms and Supporting Documents: You will need to complete the required application forms and provide various supporting documents, such as passport copies, photographs, and other documents as requested by the free zone authority.

Important Note: The specific requirements and documentation can vary. It is essential to consult the official website of your chosen free zone or contact them directly for the most accurate and up-to-date eligibility criteria. They can provide a detailed list of required documents and guide you through the process.

Your Dubai Opportunity Awaits in 2025!

The Dubai Freelancer Visa presents a compelling opportunity for UK residents to not only establish and grow their online businesses in a dynamic and supportive environment but also to secure long-term residency in a thriving global hub. The combination of a business-friendly ecosystem, attractive tax policies within free zones, a high quality of life, and the potential for global connectivity makes Dubai an increasingly attractive destination for ambitious entrepreneurs and freelancers.

While the process involves careful planning, research, and adherence to specific regulations, the rewards can be significant. Imagine operating your online empire from a sun-drenched location, benefiting from a zero-tax environment, and immersing yourself in a vibrant international culture. This isn’t just about a visa; it’s about unlocking a new chapter of opportunity and growth for your business and your life.

So, if you’re a UK resident with a thriving online business or a compelling freelance offering, 2025 could be your year to take the leap. Explore the possibilities, research the free zones, prepare your application, and embrace the exciting journey of building your online empire and securing your future in Dubai! The time to escape the ordinary and embrace extraordinary opportunities is now!

UK business leaders overconfident in their future business prospects?

UK business risk management strategies for high inflation environment

The UK economy is facing a confluence of challenges that demand careful navigation by business leaders. The recent allotment of the second-highest amount on record at the Bank of England’s short-term repo (January 2, 2025), serves as a stark reminder of the potential headwinds. This surge in borrowing by banks from the central bank signals potential liquidity concerns, a possible economic slowdown, and the ever-present risk of inflationary pressures.

Navigating the Storm: A Guide for UK Business Leaders

In this turbulent economic climate, proactive risk management is no longer an option, but a necessity. Businesses must adapt to a dynamic landscape characterised by persistent inflation, the lingering effects of Brexit, the ongoing energy crisis, and the ever-present shadow of geopolitical instability. These interconnected challenges demand a multi-faceted approach to risk mitigation.

Key Actions for Business Leaders:

Embrace Dynamic Pricing: Adapt pricing strategies to reflect market fluctuations and input costs.

Diversify Supply Chains: Reduce reliance on single suppliers and explore alternative sourcing options.

Negotiate with Suppliers: Leverage bargaining power to secure favourable terms.

Explore New Markets: Diversify customer base by expanding into new markets.

Invest in Skills and Training: Address the skills gap to ensure workforce adaptability.

Improve Energy Efficiency: Implement energy-saving measures to reduce costs.

Explore Renewable Energy Options: Consider investing in renewable energy sources.

Hedge Against Price Volatility: Explore options to mitigate the impact of energy price fluctuations.

Build Resilient Supply Chains: Diversify supply chains to minimize reliance on any single region or supplier.

Monitor Geopolitical Developments: Stay informed about global events and their potential impact.

Cultivate a Strong Brand: Invest in building a strong brand reputation to weather economic storms.

Embrace Digital Transformation: Leverage digital technologies to improve efficiency and customer experience.

Invest in Innovation: Allocate resources for research and development to explore new opportunities.

Develop a Data-Driven Culture: Leverage data analytics to gain insights into market trends and operational performance.

Strengthen Cybersecurity Measures: Implement robust cybersecurity measures to protect against cyber threats.

Conduct Regular Security Audits: Regularly assess and address vulnerabilities in IT systems.

Develop a Data Breach Response Plan: Prepare for and mitigate the impact of potential data breaches.

Stay Informed About Regulatory Changes: Ensure compliance with evolving laws and regulations.

Build Strong Relationships with Regulators: Foster open communication with regulators to address concerns.

Attract and Retain Talent: Implement strategies to attract and retain top talent.

Develop Products and Services for an Aging Population: Adapt offerings to cater to the needs of an aging demographic.

Embrace Diversity and Inclusion: Create a diverse and inclusive workplace that values all employees.

Adopt Sustainable Practices: Implement sustainable practices to minimize environmental impact.

Engage with Stakeholders: Engage with stakeholders to address their concerns and build trust.

Embrace Corporate Social Responsibility: Develop a CSR strategy that aligns with business values and contributes to a better society.

Conclusion

The UK economy faces a complex and interconnected set of challenges. However, by proactively identifying and mitigating these risks, businesses can navigate these turbulent waters and emerge stronger. This requires a shift in mindset—a move from reactive to proactive, agile, and resilient approaches. By embracing these principles, businesses can not only survive but thrive, transforming challenges into opportunities and building a more sustainable and prosperous future for the UK economy.

Are UK Business Leaders Mad Political or Missing Key Economic Data?

Recent optimism in the UK business community has raised eyebrows across the Atlantic, where economic headwinds are causing significant concern. The Lloyds Bank Business Barometer jumped by eight points to 50% in May, its highest since November 2015. This stark contrast begs the question: are UK business leaders simply more optimistic, or are they missing crucial economic data that is readily apparent in the US?

Reasons for UK Business Optimism:

Stronger-than-expected May data: The Lloyds Bank Business Barometer suggests a significant uptick in business confidence, with optimism in manufacturing, construction, and services sectors.

Government support: The UK government has implemented various measures to support businesses during the pandemic and the ongoing cost-of-living crisis. These include tax breaks, grants, and energy price caps.

However, concerns remain:

High debt levels: Both the UK and the US have accumulated significant national debt in recent years. This debt burden could limit the government’s ability to respond to future economic shocks.

Stagflation risk: The combination of rising inflation and slowing economic growth (stagflation) is a major concern for both economies. This could lead to further business uncertainty and investment delays.

Rising unemployment: Both the UK and the US are experiencing rising unemployment, which could dampen consumer spending and reduce further impact business growth.

Missing the US Picture?

While the UK business community seems to be experiencing a surge in optimism, the economic situation in the US paints a different picture. This suggests that UK business leaders may be overlooking some of the broader economic trends impacting both economies.

Conclusion:

The recent optimism of UK business leaders is a welcome sign, but it’s crucial to consider the broader economic context and potential risks. While the UK may be experiencing a temporary upswing, the challenges of high debt, stagflation, and rising unemployment remain significant. It’s important for both UK and US businesses to stay informed about the global economic situation and adjust their strategies accordingly.

Let’s discuss this further. What are your thoughts on the current economic situation in UK and the contrasting business sentiment between the UK and the US?