Banking on the Brink: BusinessRiskTV Banking Industry Forum Magazine

Welcome to the Only Place Business Leaders Dare to Ask the Real Questions About Banks

BusinessRiskTV’s Banking Industry Forum Magazine is not your average industry cheerleader. We’re the fearless voice inside the boardroom that’s tired of the smoke and mirrors. This is where hard truths meet big ideas — and business leaders like you finally get the insights you’ve been denied.

🧨 The Banking Sector Isn’t Just a Pillar of the Economy—It’s the Powder Keg

Global banks have never been more powerful… or more dangerous.

Too big to fail?

Or too bloated to function without life support?

Stabilising economies?

Or distorting them with reckless policies and short-term greed?

In this controversial but professional magazine, BusinessRiskTV lays bare the real risk drivers and unseen opportunities in the financial system that props up everything you’re building.

💼 Business Leaders Are Asking…

- What happens to UK businesses when central banks keep moving the goalposts?

- Are commercial banks still fit for purpose, or are we financing our own downfall?

- Is the next banking collapse already written into today’s financial headlines?

- Are UK SMEs and entrepreneurs being strangled by outdated lending models and global monetary groupthink?

If you’re not asking these questions, you’re already behind.

Banks Say “Trust Us” — BusinessRiskTV Says “Prove It”

Our Banking Industry Forum Magazine gives you:

✅ Unfiltered foresight on global banking trends and UK economic risk

✅ Contrarian viewpoints from independent risk analysts and thought leaders

✅ Actionable intelligence for C-suite decision-making

✅ Insider commentary on what financial regulators won’t admit publicly

✅ Spotlight analysis on the banking elite’s role in economic inequality and market manipulation

We don’t do PR. We do Business Risk Reality.

It’s Time to Think Bigger

Banks influence inflation, interest rates, consumer spending, capital flows, and ultimately the future of your business. And yet most business media tiptoe around the real issues.

We don’t.

BusinessRiskTV’s Banking Industry Forum Magazine is where bold business leaders, financial strategists, and corporate risk managers go when they’re ready to look past the headlines and make sense of what’s really happening behind the closed doors of global finance.

⚠️ If You’re Not In the Room, You’re on the Menu

Banks shape the rules of the game. But it’s your cash flow, your customers, and your company’s survival on the line. Get ahead of the curve.

Join the BusinessRiskTV Banking Industry Forum Magazine and turn knowledge into power.

🧨 Ignore it at your peril.

Bank CEOs Demand Deeper Deregulation: Why Trusting Self-Regulation is a Systemic Risk

Charlie Nunn, CEO of Lloyds Banking Group (4th December 2025), argues that while recent regulatory reforms (like the Chancellor’s Leeds Reforms) are welcome, they are “just at the start.”

His core points are:

-

Need for Further Deregulation: The government must press its deregulation mission further to significantly ramp up economic growth.

-

Deleveraging Slowdown: The current financial system’s deleveraging and de-risking has “slowed down the UK in the race over a decade.”

-

Conclusion: There is “more to do” to unleash the full potential of the financial sector and boost the economy.

Response To Banking Leaders UK As A Banking Industry Shareholder, Investor and UK Resident

The Audacity of Asking for Less Regulation

Mr. Nunn, with all due respect, your request for further deregulation reads less like a strategy for economic growth and more like a selective amnesia of the recent past. To suggest that the UK’s financial system needs more de-risking by lessening the guardrails is not just ironic; it is dangerously naive.

You speak of a “slowed down UK in the race over a decade” due to deleveraging. Let us be clear: that deleveraging was a necessary, painful, and publicly-funded inoculation against the institutionalised recklessness that nearly collapsed the entire global economy. The financial crisis was the result of the very same “self-risk management” you are now implicitly campaigning for a return to.

A Convenient Memory Lapse on “Self-Regulation”

The banking sector’s track record of self-governance is not just poor—it is an outright scandal. The fact is, banks have repeatedly proven they cannot be trusted to manage systemic risk when short-term profit incentives are in play.

Here is a reminder of what the UK’s major financial institutions have demonstrated when left to their own devices:

-

Systemic Failure: The 2008 financial crisis was the ultimate demonstration of banks’ failure to manage their own risk. It required a massive taxpayer-funded bailout, demonstrating that your sector’s “self-management” only works until the point of crisis, at which time the public is forced to pay the bill.

-

The Fine Print: When regulators do step in, the penalties are staggering and continuous, proving the controls are consistently inadequate (scroll further down this page to find even more non-exhaustive list!):

-

Barclays was fined a monumental £284 million in 2015 for poor controls in its foreign exchange business, involving collusive behaviour and sharing confidential client information.

-

NatWest was hit with a £264.7 million criminal fine in 2021 for widespread and systemic anti-money laundering (AML) failures, allowing a massive amount of criminal cash to be deposited.

-

UBS was fined £233.8 million for failings in its FX trading operations.

-

This catalogue of fines—which are just the tip of the iceberg—does not scream “ready for more freedom.” It screams, “We require diligent supervision because our internal ethics consistently yield to external pressure for profit.”

The Hilarious “Cash-Strapped” Claim

You argue the system is deleveraging and needs to ramp up growth. Yet, your argument that banks are somehow “cash-constrained” and unable to lend is simply laughable, given the reality of your balance sheets.

The truth is, UK banks currently hold billions in Central Bank Reserves with the Bank of England. These reserves have exploded due to policies like Quantitative Easing, and because the Bank of England pays interest on these reserves at the Bank Rate, major UK banks have seen their income from this “hoarding” jump by staggering amounts. For example, major banks like yours have reported income from BoE reserves that increased by over 135% in just one recent year.

You are sitting on a mountain of high-quality, safe assets, receiving a significant return for doing virtually nothing, while simultaneously claiming a lack of capital is slowing down the economy.

The capital is there. The decision to use it for safe, interest-earning reserves over the riskier, but economically vital, business of productive lending is a choice made by the banks—not a constraint imposed by over-regulation.

The Conclusion

The push for deregulation is simply a call to reintroduce the toxic incentives that led to the last crisis, allowing you to chase higher profits at the expense of systemic stability, with the comforting knowledge that the taxpayer will ultimately pick up the tab.

The Chancellor’s reforms are a start, but the priority must be stable and responsible lending, not simply boosting the returns of financial institutions. The UK economy requires genuine, productive investment, not another high-stakes gamble driven by a deregulated financial sector. You have forfeited the right to a “light-touch” regime through your own documented inability to manage risk responsibly. The public needs to be protected from your sector’s “de-risking” mission, not subjected to it.

#BankingRisk #DeregulationDebate #TooBigToFail #BusinessRiskTV #RiskManagement

Navigating Economic Uncertainties as The Fed Facility Anniversary Looms

A Banker’s Guide to Prudent Risk Management in 2024

As we approach the one-year anniversary of the Federal Reserve’s emergency lending facility, a wave of uncertainty washes over the financial landscape. Memories of hundreds of U.S. banks clinging to its lifeline for survival are still fresh, serving as a stark reminder of the economic precipice we teetered on. While immediate panic has subsided, the question lingers: what happens next?

With 2024 drawing near, business leaders, particularly those in the banking sector, must adopt a proactive and strategic approach to risk management. As an economic and banking expert, I’m here to equip you with the insights and actionable steps needed to navigate the potential economic headwinds, protect your business, and emerge stronger in the coming year.

Understanding the Landscape:

The Fed’s Emergency Lending Facility: In the face of the unprecedented economic crisis triggered by SVB collapse, the Federal Reserve launched the Primary Dealer Credit Facility (PDCF) in March 2023. This lifeline provided crucial liquidity to hundreds of U.S. banks, preventing widespread bankruptcies and systemic collapse.

Lingering Uncertainties: While the PDCF served its purpose, it also masked underlying vulnerabilities within the financial system. High debt levels, geopolitical tensions, and ongoing supply chain disruptions continue to cast a shadow of uncertainty. The potential for inflation to reignite and the looming expiration of some pandemic-era support measures add further fuel to the anxiety fire.

Navigating the Risks:

As business leaders, you cannot afford to be passive observers in this turbulent landscape. Here are some key risk management actions you should prioritize:

1. Strengthen Your Balance Sheet: Now is not the time for aggressive expansion. Focus on shoring up your capital reserves, reducing bad debt, and maintaining healthy liquidity ratios. This will provide a buffer against potential shocks and ensure you have the resources to weather any coming storms.

2. Diversify Your Income Streams: Overdependence on any single market or customer segment can leave you vulnerable to unforeseen downturns. Explore new avenues for revenue generation, expand your product offerings, and enter new markets to mitigate risk and secure sustainable growth. Lloyds Bank is planning on being biggest single-family house owner with a portfolio in excess of 10000 properties.

3. Invest in Robust Risk Management Systems: Equip yourself with the tools and technology needed to proactively identify, assess, and mitigate risks. Invest in advanced data analytics, robust cybersecurity measures, and stress testing models to stay ahead of potential threats.

4. Prioritise Communication and Transparency: Open and honest communication with stakeholders, including employees, investors, and regulators, is crucial during times of uncertainty. Be proactive in sharing your risk assessments, mitigation strategies, and contingency plans to foster trust and confidence.

5. Embrace Agility and Adaptability: The economic landscape is constantly evolving, and businesses need to be agile enough to adapt. Foster a culture of innovation, encourage proactive problem-solving, and empower your teams to respond quickly and effectively to changing circumstances.

What the Future Holds:

Predicting the future is an uncertain business, but one thing is clear: a period of continued economic volatility lies ahead. By acknowledging the lingering risks, adopting a proactive approach to risk management, and implementing the actionable steps outlined above, you can position your business for success in the face of adversity.

Remember, resilience is not just about weathering the storm; it’s about emerging stronger on the other side. Embrace the challenges, seize the opportunities that arise, and lead your business through this period of uncertainty with confidence and a clear vision for the future.

This article is just the beginning of the conversation. We are providing risk management insights and guidance needed to navigate these turbulent times. Don’t hesitate to reach out for further consultations or tailored risk management strategies specific to your business needs. Together, we can navigate the complexities of the coming year and ensure your business not only survives but thrives in the new economic landscape.

Are you an ordinary business leader not involved in banking? What does all this mean for you and your business?

While the immediate threat of widespread bank failures due to the expiration of the Fed’s emergency lending facility has subsided, the potential for instability in the U.S. banking sector could still have significant impacts on ordinary business leaders, even if they’re not directly involved in finance. Here’s how:

1. Tightened Credit Access: If banks become more cautious due to economic uncertainties or increased regulations, lending might become stricter. This could make it more difficult for businesses to obtain loans and credit lines, hindering their ability to invest, expand, or even maintain ongoing operations. The money supply in America has already died and businesses are suffering major drought in money supply

2. Increased Borrowing Costs: If banks perceive higher risks in the market, they might raise interest rates on loans. This could make borrowing more expensive for businesses, further squeezing profit margins and potentially forcing them to raise prices or cut back on expenses. The cost of money has already jumped in 2023.

3. Disruptions in Financial Services: Bank failures or financial instability could cause disruptions in essential financial services like payroll processing, money transfers, and access to capital markets. This could create operational challenges and delays for businesses, impacting their cash flow and overall efficiency. Hundreds of banks, mainly regional banks, are in danger of bankruptcy.

4. Reduced Consumer Confidence: Widespread concerns about the banking sector could dampen consumer confidence, leading to decreased spending and a slowdown in economic activity. This can directly impact businesses that rely on consumer demand, resulting in lower sales and revenue. Consumers seem to be immune from realities of their future and continue to spend but savings are running out and much of the spending is on record high credit card bills.

5. Uncertainty and Market Volatility: Increased anxieties about the financial system can lead to market volatility and instability. This can make it difficult for businesses to plan for the future and invest with confidence, further hindering economic growth and job creation.

However, it’s important to remember that these are potential consequences, not inevitable outcomes. The extent of the impact on ordinary businesses will depend on various factors, including the severity of any banking sector issues, the effectiveness of government interventions, and the overall resilience of the economy.

Here are some steps ordinary business leaders can take to mitigate the risks:

- Maintain strong financial fundamentals: Focus on building cash reserves, reducing debt, and operating efficiently to weather potential disruptions.

- Diversify funding sources: Explore alternative financing options beyond traditional bank loans, such as crowdfunding, angel investors, or venture capital.

- Build strong relationships with your bank: Maintain open communication with your bank and ensure they understand your business needs. This can help you secure credit in times of uncertainty.

- Stay informed about economic developments: Monitor economic news and forecasts to stay ahead of potential disruptions and adjust your business strategies accordingly.

- Develop contingency plans: Be prepared for various scenarios, including disruptions in financial services or a slowdown in economic activity. This will allow you to react quickly and effectively to challenges.

By being proactive and prepared, ordinary business leaders can navigate the potential impacts of banking sector challenges and protect their businesses in the face of uncertainty. Remember, resilience and adaptability are key in navigating complex economic environments.

The Delusion of Certainty: Why Central Banks Can’t (and Shouldn’t) Predict the Future

My esteemed colleagues, I stand before you today to shatter a persistent illusion – the myth of central bank infallibility. Economists hang on central bank leaders every word and economic risk analysis, when they are rarely right. Some saying they are deliberately wrong for political reasons. Others that they are incompetently wrong. Either way they are normally wrong in their economic risk analysis.

For years, we’ve treated pronouncements from the Federal Reserve, the European Central Bank, and the Bank of England as gospel, their economic forecasts swaying markets and shaping our investment decisions. Yet, with each passing year, a stark reality emerges: central banks are demonstrably, embarrassingly bad at predicting the future.

To dismantle this fallacy, let’s not dwell on abstract statistics. Instead, let’s embark on a cautionary tale, delving into three concrete examples, each a testament to the folly of relying on central bank pronouncements.

Exhibit A: The ECB’s Inflation Misfire

Remember 2020? As the pandemic swept across Europe, the European Central Bank, under Christine Lagarde’s leadership, assured us that inflation would remain subdued, even dip below their target of 2%. They argued that the economic slump would dampen price pressures, lulling businesses and policymakers into a state of comfortable complacency. Fast forward to 2023, and reality bites with the force of a tidal wave. Eurozone inflation sits at a record-breaking 10.6%, shattering the ECB’s predictions and triggering an economic maelstrom. Businesses grapple with skyrocketing costs, eroded profits, and consumer anxieties, all while the ECB scrambles to contain the inflationary fire it downplayed for far too long.

Exhibit B: The Bank of England’s Brexit Blundermark

Across the English Channel, the Bank of England, led by Mark Carney, infamously predicted a 7.5% contraction in GDP immediately following the UK’s Brexit vote in 2016. This dire pronouncement sent shockwaves through markets, prompting businesses to freeze investments and consumers to hoard cash. Yet, reality once again defied the Bank’s doomsday prophecy. The UK economy exhibited remarkable resilience. Growth slowed, but nowhere near the predicted freefall. The Bank’s miscalculation not only caused unnecessary panic but also cast a long shadow of doubt on its economic forecasting prowess – and political independence or lack there of.

Exhibit C: The Fed’s 2008 Blind Spot

Returning across the Atlantic, let’s rewind to 2008. The Federal Reserve, then led by Ben Bernanke, consistently downplayed the severity of the subprime mortgage crisis, assuring markets that the housing market slowdown was “contained.” They maintained this rosy assessment even as ominous warning signs, like falling home prices and spiking delinquencies, became increasingly visible. This failure to recognise the looming crisis had catastrophic consequences. The US economy plunged into the Great Recession, triggering global financial turmoil and widespread economic hardship. The Fed’s miscalculation is a stark reminder that even the most powerful central banks can be blinded by hubris and misstep disastrously. The banking system has yet to fully recover from the 2008 financial crisis.

These are not isolated incidents. They are a recurring theme in the history of central banking. Time and again, pronouncements from these supposedly august institutions have proven spectacularly inaccurate, leading businesses astray and fueling market volatility.

So why are central banks so consistently wrong? The answer lies in the inherent complexity of the economic system. It’s a dynamic beast, with countless moving parts and unpredictable human actors. To attempt to predict its future with any degree of certainty is akin to navigating a fog-shrouded ocean with a broken compass.

But this doesn’t absolve central banks of their responsibility. Their pronouncements, however flawed, carry immense weight. Businesses make strategic decisions based on them, investors adjust their portfolios, and entire economies react. When these pronouncements turn out to be wrong, the consequences can be severe.

What, then, is the takeaway for astute business leaders like yourselves? The answer is simple: abandon the delusion of central bank infallibility or independence. Treat their forecasts with a healthy dose of skepticism, always conducting your own due diligence and relying on diverse sources of information. Don’t let pronouncements from Frankfurt, London, or Washington dictate your every move.

Instead, embrace the inherent uncertainty of the economic landscape. Develop agile strategies that can adapt to changing circumstances, diversify your investments, and cultivate a keen awareness of the various factors that might influence your business. Remember, the future is never set in stone, and those who cling to false certainties are most likely to be caught off guard when the tide turns.

In conclusion, let us dispel the myth of central bank infallibility. They are not omniscient oracles, but fallible humans navigating the murky waters of economic complexity. As business leaders, it’s our collective responsibility to break free from the shackles of their pronouncements and forge our own path, informed by critical thinking, sound judgment, and a healthy dose of skepticism. Only then can we truly navigate the unpredictable economic seas with confidence and resilience.

Navigating the Financial Storm: How BTFP Mitigated America’s Banking Crisis and Lessons for Global Business Leaders

As business leaders navigating the ever-changing global landscape, understanding how to manage financial risks has never been more crucial. The recent banking crisis in America serves as a stark reminder of the fragility of our interconnected financial system and the importance of proactive risk management.

In the face of this crisis, the Federal Reserve (Fed) introduced the Bank Term Funding Program (BTFP) as a critical tool to stabilize the banking system. This innovative program provided banks with access to low-cost loans secured by high-quality assets, allowing them to meet their liquidity needs and continue lending to businesses and consumers. This helped to prevent a domino effect of bank failures and maintain the flow of credit throughout the economy.

But beyond the immediate crisis, the BTFP also offers valuable lessons for business leaders worldwide:

1. Diversification of funding sources: The crisis exposed the overreliance of many banks on short-term funding sources, making them vulnerable to market fluctuations. The BTFP encouraged diversification by offering long-term financing options, highlighting the importance of a balanced funding mix for mitigating risk.

2. Liquidity management: The crisis highlighted the need for robust liquidity management strategies. By providing access to emergency funding, the BTFP helped banks weather the storm and protect their ability to meet their obligations. This reinforces the importance of maintaining adequate liquidity reserves to navigate unexpected financial challenges.

3. Importance of high-quality assets: The BTFP relied on banks holding high-quality assets as collateral, demonstrating the crucial role of asset quality in managing risk. Investing in such assets provides a buffer against market volatility and ensures access to funding during times of stress.

4. Proactive communication: The Fed’s clear and timely communication regarding the BTFP helped to calm market anxieties and restore confidence in the financial system. This underpins the importance of transparent communication with stakeholders, especially during periods of uncertainty.

While the BTFP provided a vital safety net during the crisis, it is crucial to note that it was a temporary measure. The long-term stability of the financial system requires addressing underlying vulnerabilities, such as excessive leverage and inadequate regulation.

For business leaders globally, the BTFP serves as a case study in effective risk management. By diversifying their funding sources, maintaining ample liquidity, investing in high-quality assets, and communicating transparently with stakeholders, businesses can increase their resilience and navigate the complexities of the global financial landscape with greater confidence.

Remember, managing financial risks is an ongoing process. By staying informed about new developments, adapting strategies to changing circumstances, and learning from the experiences of others, business leaders can ensure their long-term success in an increasingly volatile world.

How much cash do US, UK and EU fractional reserve banks need to keep to protect against a bank run in percentage terms?

Keith Lewis 7 November 2023

Introduction

Fractional reserve banking is a system in which banks are required to keep only a fraction of their deposits in reserve, meaning that they can lend out the rest. This system allows banks to create new money in the economy, but it also makes them vulnerable to bank runs, which occur when depositors withdraw their money en masse.

To protect against bank runs, fractional reserve banks need to keep a certain amount of cash in reserve. This percentage is known as the reserve requirement. The reserve requirement is set by the central bank, and it can vary from country to country.

In the United States, the Federal Reserve System (Fed) sets the reserve requirement. As of November 2023, the reserve requirement is 0% for all banks. This means that banks are not required to keep any of their deposits in reserve.

In the United Kingdom, the Bank of England (BoE) sets the reserve requirement. As of November 2023, the reserve requirement is 10% for all banks. This means that banks must keep 10% of their deposits in reserve.

In the European Union, the European Central Bank (ECB) sets the reserve requirement. As of November 2023, the reserve requirement is 1% for all banks. This means that banks must keep 1% of their deposits in reserve.

How much cash do banks need to keep to protect against a bank run?

The amount of cash that banks need to keep to protect against a bank run depends on a number of factors, including the size of the bank, the type of deposits that the bank holds, and the overall level of confidence in the banking system.

In general, larger banks need to keep more cash in reserve than smaller banks. This is because larger banks have more depositors, and therefore they are more vulnerable to a bank run.

Banks that hold more volatile deposits, such as demand deposits (checking accounts), need to keep more cash in reserve than banks that hold less volatile deposits, such as time deposits (savings accounts). This is because demand deposits are more likely to be withdrawn quickly in the event of a bank run.

During times of financial stress, when confidence in the banking system is low, banks may need to keep more cash in reserve. This is because depositors are more likely to withdraw their money during times of financial stress.

How much cash do US, UK and EU banks keep in reserve?

As of November 2023, US banks hold an average of 8.5% of their deposits in reserve. UK banks hold an average of 13.5% of their deposits in reserve. EU banks hold an average of 1.5% of their deposits in reserve.

It is important to note that these are just averages. The amount of cash that individual banks hold in reserve can vary significantly.

How can banks protect themselves from bank runs?

There are a number of things that banks can do to protect themselves from bank runs. One important measure is to maintain a healthy capital position. This means having enough equity and retained earnings to cover losses.

Banks can also protect themselves from bank runs by investing in a diversified portfolio of assets. This helps to reduce the bank’s risk exposure in the event of a downturn in any particular sector of the economy.

Finally, banks can protect themselves from bank runs by maintaining a good reputation. This means being transparent about their financial condition and being responsive to the needs of their customers.

Conclusion

The amount of cash that US, UK and EU fractional banks need to keep to protect against a bank run depends on a number of factors, including the size of the bank, the type of deposits that the bank holds, and the overall level of confidence in the banking system.

In general, larger banks need to keep more cash in reserve than smaller banks. Banks that hold more volatile deposits need to keep more cash in reserve than banks that hold less volatile deposits. During times of financial stress, when confidence in the banking system is low, banks may need to keep more cash in reserve.

As of November 2023, US banks hold an average of 8.5% of their deposits in reserve. UK banks hold an average of 13.5% of their deposits in reserve. EU banks hold an average of 1.5% of their deposits in reserve.

There are a number of things that banks can do to protect themselves from bank runs, including maintaining a healthy capital position, investing in a diversified portfolio of assets, and maintaining a good reputation.

How can the banking industry stop destroying wealth via poor risk management decision-making

Banking Forums to inform banking risk management. What are the biggest threats to the banking industry? What opportunities are there for banking industry growth? Network with top banking industry business leaders. Pick up banking industry risk news for free. Join banking industry risk management events. Learn more about the best banking industry risk management solutions. Network with banking experts around the world with BusinessRiskTV.

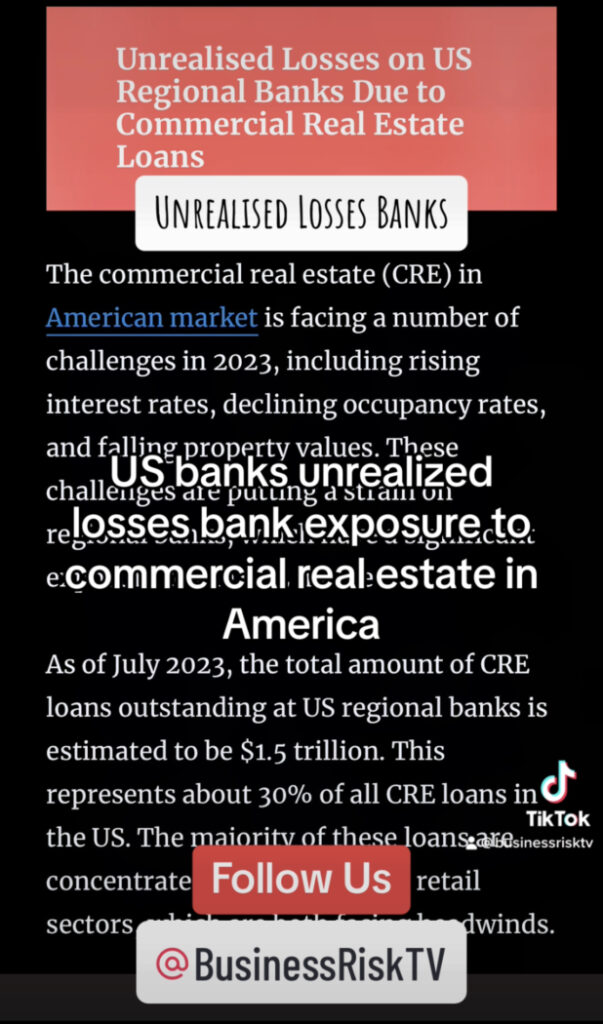

Unrealised Losses on US Regional Banks Due to Commercial Real Estate Loans

The commercial real estate (CRE) in American market is facing a number of challenges in 2023, including rising interest rates, declining occupancy rates, and falling property values. These challenges are putting a strain on regional banks, which have a significant exposure to the CRE market.

As of July 2023, the total amount of CRE loans outstanding at US regional banks is estimated to be $1.5 trillion. This represents about 30% of all CRE loans in the US. The majority of these loans are concentrated in the office and retail sectors, which are both facing headwinds.

The rising interest rate environment is making it more difficult for borrowers to repay their CRE loans. This is because the interest payments on these loans are becoming more expensive. As a result, some borrowers are defaulting on their loans, which is leading to losses for regional banks.

In addition to rising interest rates, the CRE market is also facing declining occupancy rates. This is because many businesses are downsizing their office space or closing their retail locations. As a result, there is a surplus of commercial real estate on the market, which is putting downward pressure on property values.

The combination of rising interest rates, declining occupancy rates, and falling property values is creating a perfect storm for regional banks. These banks are facing a number of challenges, including:

- Increased risk of loan defaults

- Decreased asset values

- Increased funding costs

These challenges are likely to lead to losses for regional banks. As of July 2023, the total amount of unrealised losses on CRE loans at US regional banks is estimated to be $100 billion. This represents about 7% of the total amount of CRE loans outstanding at these banks.

The level of unrealised losses on CRE loans is likely to increase in the coming months. This is because the challenges facing the CRE market are not expected to improve anytime soon. As a result, regional banks are likely to face significant losses in 2023.

How many banks closed during the Great Recession?

During the Great Recession, which lasted from 2007 to 2009, a total of 456 banks failed in the United States. This was the highest number of bank failures since the Great Depression. The majority of these bank failures were caused by losses on commercial real estate loans.

What is the H 8 statistical release?

The H 8 statistical release is a weekly report that provides data on the reserve balances of US banks. This data includes the amount of required reserves, excess reserves, and borrowed reserves held by banks. The H 8 release is published by the Federal Reserve Bank of New York.

Why the development of overnight loan markets made it more likely that banks will hold fewer excess reserves?

The development of overnight loan markets has made it more likely that banks will hold fewer excess reserves. This is because banks can now borrow reserves from other banks on an overnight basis if they need to. As a result, banks are less likely to hold excess reserves as a buffer against unexpected withdrawals.

What happens if a deposit outflow of $50 million occurs?

If a deposit outflow of $50 million occurs, a bank will need to either reduce its lending or borrow reserves from other banks. If the bank reduces its lending, it will likely lead to a decrease in economic activity. If the bank borrows reserves from other banks, it will likely have to pay a higher interest rate.

Conclusion

The commercial real estate market is facing a number of challenges in 2023, which is putting a strain on regional banks. These challenges are likely to lead to losses for regional banks in the coming months. The level of unrealised losses on CRE loans is likely to increase in the coming months. As a result, regional banks are likely to face significant losses in 2023.

It seems that it is really hard for many bankers to manage the risks from banking

Approaching two decades after the last financial industry crisis, many of the biggest banks are still destroying shareholder value by failing to manage banking business risks somewhere near the standard expected of them. As a result, we are only a hop skip and a jump from the next financial crisis at any point in time. The problem is that as bankers can’t manage banking risks we cannot have a resilient banking industry that contributes reliably to bank shareholders wealth and income, a strong global economy and a sustainable society.

30 examples of bank fines or penalties imposed by regulators since financial crash 2008 destroying shareholder value:

- In 2018, Wells Fargo was fined $1 billion by the Consumer Financial Protection Bureau (CFPB) for abusive lending practices.

- In 2014, JPMorgan Chase was fined $2.6 billion by various regulators for their role in the Madoff Ponzi scheme.

- In 2015, Citigroup was fined $700 million by various regulators for manipulating the foreign exchange market.

- In 2016, Bank of America was fined $415 million by the CFPB for illegal credit card practices.

- In 2019, Goldman Sachs was fined $2.9 billion by various regulators for their role in the 1MDB scandal.

- In 2018, Barclays was fined $2 billion by various regulators for manipulating the foreign exchange market.

- In 2017, Deutsche Bank was fined $630 million by various regulators for money laundering.

- In 2019, UBS was fined $5.1 billion by French regulators for tax evasion.

- In 2014, BNP Paribas was fined $8.9 billion by various regulators for violating U.S. sanctions.

- In 2018, Standard Chartered was fined $1.1 billion by various regulators for violating U.S. sanctions.

- In 2016, Societe Generale was fined $1.3 billion by various regulators for violating U.S. sanctions.

- In 2017, Credit Suisse was fined $536 million by various regulators for violating U.S. sanctions.

- In 2019, Danske Bank was fined $230 million by various regulators for money laundering.

- In 2018, Rabobank was fined $369 million by various regulators for money laundering.

- In 2015, HSBC was fined $1.9 billion by various regulators for money laundering.

- In 2016, Mitsubishi UFJ Financial Group was fined $622 million by various regulators for money laundering.

- In 2018, Royal Bank of Scotland was fined $4.9 billion by the U.S. Department of Justice for their role in the financial crisis.

- In 2014, Bank of America was fined $16.65 billion by the U.S. Department of Justice for their role in the financial crisis.

- In 2016, Wells Fargo was fined $185 million by the CFPB for creating fake accounts.

- In 2018, UBS was fined $15 million by the U.S. Securities and Exchange Commission (SEC) for violations related to municipal bond offerings.

- In 2017, Citigroup was fined $25 million by the SEC for spoofing.

- In 2019, Morgan Stanley was fined $10 million by the SEC for violating regulations related to short selling.

- In 2018, JPMorgan Chase was fined $65 million by the SEC for mishandling American Depository Receipts.

- In 2016, Deutsche Bank was fined $55 million by the SEC for mishandling pre-release American Depository Receipts.

- In 2019, Societe Generale was fined $1.3 billion by various regulators for violating U.S. sanctions.

- In 2016, Credit Suisse was fined $90 million by the SEC for misrepresenting the performance metric of a complex product.

- In 2017, Goldman Sachs was fined $120 million by the SEC for mishandling “pre-released” American Depository Receipts.

- In 2018, Santander was fined $11.8 million by the SEC for improperly handling customer accounts.

- In 2019, Western Union was fined $585 million by various regulators for facilitating fraudulent transactions.

- In 2020, Commerzbank was fined $47 million by German regulators for failing to implement adequate money-laundering controls.

Register to Banking Industry Risk Management Forum for free alerts to alerts bulletins and reviews to your inbox

Our banking industry forum is designed to look holistically at the challenges of a progressive bank and identify better ways of doing things.

Enter code #BankingIndustryForum

What do you need to know about banking industry risk management in our Banking Industry News Trends Risks Analysis

Subscribe to BusinessRiskTV Banking Industry Forum

#BusinessRiskTV #Banking #BankingRisks #BankingForum #BankingIndustry #BankingIndustryForum #BankingRiskManagement #BankingMagazine #BankingNews #BankingIndustry RiskForum #BankingReview #BankingReports #BankingLeaders

Discover better ways to protect and grow your business with BusinessRiskTV

The New Reality of Banking: How to Manage Uncertainty and Build a Shock-Proof Bank

The ECB’s Stark Warning: Navigating the New Reality of Constant Shocks in Banking

The European Central Bank (ECB) has moved beyond forecasting the next recession. Its new, urgent message to the financial sector is that the era of predictable business cycles is over. Banks now operate in a “new reality” defined by more frequent and diverse shocks—from geopolitical tariffs to devastating cyberattacks. The critical takeaway for business leaders is that resilience is no longer about predicting the exact nature of the next crisis, but about being prepared for a range of possibilities. This post provides a business risk management analysis of this new paradigm and outlines a strategic framework for building a truly resilient bank.

Deconstructing the “New Reality”: From Predictable Cycles to Constant Disruption

The traditional risk management model, which often relied on historical data and linear projections, is becoming obsolete. The ECB highlights a shift towards a more volatile and interconnected threat landscape. This “new reality” is characterised by:

· High-Frequency Shocks: Crises are no longer once-in-a-decade events. They are recurring, overlapping events that strain resources and recovery capabilities.

· Diverse Threat Origins: The sources of risk are no longer purely financial. They are multi-faceted, blending physical, digital, and geopolitical domains.

· The “Unknown Unknown”: The central challenge is the inability to pinpoint the next major disruption, making specific contingency plans insufficient.

Key Risk Categories in the ECB’s New Reality

To operationalise this warning, banks must broaden their risk assessment. The following categories represent the modern shock landscape:

1. Geopolitical & Economic Shocks (e.g., Tariffs): Sudden trade barriers, sanctions, or commodity price spikes can disrupt global supply chains, impact client solvency, and create volatile market conditions.

2. Cyber & Technological Shocks: Sophisticated cyberattacks on critical infrastructure or a bank’s own systems threaten operational continuity, data integrity, and customer trust. This also includes risks from third-party tech providers.

3. Climate & Environmental Shocks: Physical risks (e.g., floods, wildfires damaging assets) and transition risks (e.g., rapid policy changes devaluing carbon-intensive portfolios) are becoming significant financial threats.

4. Socio-Political Shocks: Social unrest, pandemics, or rapid regulatory changes can alter the operating environment overnight, affecting everything from staffing to compliance costs.

A Strategic Framework for Building Bank Resilience

Moving from awareness to action requires a fundamental shift in risk management strategy. Banks must build foundational resilience that is effective across multiple scenarios.

1. From Siloed Risk to Integrated Enterprise Risk Management (ERM)

Break down the silos between credit, market, operational, and cyber risk teams. An integrated ERM framework provides a holistic view of the bank’s risk profile, allowing for the identification of correlated and cascading risks—where a shock in one area (e.g., a tariff) triggers a crisis in another (e.g., client loan defaults).

2. Embrace Scenario Planning Over Single-Point Forecasting

Instead of asking “What is the most likely outcome?”, banks should continuously ask “What would we do if…?”.

· Develop Plausible, Severe Scenarios: Model the impact of combined shocks, such as a major cyberattack during a period of trade tension.

· Stress Test for Multiple Variables: Ensure capital and liquidity are adequate to withstand several different severe-but-plausible scenarios, not just one regulatory stress test.

3. Invest in Operational Resilience & Cyber Defences

Operational continuity is the bedrock of survival. This involves:

· Robust Business Continuity & Disaster Recovery (BC/DR): Regularly tested plans that ensure critical operations can continue during a disruption.

· Advanced Cybersecurity: Going beyond compliance to implement proactive threat detection, multi-layered defence systems, and comprehensive incident response plans.

· Third-Party Risk Management: Rigorously assessing the resilience of key vendors and partners in your supply chain.

4. Foster an Adaptive and Risk-Aware Culture

Technology and plans are useless without the right people. Resilience must be cultural.

· Leadership Tone: Executives must consistently communicate the importance of vigilance and adaptability.

· Empowered Decision-Making: Enable staff at all levels to identify and respond to emerging risks quickly, without being hindered by bureaucracy.

· Continuous Training: Regularly train employees on new threats, from phishing scams to the financial implications of climate policy.

Conclusion: Resilience as a Competitive Advantage

The ECB’s message is clear: the goal is not to become a fortune-teller, but to become shock-proof. By accepting this “new reality,” banks can transform their risk management function from a defensive cost centre into a strategic advantage. A bank that can demonstrate robust resilience to regulators, investors, and customers will not only survive the next unknown crisis but will also be positioned to thrive in its aftermath. The time to build that foundation is now, before the next shock arrives.

—

#BankingResilience

#RiskManagement

#FutureOfFinance

Bank of England Policy: A Business Risk Analysis for UK Leaders

BusinessRiskTV.com

#UKBusiness #BoEPolicy #QuantitativeTightening #BusinessRiskTV #ProRiskManager

The Bank of England (BoE) is using its repo (repurchase agreement) facility as a primary tool to manage liquidity in the financial system while simultaneously continuing quantitative tightening (QT). The key reason for this approach is that the BoE is moving away from the unconventional monetary policy of quantitative easing (QE) and returning to a more conventional framework where interest rates are the main tool for controlling inflation.

Repo Facility vs. Quantitative Easing

The BoE is using its repo facility instead of QE because these are two very different tools with distinct purposes.

Quantitative Easing (QE) is a large-scale, unconventional monetary policy tool used to lower long-term interest rates and stimulate economic activity, especially when short-term interest rates (like the Bank Rate) are already at or near zero. The BoE creates new digital money to buy assets, primarily UK government bonds (gilts), which injects money directly into the financial system and expands the BoE’s balance sheet. This pushes down on long-term borrowing costs, encourages lending, and supports asset prices.

The Repo Facility is a more conventional liquidity management tool. It’s a short-term lending operation where the BoE lends cash to commercial banks and other eligible institutions in exchange for high-quality collateral, such as gilts. The BoE’s short-term repo (STR) facility provides a way for banks to borrow reserves from the central bank. This is a mechanism to ensure the financial system has enough liquidity to function smoothly and to manage the distribution of reserves, not to stimulate the broader economy on a massive scale.

The BoE is using the repo facility to provide banks with reserves as it shrinks its balance sheet through quantitative tightening, a process that naturally removes reserves from the system. This allows the BoE to maintain control over short-term interest rates and ensure financial stability while letting the overall stock of reserves decline.

Rationale for Continuing Quantitative Tightening

The BoE is continuing with quantitative tightening (QT) for several key reasons:

Unwinding QE: QT is the direct reversal of QE. The BoE is selling the government bonds it bought during periods of QE or simply not reinvesting the proceeds when bonds mature. This shrinks the BoE’s balance sheet and pulls money out of the financial system, acting as a form of monetary tightening.

Controlling Inflation: High inflation is a major concern. By selling gilts, the BoE puts upward pressure on long-term interest rates, which helps to cool down the economy and bring inflation back to its 2% target.

Creating “Headroom”: The large-scale asset purchases of QE absorbed a significant amount of government debt from the market. By reducing its holdings, the BoE is making space on its balance sheet for potential future interventions should another major crisis occur. This restores the effectiveness of QE as a policy tool if it is needed again in the future.

Reducing Market Distortions: The BoE’s large-scale bond holdings can distort the gilt market, affecting price discovery and liquidity. QT helps to normalise the market for government debt.

Business Risk Analysis for UK Business Leaders

The BoE’s policy of using the repo facility while continuing with QT presents several risks for UK business leaders. The overall effect is a tightening of financial conditions that can affect everything from borrowing costs to consumer demand.

Increased Borrowing Costs: As the BoE sells gilts, it increases the supply of bonds in the market. This pushes bond prices down and their yields (the effective interest rate) up. This rise in government borrowing costs is a benchmark that directly influences the interest rates on corporate bonds, bank loans, and mortgages. Businesses looking to finance expansion, new projects, or even day-to-day operations will face higher costs of capital.

Reduced Consumer Spending: The combined effect of QT and potentially higher Bank Rate contributes to higher borrowing costs for households. This includes mortgages and other forms of consumer credit. As households face larger interest payments, their disposable income shrinks, leading to a decline in discretionary spending. For businesses, this means a potential fall in consumer demand for goods and services.

Weakened Investment: Higher borrowing costs make new investments less attractive. Projects that might have been profitable with lower interest rates may no longer be viable. This can lead to a slowdown in business investment, impacting long-term growth and productivity.

Heightened Market Volatility: The process of QT is unprecedented in its scale. The constant selling of gilts by the BoE, combined with the government’s need to issue new debt, creates a dynamic and potentially volatile gilt market. This market instability can create uncertainty for businesses and investors, making it harder to plan and manage financial risks.

Credit Crunch Risk: While the repo facility provides a backstop for banks, the overall reduction in reserves from QT could, in an extreme scenario, lead to a tightening of lending conditions. If banks become more cautious with their reduced reserve levels, they may reduce the availability of credit to businesses, leading to a credit crunch that could harm even healthy firms.

Six Ways to Protect Your Business

UK business leaders can take proactive steps to mitigate the negative repercussions of the Bank of England’s policy.

Hedge Against Interest Rate Risk: Use financial instruments like interest rate swaps or caps to fix or limit the interest rate on your debt. This provides certainty and protects your business from the risk of rising borrowing costs, allowing for more stable financial planning.

Optimise Your Cash Flow: Focus on improving operational efficiency to generate more cash internally. This reduces the need to borrow and makes the business less vulnerable to high interest rates. Consider optimising inventory, tightening credit terms for customers, and delaying non-essential capital expenditures.

Diversify Your Funding Sources: Do not rely on a single source of financing. Explore a mix of funding options, including bank loans, corporate bonds, asset-based lending, and equity financing. This reduces your exposure to any one lender or market and can help secure more favorable terms.

Strengthen Your Balance Sheet: Build up cash reserves and reduce debt where possible. A strong balance sheet provides a crucial buffer against economic shocks and gives you the flexibility to invest or withstand a downturn without needing to take on expensive new debt.

Re-evaluate Your Business Model: In a climate of reduced consumer spending and higher costs, it is vital to assess the resilience of your business model. Can you pass on some of the increased costs to customers? Can you find efficiencies in your supply chain? Focus on pricing power and cost-cutting to maintain profitability.

Maintain Strong Relationships with Lenders: Engage in open and proactive communication with your banks and other lenders. By demonstrating a clear understanding of your financial position and a sound strategy for navigating the economic environment, you can secure better terms and ensure continued access to credit, even as the broader market tightens.

Goldman Sachs UK Employee Count

Goldman Sachs UK: “Stable” Headcount Hides a Shifting City Landscape

London, UK – Forget the mass exodus. Despite Brexit’s shadow, Goldman Sachs’ UK headcount in 2025 appears surprisingly resilient, hovering around its pre-referendum levels of approximately 6,000. But for business leaders, this “stability” should raise more questions than it answers.

Beneath the headline figure lies a subtle, yet significant, transformation. While front-office roles have seen some shifts to European hubs, a quiet expansion in support, risk, and technology functions is evident in London. This isn’t just about shuffling desks; it’s a re-evaluation of London’s role within the global financial powerhouse.

Is London becoming the back-office brain of Goldman’s European operations? And as Goldman Sachs Chairman David Solomon highlights the increasing “mobility” of talent, what does this mean for the UK’s long-term competitive edge in attracting and retaining the best financial minds? Business decision-makers must look beyond the static numbers and understand the nuanced reallocation of roles that defines London’s evolving financial landscape. The implications for skills, infrastructure, and future investment are profound.

UK Bank Ringfence Risks

The potential decision by Rachel Reeves to dismantle the UK’s bank ringfencing rules marks a significant shift in financial policy. The 15-year-old regulation, separating retail banking from riskier investment activities, was designed to protect depositors and prevent another taxpayer-funded bailout. The proposed repeal, driven by industry pressure, aims to boost the sector’s international competitiveness and spur economic growth by freeing up capital. Proponents argue it would unlock billions and allow UK banks to operate more efficiently.

However, three downside risks are evident. First, the move could re-expose the UK financial system to the “too big to fail” problem, increasing systemic risk. Without a firewall, a failing investment arm could bring down the retail side, necessitating government intervention. Second, it could divert capital away from domestic lending for households and businesses, as banks prioritise more profitable, global investment opportunities. Third, it risks regulatory arbitrage, potentially fuelling the growth of a less-regulated “shadow banking” sector, which could create new vulnerabilities outside the traditional system. The Bank of England has voiced caution, highlighting the potential for negative effects on UK lending and financial stability.

USA : According to the 2022 CFA Institute Investor Trust Study, 94% of state and local pension plans had some crypto exposure.