The Bank of England’s recent record £87.15 billion repo allotment, a tool used to provide liquidity to banks as the central bank reduces its bond holdings, could signal underlying stress in the UK banking sector. This growing reliance on the central bank for funds raises a red flag for the financial stability and economic safety of the UK. Discover what this means for the wider economy and learn six crucial risk management strategies every business leader should implement now to protect and grow their enterprise more resiliently in an uncertain economic climate.

Bank of England Allots Record £87.15 Billion in Repo Operation: What It Means for UK Business Risk

The Bank of England’s Record Repo Allotment: A Warning for UK Business? 🚨

The Bank of England recently allotted a record £87.15 billion in a short-term repo operation, a move that provides a substantial injection of liquidity into the UK’s banking system. While this may seem like a routine technical adjustment by the central bank, the increasing reliance on these operations could be a significant red flag for the safety of the UK’s financial system and wider economy.

What Is a Repo Operation and Why Is This a Red Flag?

A repo (repurchase agreement) is essentially a short-term loan. The Bank of England lends money to commercial banks and in return, the banks provide high-quality assets (like government bonds) as collateral. The Bank’s increasing use of this tool is directly linked to its Quantitative Tightening (QT) programme, which involves selling off the government bonds it bought during the era of Quantitative Easing (QE). The purpose of these repo operations is to prevent a potential liquidity squeeze in the financial system as the central bank reduces its balance sheet.

The record allotment is a red flag for a few key reasons:

Growing Illiquidity: The fact that banks are demanding a record amount of funds from the central bank suggests they may be struggling to find liquidity elsewhere in the market. This could indicate underlying stress in the banking sector and a reluctance among banks to lend to each other.

Systemic Risk: This reliance on the Bank of England for funding could be a sign of increased systemic risk. If a major bank were to face a sudden liquidity crisis, the central bank would be its lender of last resort. The increasing size of these operations shows the potential scale of that reliance.

Uncertainty and Instability: A record-breaking allotment, particularly one that exceeds a recent record, creates a narrative of growing instability. This can erode confidence in the banking system and the wider economy, making businesses and investors more hesitant to spend and invest. This uncertainty trickles down to businesses and consumers, affecting everything from investment decisions to household spending.

6 Risk Management Measures for Businesses

In an environment of economic uncertainty, business leaders must be proactive to protect their organisations. Here are six essential risk management measures to enhance resilience:

Strengthen Cash Flow and Liquidity:Cash is king, especially in a downturn. Focus on optimising your working capital by accelerating accounts receivable, negotiating longer payment terms with suppliers, and maintaining a healthy cash reserve. Create detailed cash flow forecasts to anticipate potential shortfalls and manage expenses.

Diversify Revenue Streams and Supply Chains:Over-reliance on a single product, service, customer, or supplier is a major vulnerability. Actively seek new markets, customer segments, and partnerships. For your supply chain, identify alternative vendors and consider strategies like near-shoring or holding a small buffer of critical inventory to mitigate potential disruptions.

Manage Debt and Capital Expenditure Wisely: During uncertain times, it is crucial to avoid taking on excessive debt. Evaluate all major capital expenditure projects. Postpone or cancel non-essential investments that don’t directly contribute to immediate revenue or operational efficiency.

Review and Optimise Operational Costs:Take a hard look at all business expenses. Eliminate unnecessary costs without sacrificing the quality of your product or service. This could involve renegotiating contracts, leveraging technology for greater efficiency, or consolidating services. The goal is to create a leaner, more resilient cost structure.

Why the Bank of England’s Record Repo Allotment Is a Red Flag

The Bank of England’s record-breaking repo allotment is a significant red flag because it points to potential underlying stress and growing liquidity issues within the UK banking system. While repo operations are a standard tool for central banks to manage monetary policy, the increasing size of these allotments, especially in the context of the central bank’s quantitative tightening (QT) programme, reveals a deeper problem.

Growing Illiquidity and Inter-bank Distrust: The primary role of a central bank’s repo operation is to provide liquidity. A record amount being requested by commercial banks suggests they are struggling to secure the funds they need from each other. In a healthy banking system, banks would lend to one another in the inter-bank market. The fact that they are turning to the Bank of England in such high volumes could indicate a breakdown of trust between financial institutions, which is a classic symptom of a stressed system.

Systemic Risk: The increasing reliance on the central bank for funding raises concerns about systemic risk. Systemic risk is the risk of a collapse of an entire financial system due to the failure of one or more institutions. If a significant portion of the banking sector is dependent on the Bank of England for liquidity, a sudden shock or disruption could have a cascading effect across the entire system. This over-reliance makes the financial system less resilient and more vulnerable to unforeseen events.

Uncertainty and Economic Instability: A record repo allotment creates a sense of uncertainty and instability in the market. The public and investors may interpret this as a signal that the banking system is not as robust as it appears. This loss of confidence can have a tangible impact on the wider economy. It can lead to a tightening of lending standards, making it harder for businesses and households to access credit, and it can also deter investment, ultimately slowing down economic growth. The large allotment, therefore, isn’t just a technical exercise; it’s a barometer of growing financial vulnerability in the UK.

Read more free business risk management articles and view videos

6 Essential Business Risk Management Measures for UK Business Leaders

In today’s complex and uncertain economic environment, proactive business risk management is no longer an option—it’s a necessity. UK business leaders must move beyond a reactive approach and build genuine resilience into the core of their operations. Here are six essential measures to take action on now.

Optimise working capital: Focus on accelerating accounts receivable by offering incentives for early payment or enforcing stricter payment terms. At the same time, negotiate more favourable payment terms with your suppliers to extend your accounts payable.

Create robust cash flow forecasts: Use financial modelling and scenario planning to predict potential cash shortfalls. This will help you anticipate problems and give you time to secure financing or make cost adjustments before a crisis hits.

Maintain a cash reserve: Aim to build a buffer of cash sufficient to cover at least three to six months of operating expenses. This reserve acts as a critical safety net against unexpected disruptions.

2. Diversify Revenue Streams and Supply Chains

Over-reliance on a single customer, product, or supplier is a major vulnerability. Diversification builds a more robust and flexible business model.

Review and diversify your supply chain: Identify and vet alternative suppliers, especially for critical raw materials or components. Consider a dual-sourcing model or incorporating local suppliers to mitigate risks from global transport issues or geopolitical events.

3. Conduct Scenario Planning and Stress Testing

Don’t wait for a crisis to expose your weaknesses. Proactive scenario planning allows you to test your business model against a range of potential threats.

Identify key risks: Create a comprehensive risk register that outlines potential risks (e.g., economic downturn, supply chain disruption, cyber-attack) and their potential impact.

High levels of debt can become a significant burden in a tightening credit environment.

Limit new borrowing: Be cautious about taking on new debt, particularly for non-essential projects. Evaluate every borrowing decision based on its potential return on investment and its impact on your balance sheet.

Re-evaluate capital projects: Postpone or cancel major capital expenditures that are not critical for business operations or do not have a clear and immediate path to profitability. Prioritize investments that enhance operational efficiency and resilience.

5. Review and OPTIMISE Operational Costs

A lean and efficient cost structure improves profitability and allows you to better weather economic storms.

Targets decision-makers searching for the financial impact of weak risk practices

THE HIDDEN TAX OF POOR RISK MANAGEMENT

Your business is leaking money. Not in the obvious ways — like overspending or inefficiency — but in silent, insidious drains you might not even see. Poor risk management isn’t just about avoiding disasters; it’s a profit killer, a growth stifler, and, in the worst cases, an executioner of businesses that could have thrived.

Consider this: 30% of bankruptcies are due to operational failures that could have been mitigated with better risk practices (OECD). That’s not bad luck—it’s self-inflicted. And if you think your company is immune, think again.

This isn’t theoretical. Every day, businesses hemorrhage cash through:

Employee disengagement —teams that don’t see risk as their problem, costing you in errors, delays, and lost innovation.

The result? Lower profitability. Stunted growth. And, in extreme cases, extinction.

But here’s the good news: this is entirely optional and fixable.

In this e-book, we’ll expose the 12 most damaging costs of poor risk management —many of which you’re likely paying right now — and deliver 12 actionable solutions to turn risk from a liability into a competitive advantage. You’ll learn how to:

Engage every employee in risk ownership (not just compliance, but profit protection).

Stop financial bleed from preventable failures.

Turn risk-aware decision-making into a growth engine.

This isn’t another dry risk management manual. This is a survival guide for profitable, resilient business leadership.

Ready to plug the leaks? Let’s begin.

🚨 YOUR BUSINESS IS LEAKING £££ – FIND THE HOLES! 🚨

83% of UK SMEs lose £50k+ yearly from hidden risks they don’t even measure:

❌ Operational failures burning cash ❌Supply chain disasters killing margins

❌ Cyberattacks costing millions

BusinessRiskTV’s NEW eBook reveals:

✅ 12 PROVEN FIXES to stop profit leaks

✅ Real case studies from UK businesses

✅ Simple checklists to act TODAY

Chapter 1: The Hidden Costs of Poor Risk Management – How Ignoring Risk Erodes Your Profits and Threatens Survival

Introduction: The Silent Profit Killer

Every business faces risks—some obvious, others invisible. But when risk management is an afterthought, those risks don’t just linger; they multiply costs, shrink margins, and sabotage growth. This chapter exposes the real financial and operational toll of poor risk management—and why most businesses underestimate it.

—

1. The Direct Financial Costs: Where the Money Leaks

A. Unexpected Losses from Operational Failures

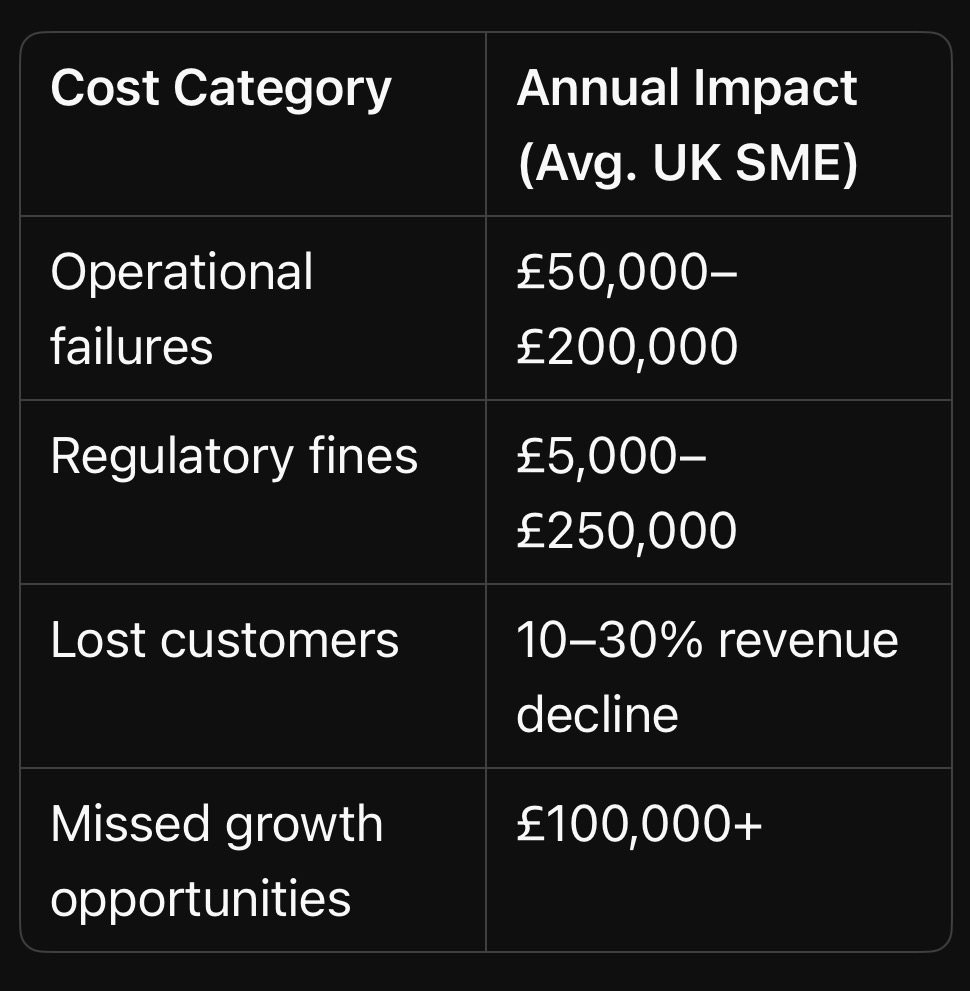

Example: A manufacturing firm ignores equipment maintenance, leading to a breakdown that halts production for 48 hours. The result? £250,000 in lost revenue + £50,000 in emergency repairs.

Stat: Companies with weak operational risk management see 30% higher unexpected costs (Deloitte).

B. Regulatory Fines & Legal Penalties

Case Study: A UK SME in financial services fails to comply with GDPR, resulting in a £180,000 fine —plus reputational damage.

Stat: 60% of small UK businesses aren’t fully compliant with key regulations (FSB).

Key Takeaway: Poor risk management isn’t just about avoiding disasters — it’s a tax on profitability, growth, and survival.

—

Actionable Insight: Audit one high-cost risk in your business this week (e.g., late payments, compliance gaps). What’s it really costing you?*

—

Chapter 2: The True Cost of Operational Failures – How Inefficient Risk Management Cripples Your Business

Introduction: The Domino Effect of Poor Operational Risk Controls

Operational risks don’t just cause one-off incidents—they trigger chain reactions that drain cash, demoralise teams, and erode customer trust. This chapter exposes the hidden, cascading costs of mismanaged operational risks and why most businesses only see the tip of the iceberg.

—

1. The Obvious Costs: What You Can’t Ignore

A. Downtime & Lost Production

Manufacturing Example: A single machine failure halts a production line for 8 hours → £25,000 in lost output + overtime costs to catch up.

Hospitality Example: A restaurant’s refrigeration breakdown spoils £3,000 of stock overnight — plus angry customers.

Stat: UK manufacturers lose £180 billion/year to unplanned downtime (EEF).

B. Emergency Repairs & Rush Orders

Reactive spending costs 3–5X more than planned maintenance.

Case Study: A logistics firm ignores fleet maintenance → two vans fail MOTs simultaneously → £8k in last-minute rentals + delayed deliveries.

C. Waste & Rework

Construction Example: Poor quality control leads to £50,000 of defective materials — then doubles labour costs to fix errors.

Stat: 20–30% of project budgets are wasted on rework (KPMG).

—

2. The Hidden Costs: What You’re Not Tracking (But Should Be)

A. Employee Productivity Drain

Scenario: A retail store’s outdated inventory system causes daily stock discrepancies. Staff waste 4 hours/day manually reconciling data instead of selling.

Stat: UK workers spend 15% of their time fixing preventable issues (PwC).

B. Management Distraction & Burnout

Small Business Reality: The owner spends 60% of their week putting out fires (supplier delays, IT crashes) instead of growing the business.

Psychological Cost: Chronic stress → poor decisions → more risks.

C. Customer Churn & Reputation Erosion

E-commerce Example: A fulfilment centre’s picking errors lead to 10% of orders arriving wrong → 15% of customers never return.

Stat: 70% of customers switch brands after just 2–3 bad experiences (Salesforce).

—

3. The Strategic Costs: How Operational Risks Stunt Growth

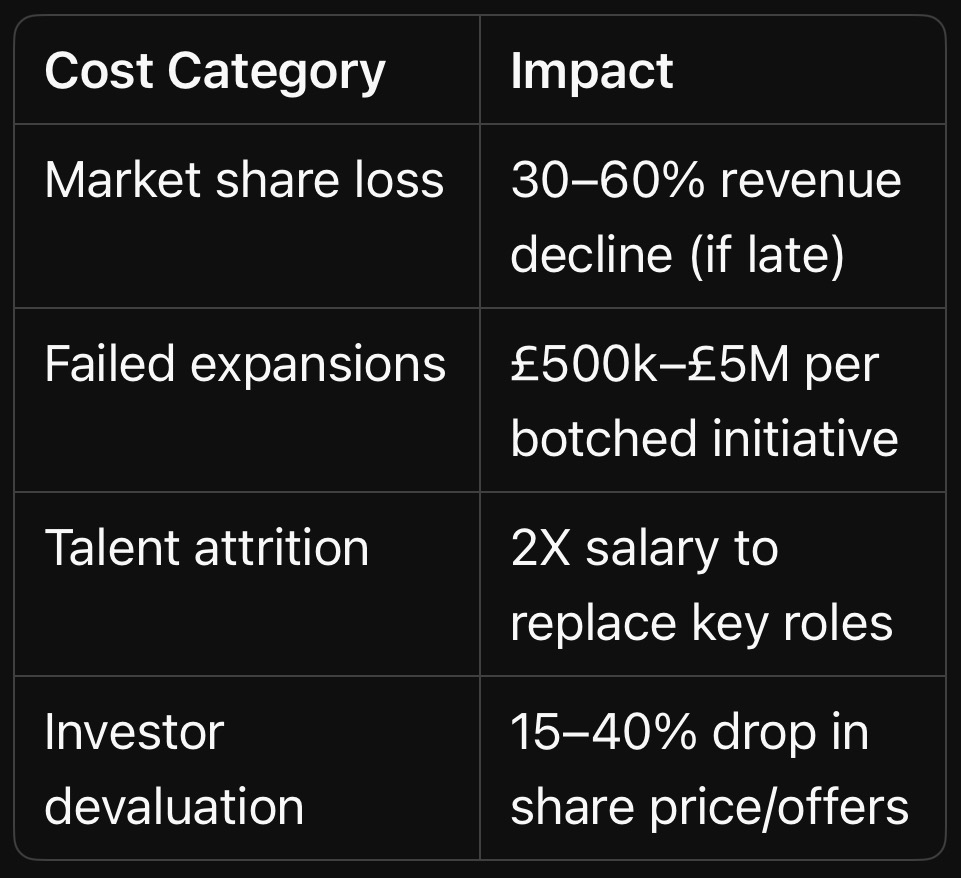

A. Lost Competitive Advantage

Case Study: A UK bakery’s unreliable oven delays a product launch by 3 months —competitors dominate supermarket shelves first.

B. Innovation Paralysis

Teams stuck in “firefighting mode” never test new ideas.

Example: A tech firm’s IT team spends 80% of time fixing outages → zero R&D progress.

C. Investor & Partner Distrust

Supply Chain Example: A fashion brand’s repeated delivery failures lead to two major retailers dropping them —£500k annual revenue gone.

—

4. The Survival Threat: When Operational Risks Become Fatal

A. Cash Flow Death Spiral

Construction Firm Case Study:

1. Poor contract risk assessment → unpaid invoices pile up

2. Equipment breakdown → project delays

3. Penalties for late delivery → bank calls in loan Result: Administration within 6 months.

B. The Carillion Effect

How ignoring operational risks (contract mismanagement, cash flow gaps) led to the UK’s biggest corporate collapse.

—

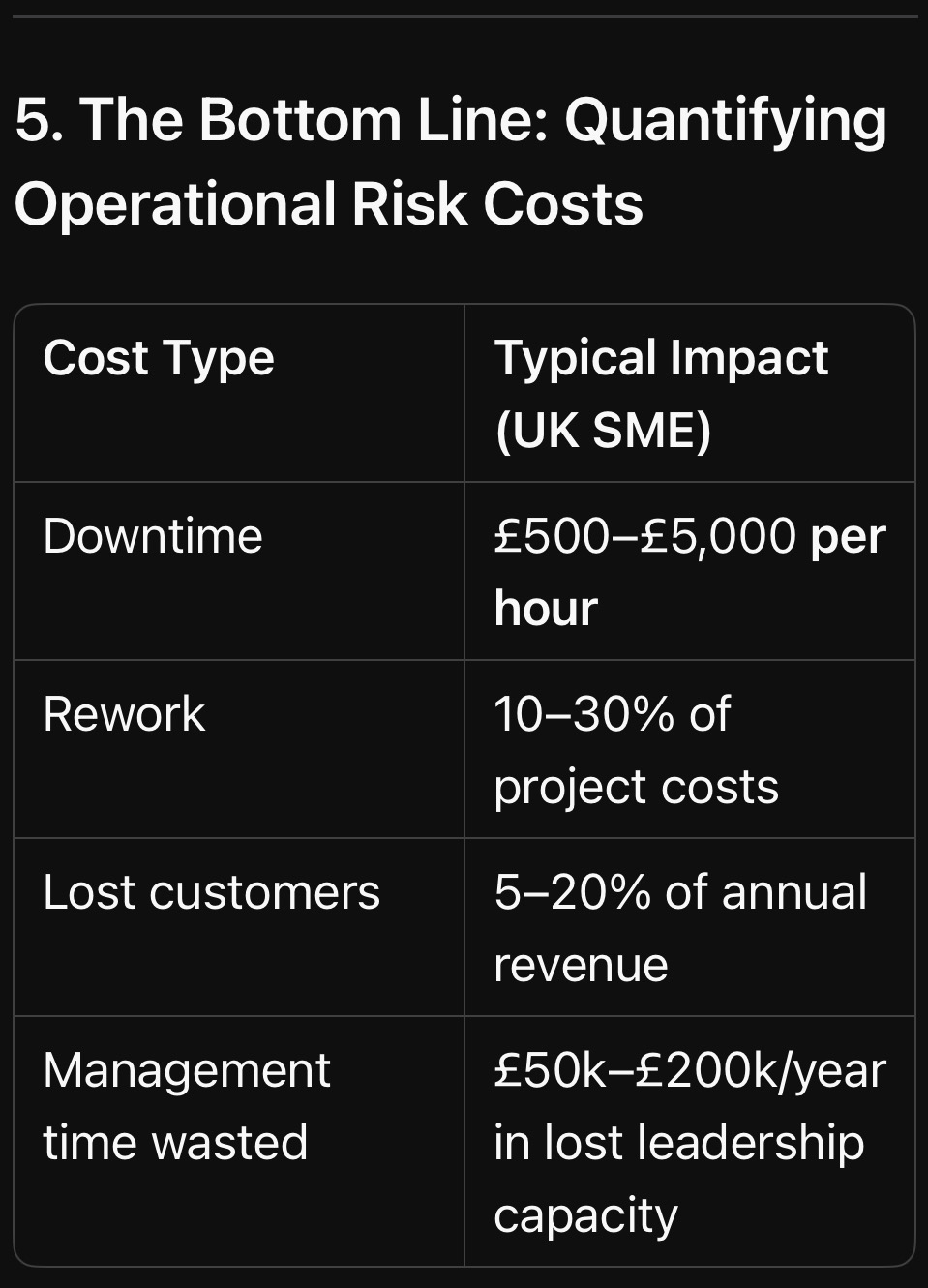

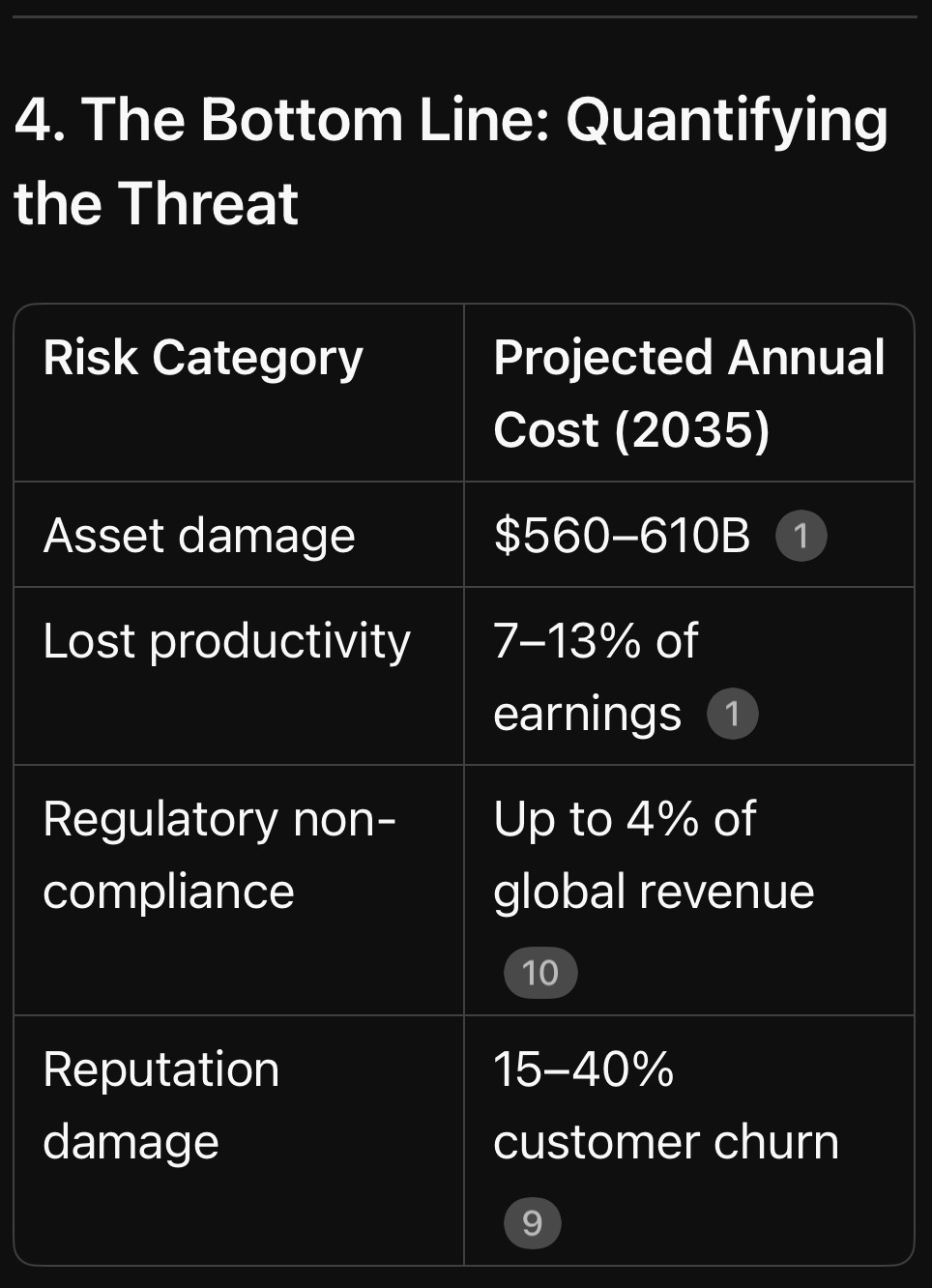

5. The Bottom Line: Quantifying Operational Risk Costs

Key Insight: Operational risks don’t just cost money—they steal time, talent, and future opportunities.

—

More From BusinessRiskTV Business Experts Hub : How to Fix It

We explore how to turn operational risk management into a profit centre, including:

The 5-minute daily habit that prevents 80% of failures

How to engage frontline teams in risk reduction (with real-world examples)

Actionable Task: Map one critical operational process (e.g., order fulfilment). Where could a single failure cost you £10k+?

—

Chapter 3: Strategic Risks – How Blind Spots in Planning Can Bankrupt Even Profitable Businesses

Introduction: The Silent Assassin of Business Growth

Strategic risks don’t announce themselves with alarms — they creep in unnoticed while leadership is distracted by day-to-day operations. By the time the damage is visible, it’s often too late to pivot. This chapter exposes how poor strategic risk management destroys market position, erodes competitive edge, and turns industry leaders into cautionary tales.

—

1. What Are Strategic Risks? (And Why They’re Different)

Key Takeaway: Strategic risks don’t just hurt profits — they erase entire business models.

—

More from BusinessRiskTV Business Experts Hub : How to Anticipate & Outmanoeuvre Strategic Risks

We explore practical frameworks to:

Spot industry shifts early (using weak signals)

Stress-test your strategy against disruption

Turn risks into opportunities (like Amazon’s pivot from books to cloud)

Actionable Task: List one strategic assumption your business relies on (e.g., “Customers will always prefer X”). How would you survive if it’s wrong?

—

Chapter 4: Financial Risks – How Poor Cash Flow & Debt Management Can Sink Your Business Overnight

Introduction: The Silent Killer of Healthy Businesses

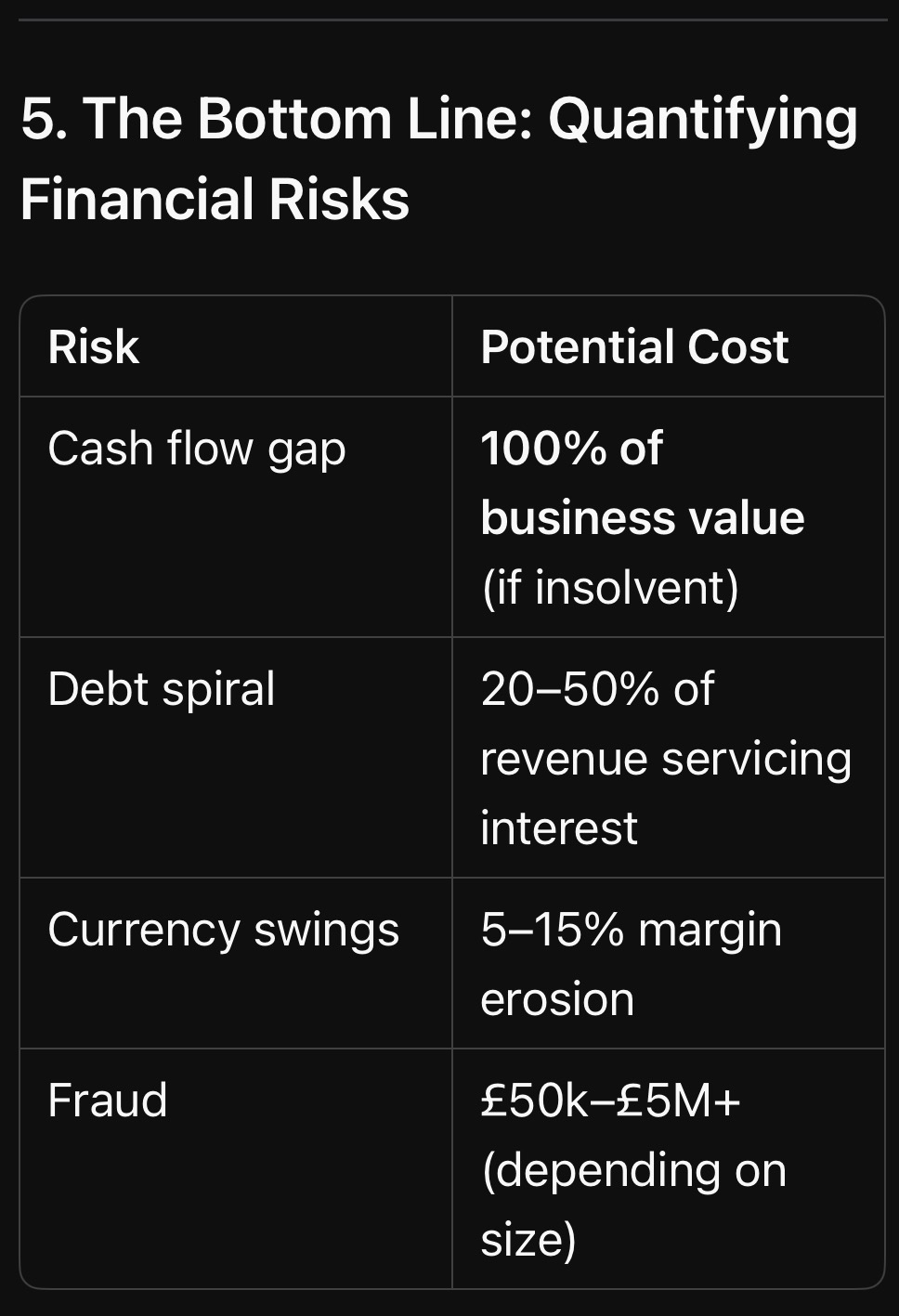

Profit doesn’t equal survival. Thousands of UK businesses post record revenues—right before going bust. Why? Because financial risk management isn’t about counting pennies — it’s about anticipating traps that strangle cash flow, trigger defaults, and collapse supply chains.

This chapter exposes the lethal financial risks hiding in plain sight — and why even profitable companies run out of money.

—

1. The Obvious (But Ignored) Financial Risks

A. Cash Flow Crises – The #1 Business Killer

Reality: 82% of UK business failures cite cash flow problems as the primary cause (UK Insolvency Service).

Example: A £5M-turnover construction firm collapses because:

– Client pays invoices 90 days late

– Supplier demands upfront payments due to past delays

– Bank rejects emergency loan Result: Liquidation despite £1.2M in “paper profits.”

B. Debt Avalanches – When Borrowing Backfires

Case Study: A fast-growing e-commerce firm takes on high-interest debt to fund inventory. Sales dip, interest compounds, and suddenly 60% of revenue services debt.

– Stat: 40% of UK SMEs struggle with unmanageable debt (Bank of England).

C. Currency & Commodity Swings

Example: A UK bakery’s flour costs jump 30% after a wheat shortage. Contracts lock in prices — margins vanish overnight.

—

2. The Hidden Financial Risks That Compound Quietly

A. Customer Concentration Risk

Scenario: A B2B software firm gets 70% of revenue from one client. When that client leaves, payroll can’t be met.

Rule of Thumb: No single client should exceed 15–20% of revenue.

B. Supplier Dependency & Price Shocks

Case Study: A car manufacturer relies on one battery supplier. When shortages hit, production stalls for 3 months → £9M loss.

C. Fraud & Financial Mismanagement

Stat: UK businesses lose £137B yearly to fraud, waste, and accounting errors (PwC).

Example: A finance director “cooks the books” — investors pull out when the truth surfaces.

—

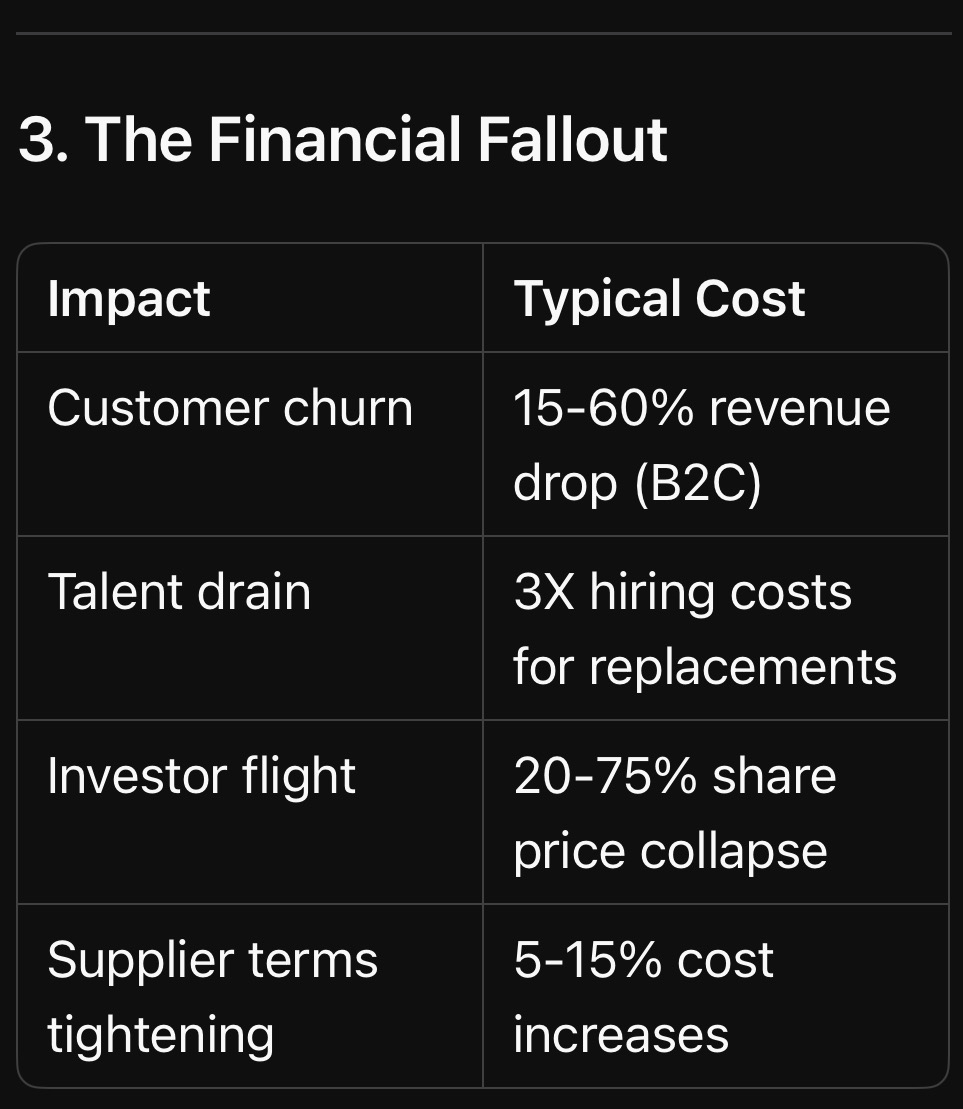

3. The Strategic Fallout: When Financial Risks Spiral

A. Credit Downgrades & Banking Nightmares

Example: A once-stable firm misses a loan covenant — interest rates spike 5%, lines of credit freeze.

B. Investor Panic & Equity Crashes

Case Study: A tech startup’s burn rate exceeds projections — VCs demand emergency restructuring, slashing valuation by 50%.

C. Employee Exodus (When Paychecks Bounce)

Stat: 78% of employees leave within 6 months of payroll issues (CIPD).

—

4. The Ultimate Cost: Bankruptcy Dominoes

A. The “Profitable But Insolvent” Paradox

How It Happens:

1. Big contracts signed → revenue looks strong

2. Clients pay late → cash dries up

3. Suppliers demand payment → no money for salaries/tax

4. HMRC forces liquidation despite “growth.”

B. The Carillion Effect (Again)

£7B collapse triggered by:

– Aggressive accounting

– Reliance on unsustainable contracts

– No cash buffer for delays

Key Insight: Financial risks don’t just reduce profits — they erase businesses in weeks.

—

More from BusinessRiskTV Business Experts Hub : How to Fix It

We explore real-world financial risk strategies, including:

The 13-week cash flow rule (used by turnaround experts)

How to renegotiate debt before it’s too late

Building a “war chest” for crises

Actionable Task: Run a “stress test” on your cash flow: What if 2 clients pay 60 days late?

—

Chapter 5: Cyber Risks – The Invisible Threat That Could Bankrupt Your Business by Breakfast

Introduction: The Digital Time Bomb Ticking in Your Business

Imagine arriving at work to find:

Your customer database on the dark web

Fraudsters draining £250,000 from your account

Ransomware locking every file until you pay Bitcoin

This isn’t a movie plot — it’s Monday morning for thousands of UK businesses. Cyber risks don’t just steal data; they extort cash, destroy reputations, and trigger regulatory hell. And here’s the worst part: Most victims never see it coming until the damage is done.

—

1. The Direct Costs: What Happens When Cybercrime Hits

A. Ransomware: The Digital Kidnapping Epidemic

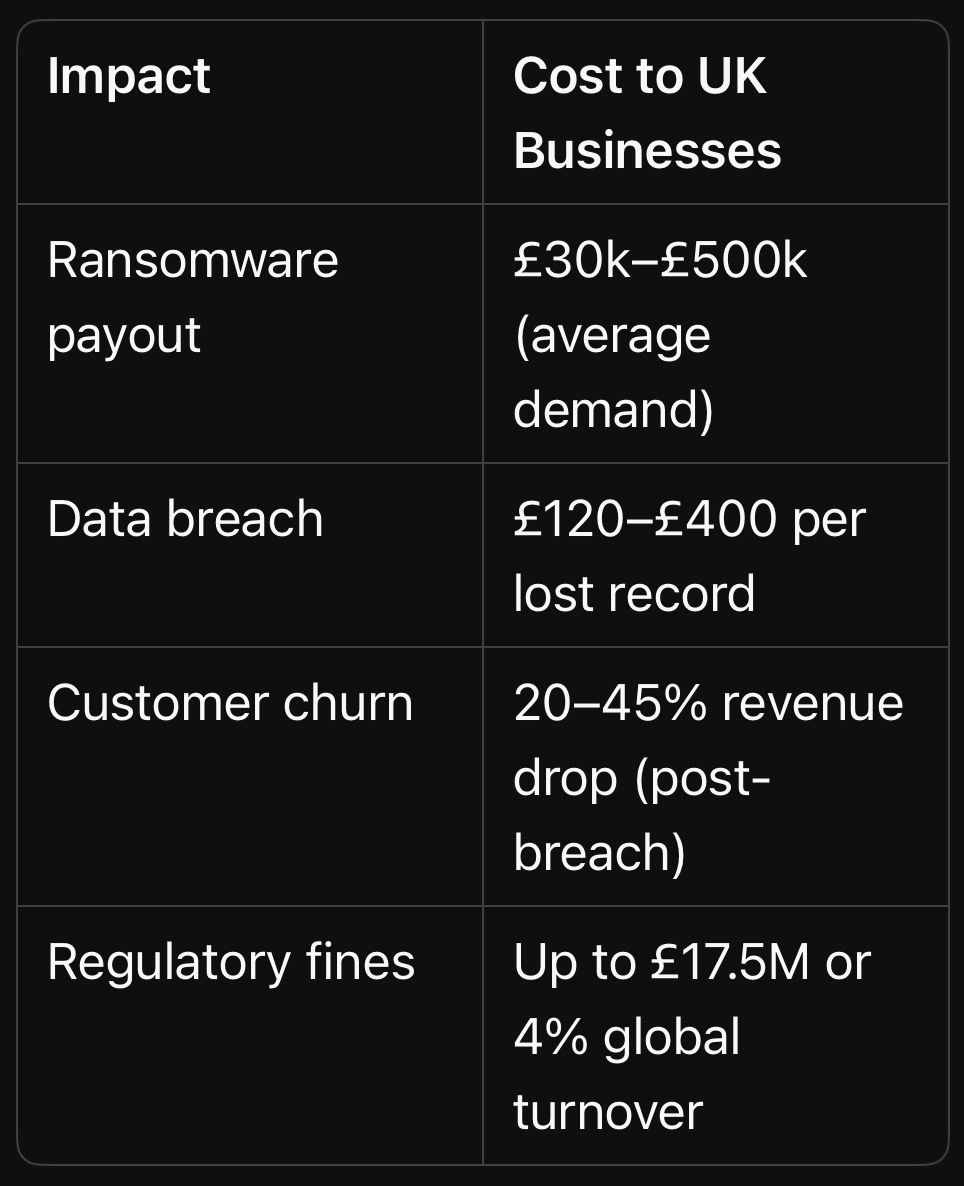

2023 Reality: A UK construction firm’s blueprints, invoices, and payroll systems encrypted. Hackers demand £120,000 to unlock files.

Stat: 73% of UK businesses hit by ransomware in 2023 (NCSC).

Brutal Truth: Paying doesn’t guarantee recovery — 32% never get full data back (Sophos).

B. Data Breaches: When Your Customers Become Victims

Case Study: A mid-sized retailer’s poorly secured e-commerce platform leaks 380,000 credit cards.

£500,000 GDPR fine

£1.2M in fraud reimbursements

22% customer churn

Stat: Average UK data breach cost: £3.4 million (IBM).

C. Business Email Compromise (BEC): The Silent Heist

How It Works: A hacker impersonates your CEO, emails finance: “Urgent: Transfer £80k to new supplier.”

UK Losses: £1.3 billion stolen via BEC in 2023 (UK Finance).

—

2. The Hidden Costs That Cripple You Later

A. Reputation Freefall & Customer Exodus

After a breach:

– 58% of customers avoid breached brands (Verizon)

– Recovery Cost: 3–5X more on marketing to rebuild trust

B. Operational Paralysis

Example: A law firm’s servers go down for 72 hours post-attack. £350k in billable hours lost + client lawsuits.

C. Insurance Nightmares

Post-Claim Realities:

– Premiums triple

– Mandatory audits drain management time

– Some policies simply won’t renew

—

3. The Strategic Fallout: Long-Term Business Damage

A. Lost Contracts & Blacklisting

Government/Corporate Tenders Now Demand:

– Cyber Essentials Certification (missing? Disqualified automatically)

– Proof of incident response plans

B. Investor Flight

Startup Killer: A fintech’s pre-IPO breach scares off VCs, slashing valuation by 60%.

C. Director Liability (Yes, You Can Go to Jail)

UK Law: Under GDPR & NIS Directive, negligent executives face fines up to £17.5M or 4% of global revenue — plus disqualification.

—

4. Why Cyber Risks Are Worse Than You Think

A. It’s Not Just “Big Targets”

61% of UK attacks hit SMEs (Verizon) — hackers bet they’re unprepared.

B. Remote Work = 300% More Attack Surfaces

Example: An employee’s compromised home laptop gives hackers access to your entire CRM.

C. AI-Powered Attacks Are Here

New Threat: Deepfake audio of your CFO “calling” finance to wire funds.

Key Insight: Cyber risks aren’t an “IT problem” — they’re an existential business threat.

—

More from BusinessRiskTV Business Experts Hub : How to Fight Back

We will explore real-world cyber defenses, including:

The 5-step SME ransomware shield (costs <£5k/year)

– How to trick hackers into avoiding you (attackers prefer easy targets)

– Turning employees into human firewalls

Actionable Task: Run this free test now: [Have I Been Pwned](https://haveibeenpwned.com/) to check if your work emails are already in hacker databases.

—

Chapter 6: Human Risks – When Your Greatest Asset Becomes Your Biggest Liability

Introduction: The Enemy Inside Your Walls

Your employees can either be your strongest defence — or your weakest link. Negligence, disengagement, and malicious actions cost UK businesses £30 billion annually (ACAS). This chapter exposes how poor people risk management leads to:

– Catastrophic errors

– Culture collapse

– Regulatory disasters

– Fraud epidemics

And why traditional HR policies fail to prevent 89% of these risks (PwC).

—

1. The Obvious (But Ignored) Human Risks

A. The High Cost of Disengagement

Example: A retail chain’s apathetic staff miss 40% of shoplifting incidents —costing £220,000/year in stolen stock.

Stat: Disengaged employees are 450% more likely to cause operational errors (Gallup).

B. Turnover Tsunamis

Case Study: A tech firm’s toxic culture drives out 7 senior engineers in 6 months — delaying a £2M product launch by 11 months.

Replacement Cost: Up to 2X annual salary per lost employee (Oxford Economics).

C. Training Gaps That Become Legal Nightmares

Reality Check: A warehouse worker badly operates a forklift, causing £80k in damages + HSE fines—because “training was just a 10-minute video.”

—

2. The Hidden (But More Dangerous) Human Risks

A. Insider Threats: When Employees Attack

Shocking Stat: 58% of data breaches involve insiders (Verizon).

Methods:

– The Malicious: IT admin sells customer data (£50k on dark web)

– The Careless: Accountant emails payroll files to personal Gmail

B. Culture Risks: How Toxicity Spreads

Example: A sales team’s “win at all costs” mentality leads to fraudulent client promises — £600k in lawsuits + FCA investigation.

C. Leadership Blind Spots

CEO Overconfidence: Ignoring team warnings about a flawed expansion → £3M write-off.

Stat: 82% of business failures trace back to poor leadership decisions (KPMG).

—

3. The Strategic Fallout: When People Risks Sink Companies

A. The Volkswagen Emissions Scandal

Root Cause: A culture where “nobody dared question” fraudulent engineering.

– Cost: €32 billion in fines/losses + permanent brand damage.

B. The Barclays CEO Scandal

How It Happened: Leadership’s obsession with “star hires” led to unchecked bullying — triggering £1M fines + investor revolt.

C. The Everyday SME Killer

Scenario: Your “trusted” bookkeeper embezzles £150k over 3 years — exposed only during a tax audit.

—

4. Why Traditional Approaches Fail

Annual compliance training?86% of employees forget it within 30 days (MIT).

“Hotline whistleblowing”?62% of staff fear retaliation (EY).

Top-down policies? Frontline teams see them as “head office nonsense.”

Key Insight: Your employees create or destroy value daily — often without realising it.

—

More from BusinessRiskTV Business Experts Hub : How to Transform Human Risk into Advantage

We explore battle-tested solutions, including:

The “Psychological Safety” hack

How to spot insider threats before they strike

Turning compliance into competitive edge

Actionable Task: Run a 5-minute “risk culture pulse check” with your team this week: “What’s one process you think could fail catastrophically?”

—

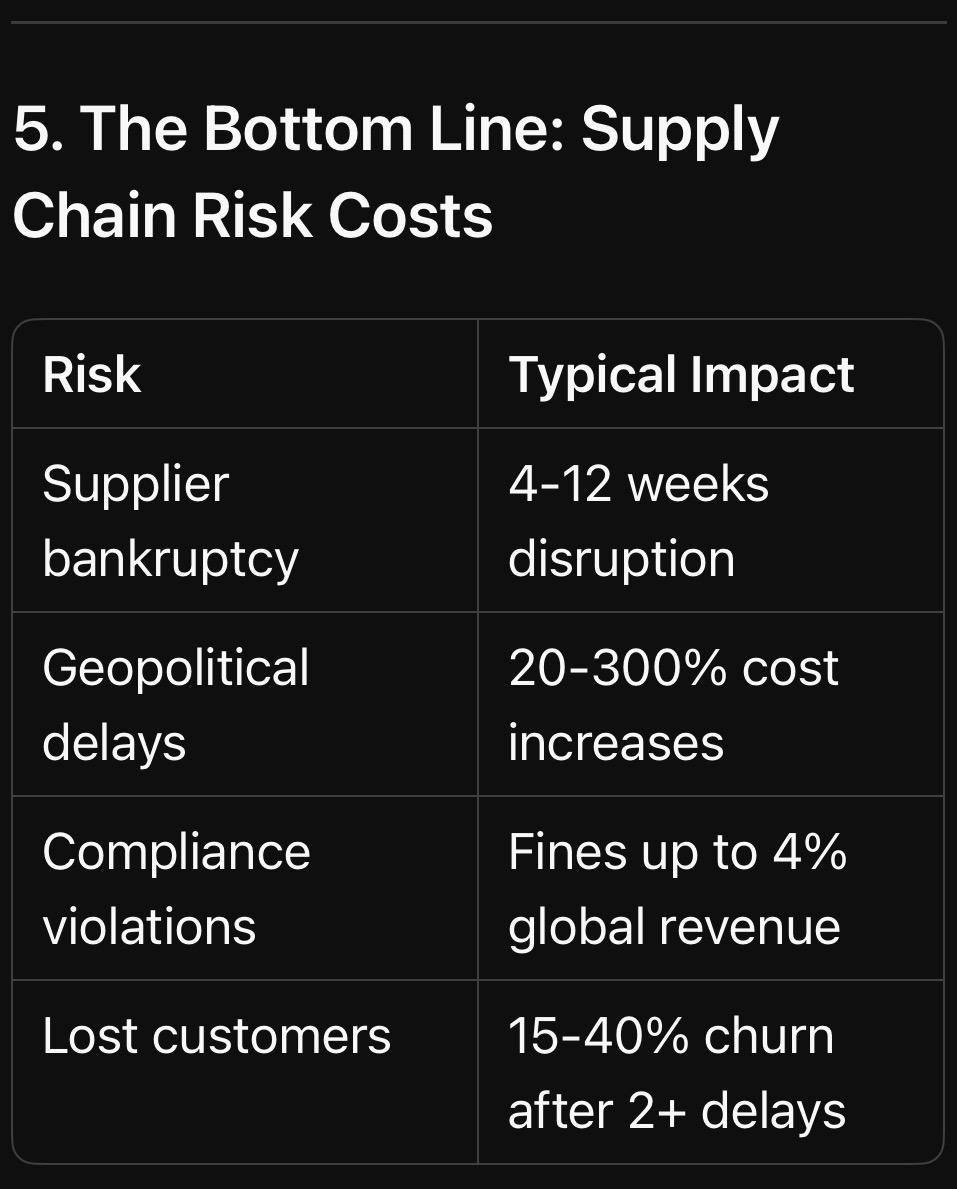

Chapter 7: Supply Chain Risks – The Fragile Web That Could Strangle Your Business Overnight

Introduction: Your Business Is Only as Strong as Its Weakest Supplier

A single delayed shipment. One insolvent vendor. A geopolitical shockwave. Suddenly, your production line stops, customers revolt, and cash flow evaporates.

Key Insight: Supply chains have become the ultimate leverage point — for your competitors or your downfall.

—

More from BusinessRiskTV Business Experts Hub : How to Build an Unbreakable Supply Chain

We explore wartime-tested strategies, including:

The “3D Supplier Mapping” trick (used by Special Forces logisticians)

How to turn suppliers into partners (not adversaries)

When to nearshore/onshore without bankrupting yourself

Actionable Task: Identify one “critical” supplier you couldn’t operate without. How would you survive if they vanished tomorrow?

—

Chapter 8: Reputational Risks – When Trust Collapses Faster Than Your Share Price

Introduction: The 24-Hour Business Execution

A single tweet. One viral video. A disgruntled employee’s LinkedIn post. In today’s digital wildfire, your hard-earned reputation can evaporate before your crisis team finishes their first coffee.

The brutal reality:

87% of consumers will abandon a brand after a reputation crisis (YouGov)

It takes 4-7 years to build trust but just 4 bad days to destroy it (Edelman Trust Barometer)

65% of a company’s market value is tied to intangible assets like reputation (Ocean Tomo)

This isn’t about PR spin – it’s about preventing the preventable and surviving the unpredictable.

—

1. The Obvious Reputation Killers

A. Social Media Firestorms

Case Study: A restaurant manager’s racist comment caught on video → 300,000 angry tweets in 48 hours → permanent 40% revenue drop

Stat: Viral crises spread 20x faster than management can respond (MIT Sloan)

B. Executive Scandals

The P&G CEO Effect: A $375 billion company lost $40B in market cap in days after CEO’s inappropriate relationship surfaced

“No comment” = “We’re guilty” in public perception

Corporate-speak increases distrust by 41% (Edelman)

Legal-first responses often worsen the crisis

—

5. The Survival Playbook (Preview)

More from BusinessRiskTV Business Experts Hub we will explore modern reputation armour, including:

The “Dark Web Early Warning” system (catch crises before they explode)

Turning employees into reputation ambassadors

When to apologise vs. when to fight back

Actionable Task: Google “[Your Brand] + scandal” right now. What autocomplete suggestions appear?

—

Chapter 9: Climate Risks – The Existential Threat That’s Already Costing Your Business

Introduction: Your Business Is on the Frontlines of the Climate Crisis

Climate change isn’t a distant threat — it’s eroding profits, disrupting supply chains, and rewriting industry rules rightnow. In 2024 alone, climate disasters caused $2 trillion in global losses, with businesses absorbing the brunt through:

Operational shutdowns (e.g., factories flooded, data centres overheated

Soaring insurance premiums (up 300% in high-risk zones)

Regulatory penalties (e.g., non-compliance with carbon disclosure rules)

This chapter exposes the hidden costs of climate risks — and why most companies are dangerously unprepared.

—

1. The Two Faces of Climate Risk

A. Physical Risks: When Nature Attacks

1. Acute Disasters:

– Example: Hurricane Helene (2024) caused $225B in damages, disrupting microchip supplies by destroying a key quartz supplier .

– Stat: Severe weather events now cost businesses $560–610B yearly in asset losses .

2. Chronic Pressures:

– Heatwaves reduce worker productivity by 15–20% in sectors like construction and agriculture .

– Droughts forced a UK beverage company to halt production for 6 weeks due to water shortages .

B. Transition Risks: The Legal and Market Backlash

1. Policy Shocks:

– Carbon taxes could erase 20% of profits for high-emission firms by 2030 .

– Example: EU’s Carbon Border Tax added 10–20% costs for non-compliant imports .

2. Reputation Fallout:

– 75% of consumers boycott brands with poor sustainability records .

– Investor Flight: ESG-backlash aside, 90% of Fortune 500 firms now face shareholder climate lawsuits .

—

2. The Hidden Costs You’re Not Tracking

A. Supply Chain Domino Effects

Case Study: Floods in Thailand (2023) disrupted 40% of global hard drive production → tech firms lost $20B+

Stat: 73% of companies admit their supply chains are “highly vulnerable” to climate shocks .

B. Workforce Crises

Heat Stress: UK warehouses saw 30% more sick days during 2024’s record summer .

Talent Drain: 67% of Gen Z employees reject jobs at firms with weak climate policies .

C. Stranded Assets

Example: Oil companies wrote off $300B in reserves as “unburnable” due to net-zero policies.

Projection: 20% of commercial real estate will be uninsurable by 2030 .

Key Insight: Climate risks are profit killers — not just “ESG checkboxes.”

—

More from BusinessRiskTV Business Experts Hub : How to Fight Back

We will explore actionable climate resilience strategies, including:

The “3D Supply Chain Mapping” tactic (used by Special Forces logisticians)

How to turn carbon cuts into tax savings

AI-powered climate forecasting tools

Actionable Task: Run a 5-minute vulnerability scan: Which single climate threat (e.g., flood, heatwave) couldshut down your operations for 48 hours?

—

*Sources: World Economic Forum , Allianz , Beazley , Optera , EPA *

Chapter 10: 12 Actionable Solutions to Transform Risk into Competitive Advantage

Introduction: Risk Management Isn’t About Survival—It’s About Dominance

The most profitable companies don’t just avoid risks — they weaponise them. Toyota’s supply chain resilience made it the #1 automaker during the chip shortage. Amazon turned cybersecurity into a $35B AWS profit centre.

This chapter delivers 12 battle-tested solutions to stop losing money and start outpacing competitors.

—

Solution 1: The “Risk Ownership” Culture Hack

Problem: Employees see risk as “management’s problem.”

Fix:

– Tie 10-15% of bonuses to risk KPIs (e.g., near-miss reports, compliance audits)

– Example: A logistics firm reduced warehouse injuries by 62% after adding safety metrics to performance reviews

Action Step: This week, have each department identify one preventable risk they’ll now “own.”

—

Solution 2: The 5-Minute Daily Risk Radar

Problem: Monthly reports miss emerging threats.

Fix:

– Daily 5-minute standups on:

Top 3 operational vulnerabilities (e.g., server capacity, inventory levels)

Weak signals (e.g., supplier payment delays, social media complaints)

Case Study: A manufacturer caught a critical component shortage 3 weeks early by tracking supplier lead times daily

**Template:**

“`

[ ] Key risk #1 status

[ ] New threat detected

[ ] Mitigation action

“`

—

Solution 3: Cyber “Human Firewall” Training That Works

Problem: Boring compliance training fails.

Fix:

Monthly simulated phishing with “hacked” employees retaking interactive VR training

Result: One law firm reduced click-through rates from 28% to 3% in 6 months

Free Tool: Use CanIPhish for automated simulations

—

Solution 4: The 13-Week Cash Flow War Chest

Problem: Companies die from cash flow gaps, not lack of profit.

Fix:

1. Map all cash inflows/outflows week-by-week

2. Identify 3 survival levers (e.g., delayed payables, early collections)

3. Stress test with:

– 30% sales drop

– 60-day client payment delays

Example: A restaurant chain survived COVID by pre-negotiating 90-day rent deferrals before lockdowns

—

Solution 5: Supplier “X-Ray” Audits

Problem: 4th-tier suppliers can bankrupt you.

Fix:

– Demand blockchain-tracked materials for critical inputs

– Red Team Test: Randomly delay payments to check supplier liquidity

– Stat: Firms with mapped supply chains recover 9x faster from disruptions

—

Solution 6: AI-Powered Risk Forecasting

Toolkit:

Climate: Cervest (predict asset flooding)

Cyber: Darktrace (autonomous threat detection)

Financial: Simudyne (stress test scenarios)

ROI Example: A insurer cut claims by 22% using flood prediction AI

—

Solution 7: The “Pre-Mortem” Strategy Session

Problem: Executives ignore failure scenarios.

Fix: Before decisions:

1. Imagine the project has failed catastrophically

2. Brainstorm exactly why

3. Build safeguards

Case Study: Boeing’s 737 Max crashes could’ve been prevented by this method

—

Solution 8: Embedded Risk Officers

Innovation: Place risk champions in:

– R&D teams (kill flawed prototypes early)

– Sales (flag unrealistic client promises)

– Result: A pharma firm avoided $200M in FDA fines by catching compliance gaps during drug development

—

Solution 9: Dynamic Risk Scoring

Tool: Custom risk dashboards weighting:

– Probability (1–10)

– Impact (£)

– Velocity (how fast threat is growing)

– Example: A bank auto-prioritises risks scoring >£500k impact

—

Solution 10: The “Unthinkable” Drill

Annual Exercise: Simulate:

– CEO arrested

– HQ destroyed

– Key Result: BrewDog survived a ransomware attack because they’d practiced IT failovers quarterly

—

Solution 11: Turn Risk Into Revenue

Examples:

– Tesla sells carbon credits ($1.8B in 2023)

– Maersk’s green shipping premiums command 20% price hikes

The dangers and potential benefits of nano fabrication

Hold on tight, because the future of your business – and maybe even everything else – is about to get seriously Nano-fied! Forget incremental improvements; we’re talking about a technological leap so massive it makes the internet revolution look like dial-up. I’m talking about nanofabrication, and it’s not some sci-fi pipe dream anymore. It’s knocking on the door, and if you’re not ready, traditional fabricators will be the least of your worries!

Imagine having a machine, right in your factory or even your office, that can build things atom by atom. Anything. From the strongest materials imaginable to personalised medicines designed just for you, to electronics so tiny they’re practically invisible. Sounds like magic, right? Well, that’s the potential of nanofabrication, and it’s closer than you think.

Why should you, a busy business leader, care about something that sounds like it belongs in a science fiction movie? Because this isn’t just about cool gadgets. It’s about a fundamental shift in how we make things, who can make them, and what is even possible. It’s a chance to leapfrog your competition, create entirely new markets, and solve problems we can only dream of tackling today. But it also carries risks so profound they could reshape the very fabric of our economy and society.

Think about it: what happens to traditional manufacturing when anyone can essentially “print” products with superior properties on demand? What happens to the pharmaceutical industry when personalised medicine becomes the norm, created at the nanoscale? What new security threats emerge when materials can be engineered at the atomic level?

This isn’t just a technological trend; it’s a potential industrial and societal earthquake. And you need to be ready to navigate it.

In this article, I’m going to break down what nanofabrication is, why it’s on the cusp of becoming a reality, and the mind-blowing opportunities and terrifying threats it presents. Then, I’ll give you nine concrete, actionable steps you can take right now to understand, prepare for, and even capitalise on this coming revolution in the UK. Forget incremental improvements; we’re talking about a paradigm shift! Let’s dive in before it’s too late!

Nanofabrication: Your Personal Genie’s Lamp is Almost Here!

Okay, let’s get down to brass tacks. What exactly is this “nanofabrication” I keep talking about? Simply put, it’s the science and technology of designing and creating structures, devices, and systems at the nanoscale – that’s one billionth of a metre! To give you some perspective, a nanometer is about the width of a few atoms lined up. At this scale, the properties of materials can change dramatically. Gold, which is typically yellow, can appear red or green at the nanoscale!

Now, how do we even think about building things at this scale? There are two main approaches:

Top-down nanofabrication: This is like taking a block of something and carving away material to create nanoscale features. Think of a sculptor working with incredibly fine tools. Current microfabrication techniques used to make computer chips are a form of top-down processing, but we’re pushing the limits to achieve even smaller dimensions.

Bottom-up nanofabrication: This is where things get really interesting. It’s like building with atomic LEGOs! We’re talking about assembling structures atom by atom or molecule by molecule. This could involve self-assembly, where molecules spontaneously arrange themselves into desired patterns, or using incredibly precise tools to place individual atoms.

While both approaches are being actively researched, bottom-up nanofabrication is often seen as the “holy grail” because it offers the potential to create materials and devices with unprecedented precision and control over their properties. Imagine designing a material with exactly the strength, conductivity, and flexibility you need, atom by atom!

Why is this “nano-magic” within touching distance of being real?

You might be thinking, “Building things atom by atom? That sounds like something out of Star Trek!” And you’re right, it does sound futuristic. But the progress in several key areas is making it increasingly likely that we’ll see practical nanofabrication technologies in the coming decades, perhaps even sooner than you think!

Advancements in Microscopy: We can now see and even manipulate individual atoms using powerful microscopes like Scanning Tunneling Microscopes (STMs) and Atomic Force Microscopes (AFMs). These aren’t just for looking; they can be used as incredibly fine tools to move atoms around.

Self-Assembly Breakthroughs:Scientists are making huge strides in understanding and controlling how molecules self-assemble. Imagine designing molecules that automatically snap together in a specific way to form nanoscale structures! This could revolutionise manufacturing by allowing us to “grow” complex devices.

Progress in Nanomaterials: We’re already seeing the impact of nanomaterials like graphene and carbon nanotubes, which have extraordinary properties. Nanofabrication will allow us to precisely engineer these and other nanomaterials for specific applications.

Convergence with Biotechnology:The ability to work at the nanoscale is crucial for advances in medicine. Nanoparticles are already being used for drug delivery, and nanofabrication could lead to revolutionary diagnostic tools and even the creation of artificial biological systems.

Government and Private Investment:There’s significant investment pouring into nanotechnology research and development worldwide, recognising its potential to drive economic growth and solve global challenges. This funding is accelerating the pace of innovation.

So, while we might not have a fully functional “replicator” from Star Trek just yet, the fundamental science is advancing rapidly. The ability to manipulate matter at the nanoscale is no longer a distant dream; it’s a tangible goal that researchers around the world are actively pursuing.

The Double-Edged Sword: Salvation and Existential Threat

Now, let’s talk about why this nanofabrication revolution is both an incredible opportunity and a potentially terrifying threat for your business and for society as a whole.

The Chance of Salvation: Your Business Transformed

For your business, access to nanofabrication could be a game-changer in ways you can barely imagine:

Unprecedented Product Innovation: Imagine creating materials with properties that are currently impossible – stronger than steel but lighter than aluminum, self-healing surfaces, or materials that can adapt to their environment. This opens the door to entirely new product categories and functionalities.

Personalised and On-Demand Manufacturing: Nanofabrication could enable highly customised products tailored to individual needs, produced on demand with minimal waste. Think personalised medicines created at the point of care or bespoke materials engineered for a specific application. This could revolutionise supply chains and inventory management.

Miniaturisation and Efficiency:Nanoscale manufacturing allows for the creation of incredibly small and efficient devices. Imagine sensors so tiny they can be embedded virtually anywhere, or electronic components with unimaginable processing power in a minuscule space. This has huge implications for industries from electronics to healthcare.

New Materials and Processes: Nanofabrication could unlock the creation of entirely new materials with unique properties, leading to breakthroughs in energy storage, catalysis, and many other fields. It could also enable more sustainable and environmentally friendly manufacturing processes with reduced waste and energy consumption.

Competitive Advantage: Early adopters of nanofabrication technologies will gain a significant competitive edge. They will be able to offer products and services that their competitors simply cannot match, potentially disrupting entire industries and creating new market leaders.

For a UK business, being at the forefront of this technology could revitalise manufacturing, create high-skilled jobs, and position the nation as a global leader in innovation. Access to advanced nanofabrication facilities and expertise could attract investment and drive economic growth.

The Potential Existential Threat: A World Reshaped – For Better or Worse?

However, the power to manipulate matter at the atomic level also comes with significant risks:

Disruption of Traditional Industries: As nanofabrication becomes more widespread, traditional manufacturing industries that rely on economies of scale and established processes could face existential threats. If anyone can “print” high-quality goods on demand, the need for large factories and complex supply chains could diminish.

Economic Inequality: Access to nanofabrication technologies could be unevenly distributed, potentially exacerbating economic inequality. Those who control these powerful tools could gain even more power, while others are left behind.

Security Risks: The ability to create materials and devices with unprecedented properties could also be exploited for malicious purposes. Imagine nanoscale weapons that are virtually undetectable or self-replicating nanobots that could pose a serious threat.

Environmental Concerns: While nanofabrication could lead to more sustainable manufacturing in the long run, the development and use of certain nanomaterials could also pose new environmental and health risks if not managed carefully.

Ethical Dilemmas: The ability to manipulate life at the nanoscale raises profound ethical questions. What are the limits of what we should create or modify? How do we ensure that these technologies are used responsibly and for the benefit of humanity?

The “Traditional Fabricator” Scenario: The initial analogy of “traditional fabricators” highlights a key concern. If competitors gain access to advanced nanofabrication capabilities before you do, they could rapidly erode your market share by producing superior, cheaper, or entirely novel products. This isn’t just about keeping up; it’s about survival.

For the UK, failing to engage with and regulate nanofabrication effectively could lead to economic disadvantage, security vulnerabilities, and missed opportunities for innovation and growth.

Nine Things Business Leaders Should Be Aware Of (Even If You Think This is Too Complicated!)

Okay, I know this might sound like a lot to take in. But trust me, as a business leader in the UK, you need to start thinking about this now. Here are nine crucial things you should be aware of about nanofabrication, even if you feel like your brain is already full:

It’s Not Just Science Fiction Anymore: Stop thinking of nanotechnology as something that will happen in a distant future. The underlying science is advancing rapidly, and we’re seeing real-world applications emerge. Keep an eye on developments in materials science, advanced manufacturing, and biotechnology – these are often leading indicators.

It Will Disrupt Your Industry (Eventually): No matter what business you’re in, nanofabrication has the potential to disrupt it. Think about how your products are made, what materials you use, and how you reach your customers. Could a competitor using nanofabrication create a better, cheaper, or more personalised alternative? Start asking these “what if” questions now.

Ignoring It is Not a Strategy: Pretending this isn’t happening won’t make it go away. In fact, it will put you at a significant disadvantage when your competitors start leveraging these technologies. Proactive engagement, even at a basic level, is crucial.

Talent is Key (Even if You Don’t Understand the Science): You don’t need to become a nanoscientist overnight, but you do need to understand the importance of talent. Start thinking about how you can attract and retain individuals with expertise in related fields like materials science, advanced manufacturing, and data science. Collaborating with universities and research institutions could be a good starting point.

Intellectual Property Will Be More Critical (and More Complex): If you can create anything at the atomic level, protecting your innovations becomes paramount. Existing IP frameworks might not be sufficient to address the unique challenges of nanofabricated products and processes. Start thinking about your IP strategy in this new context.

Regulation Will Be a Moving Target (But You Need to Engage): Governments around the world are grappling with how to regulate nanotechnology. This will likely evolve as the technology matures. Stay informed about potential regulations in the UK and engage in the policy debate to ensure a level playing field and responsible innovation.

Collaboration is Essential (You Can’t Do This Alone): The development and adoption of nanofabrication will require collaboration across disciplines and sectors. Consider forming partnerships with research institutions, other businesses, and government agencies to stay informed and explore potential opportunities.

Sustainability Could Be a Major Driver (and Benefit):Nanofabrication offers the potential for more sustainable manufacturing processes with reduced waste, energy consumption, and the use of scarce resources. Explore how these technologies could align with your sustainability goals and create new value for your business.

The Pace of Change Will Be Faster Than You Think (So Start Now!):Technological advancements are accelerating. What seems like science fiction today could be a reality much sooner than you expect. Don’t wait until it’s too late to start understanding and preparing for the nanofabrication revolution.

Protecting and Growing Your Business with Nanofabrication in the UK: Actionable Steps

So, how can you, as a business leader in the UK, not just survive but thrive in this coming era of nanofabrication? Here are some actionable steps you can take:

Invest in Education and Awareness: Dedicate resources to understanding the potential of nanofabrication for your industry. This could involve attending industry conferences, subscribing to relevant publications, and even bringing in experts for internal workshops. The goal is to build a foundational understanding within your leadership team.

Scan the Horizon for Emerging Applications: Actively monitor research and development in nanofabrication relevant to your sector. Identify potential applications that could create new products, improve existing ones, or streamline your processes. Look at patent filings, scientific publications, and news from innovative startups.

Explore Potential Collaborations: Reach out to universities and research institutions in the UK that are leading in nanotechnology research. Explore opportunities for joint projects, sponsored research, or access to specialised facilities and expertise. Organisations like the Knowledge Transfer Network (KTN) can help facilitate these connections.

Consider Strategic Investments (When the Time is Right): As nanofabrication technologies mature and become more commercially viable, consider making strategic investments in relevant equipment, processes, or startups. This requires careful due diligence and a long-term perspective. Government grants and funding initiatives for advanced manufacturing might be available.

Focus on High-Value, Differentiated Products:Nanofabrication excels at creating products with unique properties and high levels of customisation. Shift your focus towards developing and marketing such products that can command premium prices and are difficult for competitors using traditional methods to replicate.

Build a Future-Ready Workforce: Invest in training and upskilling your workforce to prepare for the skills needed in a nanofabrication-enabled economy. This includes expertise in materials science, data analysis, automation, and potentially even nanoscale engineering. Consider apprenticeships and partnerships with educational institutions.

Strengthen Your Intellectual Property Strategy: Review your current IP strategy and consider how to protect innovations arising from nanofabrication. This might involve exploring new types of patents or developing strong trade secrets. Seek advice from IP specialists with expertise in nanotechnology.

Engage with Policymakers and Regulators: Participate in discussions and consultations related to the regulation of nanotechnology in the UK. Advocate for policies that promote responsible innovation while creating a supportive environment for businesses to adopt these technologies. Industry bodies and trade associations can play a key role here.

Embrace a Culture of Innovation and Experimentation: Nanofabrication opens up a world of possibilities. Foster a culture within your organisation that encourages experimentation, risk-taking, and the exploration of unconventional ideas. Create dedicated teams or initiatives to explore the potential of nanotechnology for your business.

The age of nanofabrication is dawning. It presents both unprecedented opportunities and potentially devastating threats. By understanding the fundamentals, staying informed about developments, and taking proactive steps now, UK business leaders can position themselves not just to survive, but to thrive in this revolutionary new landscape. Don’t wait for the genie to appear; start exploring the lamp today!

Protect and grow your business with BusinessRiskTV